.png)

The Organ-on-chip technology B2B market by our Market Intelligence AI agent

Of course, here is the complete blog post based on your detailed instructions and provided data.

\*\*\*

# **Navigating the €3.5 Billion Frontier: A Deep Dive into the Organ-on-Chip Technology B2B Market**

**Meta Description:** An in-depth analysis of the Organ-on-Chip technology B2B sector: explore market size, Go-To-Market strategies, competitive dynamics, and the game-changing opportunities revealed by artificial intelligence and automation.

**Keywords:** Organ-on-chip technology B2B, artificial intelligence, AI market analysis, Organ-on-chip technology 2025, AI agents Organ-on-chip technology B2B, biotech, pharmaceutical R&D, preclinical models.

\*\*\*

### **Introduction: The Dawn of a New Era in Biotechnology**

The Organ-on-Chip (OoC) technology market represents more than just an incremental advance in biotech tooling; it signifies a paradigm shift in how we approach drug discovery, toxicity testing, and disease modeling. By simulating the intricate biology of human organs on microfluidic chips, this technology is poised to replace outdated, expensive, and ethically complex animal testing models with faster, more predictive, and human-relevant alternatives. The a market is not just emerging; it is accelerating, propelled by a convergence of regulatory tailwinds, intense pharmaceutical R&D pressures, and rapid technological innovation.

This in-depth analysis, compiled from extensive market data, offers a comprehensive exploration of this dynamic sector. We will dissect the market's structure, size, and growth drivers, providing a clear view of its €3.5 billion landscape. We will then outline three distinct Go-To-Market playbooks tailored to the primary customer segments, revealing how to effectively engage and convert key decision-makers. Following this, we will map the competitive environment, identifying the leaders who currently hold the power and the challengers poised to disrupt the status quo.

Furthermore, we will conduct a rigorous SWOT analysis to uncover the market's structural strengths, critical vulnerabilities, and untapped opportunities. Finally, we will look to the future, conceptualizing a suite of specialized AI agents designed to augment human expertise and orchestrate the entire Organ-on-Chip value chain. This article is your definitive guide to understanding and navigating the complexities and immense potential of the Organ-on-Chip B2B market in 2025 and beyond.

---

## **Section 1: The Organ-on-Chip B2B Market: A €3.5 Billion Landscape of Rapid Growth and Innovation**

[PLACEHOLDER - YOUR MARKET URL]

The Organ-on-Chip technology market is an emerging powerhouse within the biotechnology landscape, engineered to address some of the most pressing challenges in modern medicine. These microfluidic cell culture devices, which simulate the complex biology and physiology of human organs, are becoming indispensable tools for improving the efficiency and success rates of drug discovery, toxicity testing, and disease modeling. This analysis, informed by detailed market intelligence, reveals a sector not just on the cusp of a breakthrough, but in the midst of a significant expansion.

#### **Market Size and Projections: A High-Growth Trajectory**

The market's financial landscape is exceptionally robust. Our analysis sizes the **Total Addressable Market (TAM) at approximately €3.5 billion as of 2025**, with a remarkable year-over-year **growth rate of 25%**. This valuation is not speculative; it is derived from comprehensive market research reports and substantiated by industry analyses from sources like MarketsandMarkets and Grand View Research. The TAM encompasses all global sales of OoC platforms, including the associated hardware, software, and services integral to their operation.

Looking deeper, we estimate the **Serviceable Addressable Market (SAM) at €1.4 billion**. This figure represents the portion of the market where specifically vascularized OoC platforms and integrated hardware-software solutions, like those developed by innovative firms such as Cellbox Labs, have the most direct application. The SAM is calculated as approximately 40% of the TAM, focusing on pharmaceutical and biotech companies actively investing in these advanced modalities.

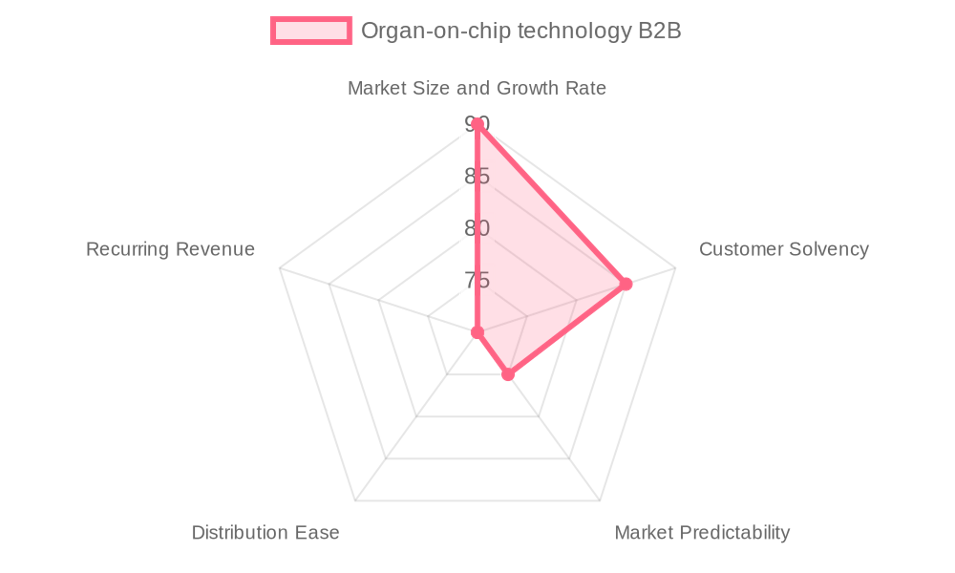

The **Serviceable Obtainable Market (SOM)**, representing a realistic market capture for a well-positioned player over the next 3-5 years, is estimated at **€140 million**. This projection assumes a company could capture about 10% of the SAM by leveraging a unique technological value proposition, such as advanced vascularization, supported by strong R&D and strategic partnerships. The market's attractiveness is underscored by a high score of **82 out of 100**, reflecting its impressive size and growth (90/100), the strong solvency of its customers (85/100), and its growing predictability (75/100).

#### **Detailed Analysis of Key Market Segments**

The a market's growth is fueled by three distinct, yet interconnected, segments, each with unique characteristics and purchase behaviors.

**1. Pharmaceutical Drug Discovery and Development (~50% of TAM)**

This segment, representing a commanding **€1.75 billion** of the total market, is the primary engine of OoC adoption. With a projected **25-30% YoY growth**, it is driven by large and mid-size pharmaceutical companies desperate to accelerate R&D and, crucially, reduce the staggering costs associated with late-stage clinical failures. Their core pain point is the inefficiency and poor predictive power of traditional preclinical models. The buying cycle here is long, typically **6-12 months**, involving multi-stakeholder evaluations where **data reliability, regulatory acceptance, and integration capability** are the paramount decision factors. Key decision-makers include R&D Directors and Heads of Preclinical Research, who are innovation-driven but risk-averse, making trusted partnerships and validated data essential for conversion.

**2. Biotechnology Research Institutions and CROs (~30% of TAM)**

Valued at **€1.05 billion**, this segment consists of academic labs, biotech startups, and Contract Research Organizations (CROs). Growing at a healthy **20-25% annually**, these customers use OoC technology for foundational disease modeling and mechanistic studies. They are scientifically curious, prioritize **experimental flexibility**, and are under pressure to produce fast, reproducible results to secure grants or serve clients. Their pain points revolve around limited access to high-fidelity human models and budgetary constraints tied to grant cycles. The purchase journey is shorter, around **4-8 months**, influenced by project timelines and funding availability. Key decision-makers, such as Principal Investigators and Lab Managers, prioritize **ease of use, cost-effectiveness, and compatibility** with their experimental designs.

**3. Diagnostics and Toxicology Testing Laboratories (~20% of TAM)**

This segment, sized at **€700 million** with a **15-20% YoY growth**, is driven by a powerful regulatory and ethical push. These laboratories are focused on safety and toxicity testing for chemicals, cosmetics, and food products. Their primary driver is the need to comply with increasing restrictions and outright bans on animal testing. This audience is compliance-oriented and ethics-driven, with their main pain point being the need for **reproducible, human-relevant models that meet stringent regulatory standards**. The sales cycle is the shortest, often **3-6 months**, as purchasing decisions are frequently triggered by new regulations. Lab Directors and Quality Assurance Managers make decisions based on **regulatory acceptance, reproducibility, and cost**.

#### **Key Signals and Evolutions Shaping the Market**

Our analysis detected several key signals pointing to the market's future direction:

- **Intensifying Regulatory Tailwinds:** The FDA and EMA are actively expressing interest in OoC technology for preclinical validation, a signal that regulatory acceptance is moving from a possibility to a probability. This directly accelerates demand.

- **The Rise of Personalization:** A growing investment in personalized medicine is creating demand for custom OoC platforms that can model pathologies of specific patient populations, opening a high-value niche.

- **AI and Automation Integration:** The trend of integrating AI-driven data analytics is becoming a key differentiator, moving platforms from simple hardware to intelligent experimental systems.

- **Vascularization as a Standard:** The development of vascularized models is a critical technological leap, dramatically improving the physiological relevance and predictive power of OoC systems.

- **Multi-Organ Systems:** While complex, the pursuit of multi-organ-on-chip platforms that simulate systemic interactions represents the next frontier, promising unprecedented insights into drug effects on the whole body.

These forces are converging to create a market ripe with opportunity. The primary evolution is technological, with a rapid innovation rate pushing the boundaries of microfabrication and biosensor integration. This is complemented by a powerful regulatory evolution, forcing industries to abandon legacy methods. Finally, a behavioral evolution is underway within R&D departments, with a growing acceptance that OoC is not just a research tool, but a critical strategic asset for de-risking drug development pipelines.

---

## **Section 2: Three Potentially Winning Go-To-Market Strategies: How to Conquer Each Segment of the Organ-on-Chip Market**

Successfully penetrating the Organ-on-Chip market requires more than a one-size-fits-all approach. The distinct needs, buying behaviors, and decision-making drivers of each primary segment necessitate tailored Go-To-Market (GTM) strategies. Based on our analysis of ideal customer profiles and personas, we have outlined three specialized playbooks designed to maximize traction and ROI in this complex B2B environment.

[PLACEHOLDER - GTM\_1 IMAGE]

#### **A. GTM for Segment 1: Pharmaceutical Drug Discovery and Development**

This segment is the market's largest prize, but it demands a sophisticated, relationship-driven approach to navigate its long sales cycles and high stakes.

- **Ideal Customer Profile (ICP):** The target is a mature B2B pharmaceutical company in Europe or North America with **500-5,000 employees** and revenues between **€100M-€1B**. Critically, these companies have a dedicated annual OoC R&D budget in the **€1M-€5M range** and are wrestling with decision timelines of **6-12 months**.

- **Winning Persona & Key Obsessions:** The key decision-maker is the **R&D Director**. Their world revolves around three core obsessions: 1) **Reducing late-stage clinical failures**, which represent massive financial and reputational losses; 2) **Ensuring regulatory compliance** with agencies increasingly pushing for human-relevant data; and 3) **Achieving cost and time savings** in the notoriously lengthy drug development process.

- **Top Acquisition Channels:** A multi-touch strategy is essential. **1) Industry conferences** are vital for building credibility and direct networking. **2) Scientific publications and whitepapers** establish technological authority and provide validation. **3) Direct sales and strategic partnerships** are needed to manage the complex, multi-stakeholder procurement process. **4) Highly targeted LinkedIn advertising and outreach** can effectively nurture leads with case studies and ROI-centric messaging.

- **Acquisition Process & ROI:** The acquisition journey is triggered by internal pipeline optimization goals or new regulatory guidance. A typical 4-step process involves: **1) Awareness** through thought leadership content; **2) Consideration**, driven by detailed case studies and validation data; **3) Evaluation**, involving pilot studies and technical deep dives; and **4) Procurement**, managed through strategic partnership agreements. With a Customer Acquisition Cost (CAC) benchmarked at **$15,000**, the long-term value (LTV) from multi-year platform usage, consumables, and software licenses can create a highly favorable **LTV:CAC ratio**, potentially exceeding 10:1.

- **Key Insight to Conquer:** Victory in this segment hinges on **trust and validation**. The message must shift from "our technology is innovative" to "our platform is a validated, de-risked strategic asset that reduces failure costs." Citing EU funding, awards, and successful collaborations with other pharma players is not just marketing—it's a prerequisite for entry.

[PLACEHOLDER - GTM\_2 IMAGE]

#### **B. GTM for Segment 2: Biotechnology Research Institutions and CROs**

This segment is driven by scientific curiosity and project-based funding, requiring a GTM strategy focused on flexibility, education, and accessibility.

- **Ideal Customer Profile (ICP):** The target is a biotech startup, academic lab, or CRO with **50-500 employees** and revenues of **€5M-€50M**. These organizations are early-to-mid-technology adopters with smaller annual OoC budgets of **€100K-€500K** and a decision timeline of **4-8 months**, often tied to grant cycles.

- **Winning Persona & Key Obsessions:** The **Principal Investigator (PI)** is the central figure. Their obsessions are: 1) **Generating publishable data** to secure future funding and build their reputation; 2) **Accessing flexible and cost-effective platforms** that can be adapted to various experimental designs without prohibitive costs; and 3) **Achieving reproducible results quickly** to meet project deadlines.

- **Top Acquisition Channels:** The most effective channels are those trusted by the scientific community. **1) Scientific journals and publications** are the gold standard for credibility. **2) Workshops and webinars** hosted by collaborating academics provide invaluable peer-to-peer validation. **3) Industry trade fairs and academic conferences** offer opportunities for hands-on demos. **4) Google Ads targeting specific research keywords** (e.g., "vascularized microfluidics") can capture active interest.

- **Acquisition Process & ROI:** The process is often triggered by a new grant award or a research breakthrough. The 4-step journey includes: **1) Discovery** through scientific literature; **2) Education** via webinars and protocol guides; **3) Trial** with demo units or small-scale pilots; and **4) Purchase**, often through lab managers and procurement officers. With a lower CAC, estimated around **[CAC to complete, lower than segment 1]**, and potential for long-term loyalty as labs grow, the ROI remains strong, especially when high-impact publications result from the platform's use.

- **Key Insight to Conquer:** The winning strategy is to be a **collaborator, not just a vendor**. Providing exceptional technical support, detailed protocols, and grant-writing assistance builds immense goodwill. The message should emphasize **experimental flexibility and ease of use**, highlighting how the platform can accelerate research and lead to high-impact publications.

[PLACEHOLDER - GTM\_3 IMAGE]

#### **C. GTM for Segment 3: Diagnostics and Toxicology Testing Laboratories**

This segment is the most pragmatic and compliance-driven, demanding a GTM strategy centered on regulatory proof and reliability.

- **Ideal Customer Profile (ICP):** The focus is on contract testing labs and regulatory compliance firms with **20-200 employees** and revenues of **€2M-€20M**. They are moderate technology adopters with focused OoC budgets of **€50K-€200K** and short decision timelines of **3-6 months**, dictated by regulatory mandates.

- **Winning Persona & Key Obsessions:** The **Lab Director** is the key buyer, reporting to a Compliance or Safety Officer. Their three obsessions are: 1) **Adopting validated in vitro assays** that demonstrably comply with bans on animal testing; 2) **Ensuring high reproducibility** of results to meet and maintain accreditations; and 3) **Managing tight cost pressures** in a competitive service-based industry.

- **Top Acquisition Channels:** Channels must align with the regulatory world. **1) Regulatory workshops and industry certification bodies** are prime venues for influence. **2) Industry trade publications** focused on toxicology and chemical safety are key for messaging. **3) Direct sales outreach** citing specific regional regulations is highly effective. **4) Networking at compliance-focused conferences** provides direct access to decision-makers.

- **Acquisition Process & ROI:** The buying trigger is almost always a **regulatory change**. The acquisition process is direct: **1) Awareness** of a compliant solution via trade publications; **2) Validation**, by reviewing reproducibility reports and certification data; **3) Implementation Discussion**, focusing on cost and lab integration; and **4) Purchase**, to meet an impending compliance deadline. The CAC is the lowest of the three segments, and ROI is calculated on a clear cost-benefit basis of compliance versus non-compliance fines or loss of business.

- **Key Insight to Conquer:** **Regulatory alignment is everything.** The conversation must lead with how the platform directly solves a compliance problem. Messaging should be unambiguous, focusing on **reproducibility data, validation against established standards, and case studies of successful regulatory adoption**. The product is not just a piece of technology; it is a compliance solution.

---

## **Section 3: Who Truly Holds the Power in the Organ-on-Chip B2B Market?**

Understanding the competitive landscape in the Organ-on-Chip sector requires looking beyond a simple list of companies. It requires dissecting the value chain to see where power is concentrated, identifying the true axes of differentiation, and mapping the key players according to their ability to innovate and execute. This analysis reveals a market that is highly competitive but not yet commoditized, where strategic positioning and technological superiority are the keys to long-term dominance.

[PLACEHOLDER - COMPETITION URL]

#### **A. The Value Chain: Where Power and Margins Converge**

The Organ-on-Chip value chain consists of several distinct stages: **Research and Development**, **Microfabrication of Devices**, **Integration of Hardware and Software**, **Pharmaceutical Drug Testing**, and **Data Analysis and Interpretation**. While each stage is crucial, the highest barriers to entry—and therefore the greatest concentration of power—lie unequivocally within the **integrated hardware and software system design stage**.

This is where specialized technical expertise meets significant capital investment, proprietary technology, and the need for rigorous regulatory validation. Companies that master this nexus control the core of the value proposition. Market leaders like **Emulate** and **Mimetas** have established formidable bottlenecks here. They leverage advanced, AI-integrated microfluidic platforms and have cultivated deep-seated partnerships with major pharmaceutical clients. This creates substantial negotiating power and high switching costs for customers, as validating and integrating a new platform is a complex and resource-intensive endeavor. Consequently, this segment commands the strongest structural margins and faces the lowest direct competitive intensity, making it the primary theater where durable value is created and captured.

#### **B. The True Axes of Differentiation**

In this sophisticated market, competition does not revolve around price alone. Instead, two fundamental axes of differentiation define a company's position and potential for success:

1. **Technology Sophistication:** This is the primary driver of value. It is not just about the chip itself, but the level of innovation embodied in the entire system. Key components include the biological complexity (e.g., **vascularization**, which drastically improves physiological relevance), the integration of **real-time biosensors**, the ability to simulate **multi-organ interactions**, and the incorporation of **AI-driven analytics** for experiment design and interpretation. Companies leading on this axis offer platforms that generate more predictive, reliable, and actionable data.

1. **Market Reach and Customer Base:** Technological brilliance is insufficient without commercial execution. This axis measures a company's footprint in the market, particularly its penetration into high-value pharmaceutical and biotech accounts. It reflects the scale of commercial operations, the strength of strategic partnerships with industry giants, and the robustness of customer support infrastructure. A strong position on this axis ensures sales volume, generates recurring revenue from consumables and software, and builds the brand recognition necessary for sustained leadership in a B2B environment.

The main competitive tension lies between innovators with high technology sophistication but limited market reach (Specialists) and established players trying to expand their technological edge to defend their broad customer base (Leaders).

[PLACEHOLDER - COMPETITION QUADRANT URL]

#### **C. Mapping the 10 Key Players: Leaders, Challengers, and Specialists**

An analysis of the competitive field, positioning companies based on their technology sophistication and market reach, reveals a clear hierarchy.

- **Market Leaders:** These companies demonstrate strength in both technological innovation and commercial execution. The primary leader is **Emulate**, with an estimated annual revenue of around $60 million and approximately 200 employees. Their leadership is cemented by cutting-edge multi-organ platforms and major partnerships with pharmaceutical giants like Pfizer and Johnson & Johnson. They are closely followed by **Mimetas** (approx. €15M revenue, ~50 staff), known for high-throughput organotypic models popular in Europe, and **CN Bio Innovations** (€12M revenue, ~35 staff), which has a strong offering in vascularized liver-on-chip models.

- **Challengers:** These players have solid operational execution and a growing customer base but may lag slightly in visionary technology or market-wide penetration. This group includes companies like **InSphero**, which excels in scalable 3D cell culture technologies, **Hesperos** (approx. $8M revenue, ~25 staff), focusing on cost-effective toxicology platforms, and **Hurel Corporation**, which delivers reliable human cell-based platforms.

- **Trend-Setting Specialists:** These are highly innovative firms with potentially disruptive technology but currently limited market reach, often due to being resource-constrained or hyper-focused on a niche. **TissUse** (€10M revenue, ~40 staff) is a prime example, pioneering patented multi-organ-on-chip platforms with a strong academic following but less penetration into large pharma. The renowned **Wyss Institute**, while primarily academic, consistently produces foundational innovations that set future market trends.

- **Pure Players:** These companies serve specialized niches with deep expertise but limited ambition for broad market scalability. **Nortis** is a classic example, specializing in kidney-on-chip devices. **Microfluidic ChipShop** is another, providing essential microfluidic components for research but not complete, integrated platforms.

This mapping reveals a dynamic environment where technological specialists are constantly challenging the market reach of established leaders, creating a healthy, innovation-driven ecosystem with a total competitive intensity score of **72 out of 100**.

#### **D. Analysis of the Market Leaders**

The leadership position in the OoC market is held by a cohort of companies that have successfully blended advanced technology with effective commercial strategies. The vanguard includes **Emulate Inc., MIMETAS B.V., TissUse GmBH, CN Bio Innovations Ltd, Insphero AG, Nortis Inc., BioIVT, Dynamic42 GmBH, React4Life, and Obatala Sciences**.

At the forefront is **Emulate, Inc. (USA)**. Their strategy hinges on creating a comprehensive "Human Emulation System" that combines sophisticated Organ-Chips with intuitive software and automated instrumentation. Their strength lies in their deep, multi-year partnerships with top-tier pharmaceutical companies, which not only provide revenue but also serve as powerful validation of their platform's utility and reliability. This market validation, coupled with a strong IP portfolio around their core flow-based technology, makes them the benchmark for competitors.

Other leaders employ parallel strategies. **MIMETAS B.V.** has differentiated itself with its OrganoPlate® platform, which is designed for higher throughput, appealing to CROs and research institutions looking to scale up their experiments. **TissUse GmBH** stands out for its unique, patented multi-organ-on-chip technology, which allows for the study of systemic drug effects—a highly complex but incredibly valuable capability. The key factor uniting these leaders is their ability to provide not just a device, but a full, validated workflow solution that generates reliable, human-relevant data, thereby de-risking the enormous investment of drug development for their clients.

#### **E. Focus on the Challengers: The Pursuit of Disruption**

While leaders define the current market, challengers are shaping its future. This dynamic group includes **CN Bio Innovations Ltd, Dynamic42 GmBH, AlveoliX AG, BeOnChip S.L., Initio Cell, Netri SAS, Hesperos Inc., Lena Biosciences, RevivoCell, and Altis Biosystems**.

The principal challenger to watch is **CN Bio Innovations Ltd**. Having recently raised a **$21 million Series B in 2024**, they are well-capitalized to scale their operations. Their strategy focuses on disrupting the market with advanced, yet accessible, single- and multi-organ models, with a particular strength in liver-on-a-chip technologies that have been adopted by regulatory agencies like the FDA. Their potential for disruption lies in offering solutions that are perceived as more user-friendly and faster to integrate into existing lab workflows than some of the more complex systems from leaders.

Other challengers are employing different angles of attack. **Hesperos Inc.** targets the toxicology market with a focus on cost-effectiveness and replacing animal testing, a powerful value proposition for cosmetics and chemical companies. Companies like **AlveoliX AG** (lung-on-chip) and **BeOnChip S.L.** (microfluidic devices) are succeeding by specializing in a single organ or component with best-in-class performance. The primary threat these challengers pose to leaders is not a frontal assault across the entire market, but a death-by-a-thousand-cuts strategy: winning specific niches, applications, and customer types with more focused, agile, and often more cost-effective solutions, thereby eroding the leaders' market share from the edges.

---

## **Section 4: The Organ-on-Chip Market SWOT: Hidden Strengths, Critical Vulnerabilities, and Strategic Opportunities**

A comprehensive SWOT analysis of the Organ-on-Chip market reveals a sector defined by a powerful tension between explosive growth potential and significant operational complexity. The market's structural strengths provide a robust foundation for growth, but underlying weaknesses create vulnerabilities that savvy competitors can exploit. Unlocking the immense opportunities requires navigating a landscape of potent threats. This deep dive, powered by AI-driven analysis, uncovers the strategic imperatives for success.

[PLACEHOLDER - MARKET SWOT URL]

#### **Structural Strengths: The Pillars of a Thriving Market**

The OoC market is built on exceptionally strong fundamentals that support sustainable growth and profitability. These are not fleeting trends but deep-seated advantages.

1. **Robust Market Fundamentals:** With a current valuation of approximately **€3.5 billion** and a staggering **25% year-over-year growth rate**, the market offers significant headroom for expansion. This high-growth environment allows multiple players to thrive without resorting to zero-sum competition. AI-driven predictive analytics can further amplify this strength by optimizing R&D workflows and accelerating time-to-market.

1. **Powerful Demand Drivers:** The demand from pharmaceutical companies is not just growing; it’s becoming a strategic necessity. The intense pressure to reduce costly late-stage clinical failures provides a powerful market pull. This is reinforced by a strong regulatory push from bodies like the FDA and EMA to replace animal testing, creating a durable and predictable source of demand.

1. **A Climate of Healthy Innovation:** The market is moderately fragmented, with numerous firms offering differentiated platforms focused on unique features like **vascularization, AI integration, or multi-organ simulation**. This fosters a healthy, innovation-led competitive dynamic, preventing commoditization and rewarding technological advancement.

1. **High Customer Solvency:** The primary customers—large pharmaceutical companies and well-funded biotech firms—possess substantial R&D budgets. This financial stability ensures a reliable revenue stream for OoC providers and supports long-term partnerships, with a benchmark **Customer Retention Rate of 90%** being a key industry KPI.

1. **Favorable Regulatory Framework:** Active encouragement from major global regulatory agencies for the validation and adoption of OoC models provides immense credibility. Furthermore, outright bans on animal testing in sectors like cosmetics create captive markets for these alternative technologies.

1. **Strong Intellectual Property Defenses:** The field is characterized by strong patent protection around core microfluidic designs, proprietary tissue models, and integration techniques. This allows innovative companies to build a defensible moat around their technology, protecting their R&D investments.

#### **Critical Weaknesses: The Structural Fault Lines**

Despite its strengths, the market is not without its challenges. These weaknesses represent risks but also opportunities for companies that can strategically address them.

1. **High Capital Intensity and Long Sales Cycles:** The upfront investment required for R&D, cleanroom microfabrication, and specialized lab facilities is substantial. This financial burden is compounded by long B2B sales cycles, which average **6-12 months** in the pharmaceutical segment, straining cash flow for smaller players.

1. **Complex Regulatory Validation:** While regulators are encouraging, the validation process for new OoC platforms remains complex, costly, and time-consuming. This uncertainty can act as a significant barrier to entry and slow the commercialization of new innovations.

1. **Supply Chain Vulnerabilities:** The entire industry depends on a limited number of specialized suppliers for critical components like biomaterials, microfluidic parts, and biosensors. This concentration exposes companies to supply disruptions, price volatility, and quality control issues. AI-powered supply chain forecasting could mitigate this by predicting demand and identifying alternative suppliers proactively.

1. **Scarcity of Specialized Talent:** The interdisciplinary nature of OoC technology requires a rare blend of expertise in microfluidics, tissue engineering, cell biology, and data science. The scarcity of this talent intensifies recruitment competition and can constrain a company's ability to scale.

1. **Technical and Integration Complexity:** For end-users, adopting a new OoC platform is not a simple plug-and-play process. It requires significant effort to integrate the platform into existing lab workflows and validate the data it produces. This creates moderate switching costs but also customer hesitancy.

1. **Cultural Resistance to Change:** Within some large, conservative organizations, there remains a deep-seated reliance on traditional animal testing models. Overcoming this inertia requires extensive education, compelling validation data, and a clear demonstration of ROI, which slows adoption rates.

[PLACEHOLDER - MARKET SWOT URL 2]

#### **Sectoral Opportunities: Catalysts for Future Growth**

The confluence of market trends and technological advancements is creating a wealth of opportunities for value creation.

1. **Expansion into Personalized Medicine:** The ability to use patient-derived cells to create customized OoC models is a game-changer for precision medicine and rare disease research. This opens up a high-value market segment where tailored platforms can predict individual drug responses. AI is critical here for tailoring models based on patient omics data.

1. **Development of AI-Integrated Multi-Organ Platforms:** The holy grail of OoC is the simulation of systemic, multi-organ interactions. Integrating these complex biological models with AI-driven analytics to interpret the vast datasets they produce represents a monumental opportunity to deliver unprecedented predictive insights.

1. **Transition to SaaS and Service-Based Models:** Forward-thinking companies are moving beyond simple hardware sales. The opportunity lies in creating recurring revenue streams by offering integrated packages that include the device, consumables, cloud-based software, and data analytics-as-a-service (AaaS).

1. **Geographic Expansion into Emerging Biotech Hubs:** While North America and Europe currently dominate, substantial growth potential exists in emerging biotech clusters in the Asia-Pacific region and Latin America. A first-mover advantage could be significant.

1. **Addressing the Toxicology Market:** Beyond pharmaceuticals, there is a massive opportunity in providing validated, high-throughput toxicology testing for the chemical, food, and cosmetics industries, all of which are under regulatory pressure to reduce animal testing.

1. **Data Monetization:** The anonymized experimental data generated by OoC platforms is, in itself, a valuable asset. There is a significant opportunity to create new revenue streams by licensing these datasets and predictive algorithms to pharmaceutical firms and research institutions.

#### **Global Threats: Navigating the Market Risks**

The path to success is lined with several significant threats that require constant vigilance and strategic mitigation.

1. **Intense Competitive Rivalry:** The market is populated by highly specialized and well-funded companies, leading to intense competition. This rivalry puts constant pressure on pricing (evidenced by a market average **Gross Margin of 65%**) and necessitates a relentless pace of innovation to maintain a competitive edge.

1. **Disruption from Alternative Technologies:** Rapid advances in other _in vitro_ technologies or purely computational, AI-driven drug discovery methods could emerge as viable substitutes, potentially reducing the relevance of hardware-based OoC platforms.

1. **Regulatory and Policy Uncertainty:** While the current trend is favorable, a sudden shift in regulatory standards or a delay in the validation pathways for OoC models could significantly slow market growth and disrupt business models.

1. **Cybersecurity Risks:** As OoC platforms become more connected and data-driven, they become attractive targets for cyberattacks. A breach involving sensitive experimental data or proprietary platform software could have devastating reputational and financial consequences.

1. **Economic Volatility:** A global economic downturn could lead to reductions in the R&D budgets of pharmaceutical and biotech companies, which could, in turn, delay purchasing decisions and slow the adoption of new, capital-intensive technologies.

1. **Information Warfare and Misinformation:** In a field built on scientific credibility, misinformation campaigns aimed at undermining the reliability of OoC data or exaggerating the capabilities of competing technologies could erode customer trust and disrupt the market.

**Key Insight & Offensive Strategy:** The central tension in this market is between immense **growth potential driven by technological innovation** and **high barriers to adoption due to technical complexity and regulatory hurdles**. The recommended offensive strategy is to leverage AI not just as a feature, but as a core enabler to address this tension directly. An investment in AI-driven automation for experimental design, data interpretation, and compliance reporting can dramatically lower the barrier to adoption, accelerating sales cycles and creating a powerful competitive advantage.

---

## **Section 5: 15+ AI Agent Concepts Designed for the Organ-on-Chip Sector**

To translate the immense potential of AI into tangible value for the Organ-on-Chip market, it is essential to move beyond abstract concepts and envision concrete applications. The following are conceptual frameworks for AI agents—specialized, automated workflows designed to augment human experts across the value chain. These are not existing products but forward-looking ideas intended to illustrate how targeted AI could revolutionize R&D, operations, and commercial strategy in this sector.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

#### **A. Two High-Impact AI Agent Concepts for Immediate Application**

These two concepts address some of the most critical pain points in the OoC market: the slow pace of research and the long, complex sales cycles.

**Agent Concept 1: "Faye," the AI-Driven Experimental Design & Analytics Agent**

- **Function:** Faye automates the design, monitoring, and interpretation of complex OoC experiments. It integrates multi-omics data, real-time biosensor feeds, and computational simulations to optimize protocols, predict outcomes, and accelerate the validation of new tissue models.

- **Augmented Job Title:** **Research Scientist & Bioengineer.** Faye acts as a tireless digital collaborator, augmenting their expertise by generating hypotheses, detecting experimental anomalies in real-time, and modeling predictive outcomes, effectively freeing them to focus on higher-level strategic research.

- **Problem Treated:** It directly tackles the bottlenecks of long development cycles and the high cost of failed experiments, which are major weaknesses of the market.

- **Concrete Use Case:** A pharmaceutical client wants to test a new oncology drug on a vascularized tumor-on-a-chip model. Faye analyzes existing literature and past experimental data to propose an optimal dosing schedule, cell density, and flow rate. During the experiment, it monitors biosensor data and alerts researchers to early signs of off-target toxicity, allowing them to adjust the protocol and salvage the study, saving weeks of work and significant cost.

- **KPIs Impacted:** 1) **R&D Cycle Time** (reduced by an estimated 20-30%); 2) **Experimental Success Rate** (increased); 3) **Percentage of Revenue from New Products** (accelerated by faster innovation).

- **Game-Changer Impact:** Faye transforms R&D from a linear, trial-and-error process into a dynamic, data-driven cycle of rapid iteration and validation, dramatically enhancing a company's core innovative capacity.

**Agent Concept 2: "Echo," the AI-Powered Sales Cycle & Customer Insight Agent**

- **Function:** Echo uses AI to accelerate the long B2B sales cycle. It analyzes market signals and CRM data to score leads, segments customers based on their specific needs and publications, personalizes outreach content, and predicts potential churn.

- **Augmented Job Title:** **Sales Executive & Marketing Manager.** Echo empowers the commercial team with actionable intelligence, allowing them to prioritize high-intent leads, tailor their technical messaging to a prospect's specific research, and proactively manage key accounts.

- **Problem Treated:** It directly addresses the critical market weakness of long (6-12 month), complex sales cycles and the high Customer Acquisition Cost (CAC) benchmarked at **$15,000**.

- **Concrete Use Case:** Echo identifies a mid-sized pharma company that has recently published papers on kidney toxicity and is hiring for preclinical scientists. It automatically flags this company as a high-priority lead. It then helps the sales executive craft a personalized email sequence that references the company's specific research challenges and highlights how their kidney-on-a-chip platform has produced relevant data in similar studies, leading to a much higher engagement rate and a faster-booked meeting.

- **KPIs Impacted:** 1) **Lead-to-Customer Conversion Rate** (goal to increase from market reference of 8%); 2) **Customer Acquisition Cost (CAC)** (goal to decrease); 3) **Sales Cycle Length** (goal to shorten).

- **Game-Changer Impact:** Echo converts sales from a high-effort, low-yield activity into a precise, insight-driven process, allowing companies to scale their commercial operations much more efficiently and predictably.

#### **B. A Broader Suite of Conceptual AI Agents for the Sector**

Beyond these two, a full ecosystem of specialized agents could be conceptualized to optimize every facet of an OoC business.

[PLACEHOLDER - MARKET SWOT PRIORITY URL]

- **Scout - Market Intelligence Agent:** Augments **Strategy Analysts** by continuously monitoring patents, publications, and competitor announcements to provide early warnings of market shifts and emerging trends.

- **Max - Supply Chain Resilience Agent:** Augments **Operations Managers** by forecasting demand for specialized biomaterials, monitoring supplier risk, and optimizing inventory to prevent costly production delays.

- **Aegis - Regulatory Compliance Agent:** Augments **Regulatory Affairs Specialists** by automatically tracking global policy changes (from FDA, EMA, etc.) and helping to generate compliance documentation, reducing time-to-market.

- **Optima - Manufacturing Process Agent:** Augments **Manufacturing Engineers** by using computer vision and sensor data to monitor microfabrication processes in real-time, predict equipment maintenance needs, and improve device yield.

- **Capital - Financial Planning Agent:** Augments **Finance Directors** by modeling cash flow scenarios, forecasting R&D budget needs, and analyzing investment risks in a capital-intensive environment.

- **Bridge - Stakeholder Education Agent:** Augments **Marketing Teams** by creating personalized educational content and virtual demonstrations to overcome cultural resistance and accelerate technology adoption among conservative stakeholders.

- **Sentinel - Cybersecurity Agent:** Augments **IT Security Officers** by using adaptive AI to detect threats to sensitive experimental data and ensure compliance with data privacy regulations.

- **Nova - Personalized Model Agent:** Augments **Precision Medicine Researchers** by using patient-specific data to customize OoC models and predict individualized drug responses.

- **Insight - Data Monetization Agent:** Augments **Business Development Teams** by packaging anonymized experimental data into licensable datasets, creating new revenue streams.

- **Helix - BioResearch Agent:** Augments **R&D Scientists** by mining biomedical literature to accelerate hypothesis generation and experimental design.

#### **C. The Ultimate Vision: A Coordinated System of AI Agents**

The true transformative potential of AI lies not in isolated agents, but in a fully integrated, interdependent system orchestrated by a master agent. This "AI-augmented company" concept is based on a central orchestrator coordinating specialized agents across the entire value chain.

[PLACEHOLDER - MARKET AGENT SYSTEM URL]

Imagine a **Master Orchestrator Agent**, named **"Harmony Command Center,"** that acts as the digital chief of operations. It has a real-time view of the entire business, from research to sales. Harmony would coordinate the actions of five specialized sub-agents:

1. **Helix (R&D):** Scans for new research breakthroughs.

2. **Forge (Microfabrication):** Manages device production schedules and quality.

3. **Nexus (Integration):** Ensures hardware and software compatibility.

4. **Pharma (Testing):** Oversees automated drug testing protocols.

5. **Matrix (Data Synthesis):** Analyzes results from all stages to find strategic insights.

In this system, when **Helix** identifies a promising new vascularization technique, **Harmony** can instantly task **Forge** with creating a prototype, coordinate with **Nexus** on the new sensor integration, and pre-schedule testing time with **Pharma**. **Matrix** would then analyze the results and feed them back to Harmony, which could decide whether to fast-track the innovation into the commercial pipeline. This creates a hyper-agile, self-optimizing organization where information flows seamlessly, bottlenecks are instantly identified, and strategic decisions are made based on a complete, real-time understanding of the entire value chain. This is the futuristic vision of a company fully augmented by AI, capable of out-maneuvering and out-innovating competitors at every turn.

---

## **Section 6: Is Your Company Ready for the AI-Augmented Future?**

This deep dive into the Organ-on-Chip market reveals a sector at a strategic inflection point. The intersection of rapid growth, technological disruption, and intense competitive pressure creates an environment where efficiency, speed, and insight are paramount. As we've explored, targeted AI agents and systems are not a futuristic fantasy; they are a conceptual blueprint for building a decisive competitive advantage.

Companies that embrace an AI-augmented approach—automating R&D, streamlining operations, and personalizing customer engagement—will be best positioned to capture a disproportionate share of this burgeoning €3.5 billion market. Those who hesitate risk being outpaced by more agile, data-driven competitors. The time to consider how AI can transform your value chain is now.

---

### **Conclusion: Charting a Course in a Transformative Market**

Our comprehensive analysis of the Organ-on-Chip B2B sector paints a vivid picture of a market characterized by immense opportunity and significant complexity. We have uncovered a rapidly expanding **€3.5 billion global market**, growing at a formidable **25% annually**. This growth is primarily fueled by a clear and urgent need within the pharmaceutical sector—which accounts for 50% of the market—to de-risk and accelerate drug development pipelines. The competitive landscape is dynamic, with established leaders like **Emulate** setting the pace through technological sophistication and deep market penetration, while well-funded challengers like **CN Bio Innovations** are strategically positioned to disrupt the status quo.

The key to unlocking this market, as our analysis of Go-To-Market strategies reveals, lies in a highly segmented approach. A one-size-fits-all strategy will fail; success demands tailored playbooks that speak directly to the unique pain points and buying triggers of pharmaceutical R&D directors, academic principal investigators, and compliance-focused lab managers. While the market's structural strengths—such as strong demand drivers and high customer solvency—are compelling, they are balanced by critical weaknesses, including long sales cycles, talent scarcity, and supply chain vulnerabilities.

Looking forward, the direction of the Organ-on-Chip market is clear: it is moving towards more predictive, more complex, and more automated systems. The greatest opportunities lie in the integration of advanced biological features like **vascularization** with the power of **artificial intelligence**. AI is no longer a peripheral technology; it is becoming the central nervous system for the entire OoC value chain. As we conceptualized with our suite of specialized AI agents, the potential for AI to accelerate research, optimize manufacturing, shorten sales cycles, and ensure regulatory compliance is transformative. The companies that will lead the next decade of this market will be those that not only build superior chips but also build superior intelligence into every facet of their operations.

If you are interested in this topic you can follow these next steps:

1️⃣ **Download below the full Organ-on-chip technology B2B market study in pdf format**

[PLACEHOLDER - PDF DOWNLOAD LINK]

2️⃣ **Get additional insights of this market by reading our memo of an interesting company in this market called Cellbox Labs (Advanced vascular organ-on-chip for precise drug discovery)**

[PLACEHOLDER - CELLBOX LABS MEMO LINK]

3️⃣ **If you want us to build a custom AI system and dedicated AI agents, book a strategic discussion with an AI Partner : https://forms.proplace.co/meet**