.png)

The Multi-dimensional Data Indexing SaaS market by our Market Intelligence AI agent

# The Unseen Engine of AI: A Deep Dive into the Multi-dimensional Data Indexing SaaS Market

**Meta Description:** An in-depth analysis of the Multi-dimensional Data Indexing SaaS sector: market size, go-to-market strategies, competitive dynamics, and AI-driven opportunities revealed through automated intelligence. Discover the forces shaping this critical technology backbone.

**Keywords:** Multi-dimensional Data Indexing SaaS, artificial intelligence, AI market analysis, Multi-dimensional Data Indexing SaaS 2025, AI agents Multi-dimensional Data Indexing SaaS, data analytics, big data, cloud computing, Qbeast.

\*\*\*

### Introduction: Navigating the Data Deluge

In the modern digital economy, data is not just an asset; it is the ocean upon which business strategies sail. Yet, navigating this vast, turbulent ocean of information presents a monumental challenge. As data volumes grow exponentially, the ability to query, analyze, and derive insights in real-time has become the critical differentiator between market leaders and laggards. This is where the power of **Multi-dimensional Data Indexing SaaS** emerges—a specialized, high-growth sector acting as the unseen engine powering next-generation analytics and artificial intelligence.

This market is not merely about storage; it's about speed, efficiency, and intelligence. It addresses the core pain points of modern enterprises: sluggish query times that hamper decision-making, exorbitant cloud compute costs that drain budgets, and the bottleneck of preparing massive datasets for AI model training. The solutions in this space are rebuilding the very foundation of data interaction, leveraging patented algorithms and cloud-native platforms to transform slow, expensive processes into agile, cost-effective workflows.

This comprehensive analysis, powered by our Market Intelligence AI agent, will dissect this dynamic landscape. We will explore the market's substantial size and rapid growth, decode the winning go-to-market strategies for its key segments, map the competitive forces at play, and uncover the strategic opportunities and threats that define its future. Finally, we will conceptualize how dedicated AI agents could further revolutionize this sector, augmenting human expertise and unlocking unprecedented value. This deep dive offers a strategic blueprint for investors, executives, and innovators looking to capitalize on one of the most vital, yet often overlooked, markets in the technology ecosystem.

\*\*\*

## Part 1: A €4.5 Billion Booming Market: The Panorama of Multi-dimensional Data Indexing SaaS

[PLACEHOLDER - YOUR MARKET URL]

The Multi-dimensional Data Indexing SaaS market represents a specialized but fundamentally crucial segment within the broader data analytics and management industry. Our analysis reveals it's a space defined by immense scale, rapid technological evolution, and powerful demand drivers. It operates at the intersection of Big Data, cloud computing, and artificial intelligence, making its health and trajectory a bellwether for the digital economy at large.

The core value proposition is clear and compelling: optimizing data retrieval and query performance through advanced indexing techniques, delivered via scalable, cloud-based SaaS platforms. As businesses worldwide migrate their data lakes to the cloud and intensify their reliance on AI, the need for solutions that can make sense of this data—quickly and cost-efficiently—has become non-negotiable.

### Market Size and Growth: A Strong and Sustained Trajectory

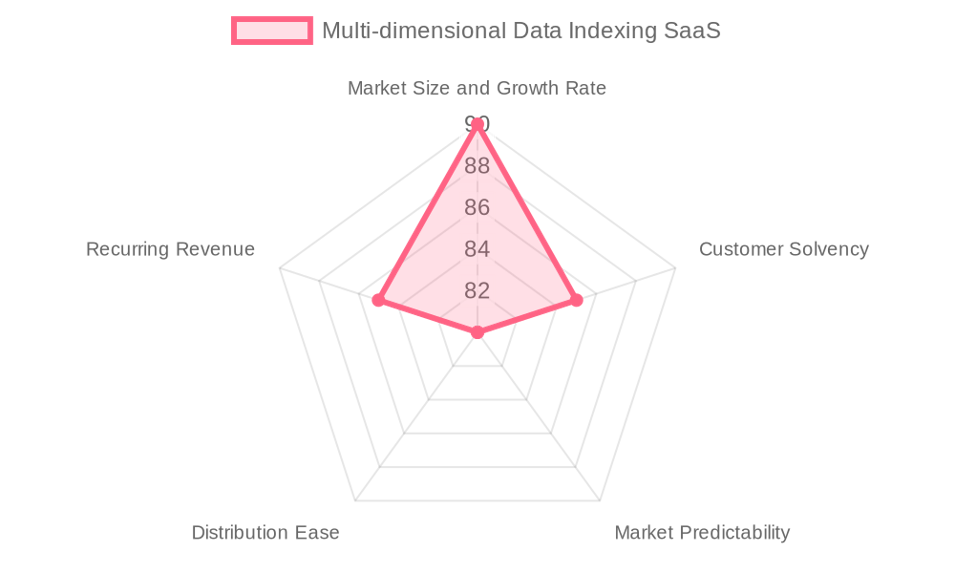

Our intelligence confirms the market's robust financial footing. The **Total Addressable Market (TAM)** for multi-dimensional data indexing SaaS is currently estimated at **€4.5 billion**. This significant valuation is underpinned by a strong projected **year-over-year growth rate of 22%**. This growth isn't speculative; it's fueled by tangible, macro-level shifts.

The calculation of this TAM is derived from the global cloud analytics software market, a titan valued at approximately €70 billion in 2024. Our analysis, informed by reports from Gartner, IDC, and Forrester, attributes about 6-7% of this larger market specifically to advanced indexing SaaS technologies. The key drivers are the exponential growth of data volumes and the escalating demand for real-time decision-making and efficient AI model training, which traditional indexing methods can no longer support effectively.

### A Market of Three Distinct Segments

The market is not a monolith. Its €4.5 billion TAM is comprised of three primary segments, each with unique characteristics, needs, and purchasing behaviors.

**1. Enterprise Data Analytics Optimization (50% of TAM - €2.25 Billion)**

This segment represents the largest piece of the market, driven by Fortune 1000 companies and data-intensive sectors like finance, telecommunications, and retail. These organizations operate vast, complex data lakes and face two primary pain points: **sluggish query response times** that impact business intelligence and AI initiatives, and **high cloud compute costs** stemming from inefficient data processing.

Their purchasing behavior is characterized by an extended buying cycle, typically lasting **3 to 6 months**, involving multiple stakeholders from the CIO and Head of Data Engineering to Data Architects. Decisions hinge on proven ROI, particularly in query speed and cost reduction, and seamless compatibility with their existing open data platforms like Apache Spark or Google BigQuery. The go-to-market motion here is high-touch, relying on enterprise direct sales, in-depth demos, and thought leadership to build trust and demonstrate value.

**2. Midmarket and SMB Data SaaS Users (30% of TAM - €1.35 Billion)**

Growing at an impressive **25% YoY**, this segment is the market's fastest-growing frontier. It includes tech startups and medium-sized businesses in sectors like e-commerce and health tech. These companies are increasingly adopting cloud data platforms but often lack large, dedicated data engineering teams. Their primary need is for affordable, easy-to-implement solutions that boost query efficiency and make them "AI-ready" without requiring a major infrastructure overhaul.

Their buying cycle is significantly shorter, often **1 to 3 months**, and driven by direct product evaluation. Decision-makers, such as Founders and Heads of IT, prioritize ease of integration, demonstrable cost savings, and vendor reliability. The most effective GTM channels are self-service, including online demos, free trials converting to paid subscriptions, and strong community engagement in forums like Slack.

**3. Cloud Data Platform Vendors and Partners (20% of TAM - €0.9 Billion)**

This segment consists of the cloud vendors and data platform integrators themselves. Their motivation is to augment their own offerings with advanced indexing capabilities to differentiate their platforms and increase customer stickiness. They are not end-users in the traditional sense but rather strategic partners seeking to embed or bundle third-party indexing solutions.

The purchase cycle here is a partnership and integration-oriented process that can last **6 months or more**. Key decision-makers include the Head of Partnerships and Platform Product Managers. Decisions are based on technical alignment, API compatibility, and the potential for a joint go-to-market strategy. This channel, while slower, offers significant scaling opportunities through co-marketing and enterprise agreements.

### Key Evolutions and Emerging Trends

Our AI-augmented analysis detects several signals shaping the market's future. The **shift to open data platforms** like Apache Spark is a major tailwind, as it increases data heterogeneity and the need for sophisticated optimization layers. Simultaneously, the **increasing use of AI and machine learning** is a powerful demand catalyst. As Qbeast’s own value proposition highlights, accelerating AI model training by over 62% is a game-changing outcome that drives urgent adoption.

On the regulatory front, compliance with **data privacy regulations like GDPR** and adherence to **cloud data sovereignty laws** are becoming critical product features. SaaS providers must ensure their indexing solutions support robust data governance and, in many cases, offer regional data center presence to win customer trust. These regulatory pressures, while challenging, also create opportunities for well-prepared vendors to establish themselves as trusted partners in a complex landscape. The future will likely belong to those who can balance cutting-edge innovation with the rigorous demands of enterprise-grade security and compliance.

\*\*\*

## Part 2: Three Winning Go-To-Market Playbooks: Conquering Each Market Segment

A €4.5 billion market is an attractive battlefield, but victory requires more than just a powerful product. It demands precise, segment-specific Go-To-Market (GTM) strategies that speak directly to the unique needs, motivations, and buying habits of each customer profile. Our analysis of the GTM dynamics reveals three distinct playbooks, one for each major segment.

### A. The Enterprise Playbook: Mastering the High-Touch, High-Value Sale

[PLACEHOLDER - GTM\_1 IMAGE]

Conquering the enterprise segment, the largest slice of the market, is a game of strategy, trust, and proven value. This is not a segment won through passive inbound alone; it requires a sophisticated, consultative sales approach.

The **ideal customer profile** is a large B2B enterprise with over 1,000 employees and revenues exceeding €500M, typically in finance, telecommunications, or retail. They possess high technological maturity and an annual data analytics budget often exceeding €1M. The **winning persona** to target is the **Chief Information Officer (CIO)** or the **Head of Data Engineering**. Their obsessions are threefold: 1) driving innovation to maintain a competitive edge, 2) controlling and reducing spiraling cloud compute costs, and 3) enabling faster, more reliable data access for critical AI and analytics initiatives.

The acquisition journey is triggered by clear pain points: excessive AWS or other cloud bills, slow query speeds impacting a new AI project, or frustrations with the limitations of existing indexing tools. The **best acquisition channels** are therefore direct and relationship-focused:

1. **Direct Enterprise Sales Teams:** Consultative sellers who can navigate complex organizational charts and build multi-stakeholder consensus.

2. **Targeted LinkedIn Outreach:** For warming up key decision-makers like Data Architects and VPs of IT.

3. **High-Value Content:** Technical whitepapers and ROI case studies that address specific pain points around cost and speed.

4. **Industry Conferences:** For direct engagement and demonstrating thought leadership.

The acquisition process unfolds over **four key stages**: 1) initial discovery and pain agitation, 2) a technical demonstration and proof of concept (POC), 3) ROI and security review with IT and finance leadership, and 4) contract negotiation. The key to conquering this segment is to **quantify value relentlessly**. A detailed ROI calculation showing a Customer Lifetime Value (LTV) far exceeding the Customer Acquisition Cost (CAC) of around **€15,000**, with a clear path to reducing compute expenses by up to 70% or accelerating AI training by 62%, becomes an undeniable proposition.

### B. The Midmarket & SMB Playbook: Winning with Simplicity, Speed, and Community

[PLACEHOLDER - GTM\_2 IMAGE]

The midmarket and SMB segment is the market's growth engine. Winning here requires a different mindset: one focused on low friction, rapid time-to-value, and scalability.

The **ideal customer profile** is a fast-growing tech startup or a medium-sized business (50-500 employees) in e-commerce or health tech, often with recent funding. The **key persona** is frequently the **Founder or Head of IT**, a pragmatic leader obsessed with 1) agility and speed-to-insight, 2) resource conservation and avoiding unnecessary complexity, and 3) empowering their teams a with powerful tools without needing a large data engineering department.

Here, the buying journey is triggered by the practical pains of a growing business: cloud costs are becoming a significant line item, or data queries are too slow to support a new product feature. Because resources are tight, **the most effective acquisition channels** are scalable and self-serve:

1. **Freemium/Free Trial Offerings:** Allowing users to experience the value firsthand with no upfront commitment.

2. **Product-Led Content:** Online tutorials and step-by-step guides, especially on YouTube, that demonstrate ease of use.

3. **Community Engagement:** Actively participating in Slack communities and other forums where data analysts and developers seek peer recommendations.

4. **Targeted Digital Ads:** Focusing on platforms like YouTube to reach decision-makers who are actively researching solutions.

The acquisition process is much faster: 1) discovery through content or community, 2) a quick self-service trial or demo, 3) a value-based decision, and 4) online subscription. The key to winning this segment is to **eliminate friction**. The messaging must emphasize simplicity ("no infrastructure changes required"), clear cost savings, and the ability to "punch above their weight" in AI and analytics. A Free Trial to Paid Conversion Rate of **25%** is a strong benchmark for success in this product-led motion.

### C. The Partner Playbook: Scaling Through the Ecosystem

[PLACEHOLDER - GTM\_3 IMAGE]

The partner segment offers a powerful force multiplier. The goal is not to sell _to_ these cloud data platform vendors but to sell _through_ them.

The **ideal partner profile** is a cloud platform provider or a major data platform integrator with a strong ecosystem and a strategic focus on augmenting their analytics capabilities. The **target persona** is the **Head of Partnerships or a Platform Product Manager**. Their core obsessions are: 1) differentiating their platform from competitors, 2) increasing platform "stickiness" and reducing customer churn, and 3) creating new revenue streams through a richer ecosystem.

Engagement is triggered by strategic imperatives: a competitor announces a new embedded performance feature, or major customers begin requesting better native query acceleration. The "sale" is a negotiation of a strategic alliance. **The best channels** are therefore relationship-based:

1. **Direct Business Development:** Strategic outreach to partnership leaders.

2. **Industry Events & Cloud Summits:** Networking and building relationships at key conferences.

3. **Co-Branded Content:** Joint whitepapers or webinars that demonstrate the combined value proposition.

4. **Technical Evangelism:** Engaging with their developer community to build grassroots demand for an integration.

The process is long and strategic: 1) strategic alignment and value proposition mapping, 2) technical deep-dive and API compatibility assessment, 3) joint GTM and revenue-sharing negotiation, and 4) co-marketing and sales enablement. The key to winning this segment is to present a **low-risk, high-reward partnership**. This means demonstrating seamless technical integration, a clear path to joint revenue, and a commitment to shared success. Success is measured not in single deals, but in the long-term revenue influence generated through the partner's vast customer base.

\*\*\*

## Part 3: The Power Dynamic: Who Truly Controls the Multi-dimensional Data Indexing SaaS Market?

Understanding a market requires more than just sizing it; it requires mapping the invisible forces of competition and influence. In the multi-dimensional data indexing space, a fierce contest is underway between established titans and agile innovators. The question is not just who has the best technology, but who has the market power to dictate terms.

### The Value Chain and Locus of Power

[PLACEHOLDER - COMPANY MAP IMAGE]

The value chain in this market is intricate. It begins with foundational **cloud infrastructure providers** (e.g., AWS, Google Cloud), who wield significant power as essential suppliers. Upon this foundation sit the **open data platforms** (e.g., Apache Spark, BigQuery), which have become the de facto standard, giving them leverage. The **Multi-dimensional Data Indexing SaaS providers**, like Qbeast, insert themselves as a critical optimization layer on top of these platforms. Their patented technology creates value by making the entire stack more efficient. Finally, **customers**—from large enterprises to SMBs—exert their own power through their purchasing decisions and demand for performance and ROI.

Our analysis, leveraging Porter's Five Forces framework, suggests that the **bargaining power of customers is high**. They face moderate switching costs but can easily compare alternatives, especially in the midmarket. The **rivalry among existing competitors is also high**, with established players like Snowflake and Databricks investing heavily in marketing and R&D. While the barriers to entry are moderate due to the technical complexity and need for patented IP, the real power in this market appears to reside with two groups: the **dominant cloud platforms** that control the underlying ecosystem, and the **innovators whose technology becomes indispensable**, creating a strong "gravity" that pulls customers and partners into their orbit.

### The Two Axes of Differentiation

In this competitive landscape, companies battle along two primary axes of differentiation:

1. **Innovation in Indexing Technology:** This is the technical heart of the market. It's not just about having an index; it's about the sophistication of the algorithms. Differentiation comes from developing patented, AI-optimized techniques that deliver quantifiable leaps in performance—faster queries, accelerated AI training, and dramatic cost reductions. This dimension is about pure product superiority and the ability to solve a customer's technical problem in a way no one else can.

1. **Market Reach and Go-To-Market Effectiveness:** This is the commercial muscle. A groundbreaking technology is useless if it cannot reach the right customers. This axis measures a company's ability to execute across different segments, whether through a high-performing enterprise sales force, a frictionless self-service platform for SMBs, or a savvy partnership team that can build a powerful ecosystem.

The core tension in the market is the interplay between these two axes. Can a company with superior technology but limited market reach outmaneuver a well-entrenched giant with a slightly inferior but "good enough" product? Our analysis suggests that long-term leadership will belong to those who can achieve excellence on both fronts.

### Mapping the 10 Key Players

[PLACEHOLDER - COMPETITION QUADRANT URL]

Our analysis positions the key competitors based on their innovation and market effectiveness, revealing a clear structure of Leaders, Challengers, Specialists, and Pure Players.

- **Market Leaders:** Companies like **Snowflake** (over $1B revenue) and **Databricks** (hundreds of millions in revenue) demonstrate high performance on both axes. They combine robust, innovative platforms with powerful, extensive GTM machines, allowing them to dominate the lucrative enterprise segment.

- **Specialists:** A firm like **Dremio** (under $100M revenue) exemplifies this category. It boasts strong technological innovation and is highly regarded for its open data lake integrations, but has a more limited market reach than the leaders, focusing intensely on midmarket self-service.

- **Challengers:** This group includes companies like **Qubole** (under $100M revenue) and **Starburst Data** (under $50M revenue). They possess solid market reach, particularly in the enterprise (Qubole) or midmarket (Starburst), but their level of core indexing innovation is currently more moderate compared to the top leaders and specialists.

- **Pure Players & Trend Setters:** This includes highly innovative open-source projects or companies built around them, such as **Apache Pinot** or **Presto**. They have immense disruption potential and are revered by developers, but often have lower commercial traction and market execution capabilities. **Tabular**, recently acquired by Databricks for a reported $1 billion, was a prime example of a trend setter with immense disruptive IP that was ultimately absorbed by a market leader.

This mapping reveals a dynamic battlefield where leaders are constantly warding off highly focused specialists and well-funded challengers, while also keeping an eye on disruptive open-source technologies that could shift the landscape.

### D. A Closer Look at the Leaders: The Databricks Strategy

The leaders in this space are a formidable group of technology giants who have set the standard for cloud data analytics. This cohort includes **Databricks, Snowflake, Amazon Web Services, Google Cloud Platform, Microsoft Azure, Palantir, Cloudera, Teradata, Oracle, and IBM**. They dominate through a combination of massive scale, vast resources, and deeply entrenched customer relationships.

Let's focus on **Databricks** as a prime example of leadership strategy. Employing over 3,000 people and generating hundreds of millions in revenue, Databricks has built its dominance by tightly integrating AI-optimized multi-dimensional indexing with its core Apache Spark-based platform. Their key strategic lever is the **acceleration of AI/ML workflows**. By positioning themselves as the essential platform for data scientists and ML engineers, they have captured a high-value, high-growth segment of the market. Their GTM is a powerful blend of top-down enterprise sales, targeting CIOs and Chief Data Officers, and bottom-up community engagement, building a loyal following among developers and data scientists. This dual approach, combined with continuous innovation (like the acquisition of Tabular), makes them a powerful and enduring leader.

### E. The Challengers' Gambit: The Rise of Starburst and Others

While the leaders command the market, a vibrant ecosystem of challengers is actively working to disrupt the status quo. This group includes agile and innovative companies such as **Starburst, Dremio, Tabular (now part of Databricks), Onehouse, LakeFS, ClickHouse, Firebolt, DataPelago, BigQuery Omni, and Trino**. Their strategies often revolve around exploiting niches the leaders are slower to address.

Let's analyze the lead challenger, **Starburst Data**. With around 250 employees and revenue under $50 million, Starburst's strategy is not to out-innovate Databricks on core AI algorithms, but to out-compete on flexibility and cost-effectiveness. They focus on providing a query engine that can sit on top of _any_ data source, championing an open-ecosystem approach that appeals to midmarket customers wary of vendor lock-in. Their GTM emphasizes ease of integration and a lower total cost of ownership. This "accessible" positioning allows them to carve out a significant market share without engaging in a head-to-head technology race with the leaders. The primary threat they and other challengers pose is one of fragmentation and price erosion, forcing the leaders to defend their value proposition and justify their premium pricing constantly.

\*\*\*

## Part 4: A Sector Under the Microscope: SWOT Analysis of Multi-dimensional Data Indexing SaaS

Every market, no matter how promising, is a complex interplay of strengths, weaknesses, opportunities, and threats. A strategic assessment requires an unvarnished look at these four dimensions. Our AI-powered SWOT analysis digs beneath the surface to reveal the structural dynamics that will define the winners and losers in the coming years.

### STRENGTHS: The Market's Solid Foundation

[PLACEHOLDER - MARKET SWOT URL]

The Multi-dimensional Data Indexing SaaS market is built on a bedrock of powerful structural strengths that create a favorable environment for growth and innovation.

- **Robust Market Fundamentals:** The most evident strength is the sheer scale and growth of the market. A **€4.5 billion Total Addressable Market growing at 22% annually** provides ample room for multiple players to thrive. AI's proliferation acts as a powerful accelerant, exponentially increasing the need for the very solutions this market provides.

- **Powerful Demand Drivers:** The demand is not speculative; it's driven by fundamental business needs. The global explosion of data in cloud data lakes, coupled with the urgent push for AI-driven insights, creates an inexorable pull for technologies that can **reduce query latency and cut cloud compute costs**.

- **High Innovation Velocity:** This is a market where intellectual property matters. The emphasis on **patented multi-dimensional indexing algorithms** creates a strong competitive moat. AI further enhances this, powering a virtuous cycle of continuous algorithm improvement that sustains a provider's technological edge.

- **Strong Value Chain Structure:** The market benefits from well-defined and accessible distribution channels. The ability to reach customers through **direct enterprise sales, online self-service platforms, and strategic partner ecosystems** allows companies to tailor their GTM to different segments effectively.

- **Favorable Financial Dynamics:** The SaaS subscription model is a core strength, providing **predictable, recurring revenue**. This predictability, combined with strong performance, attracts significant investment and premium valuations, with IRR benchmarks around 14-16% and top performers exceeding that.

- **Sticky Ecosystem Integration:** Compatibility with dominant open data platforms like Apache Spark and Google BigQuery is a major strength. Deep integration builds **ecosystem stickiness**, which increases switching costs for customers and creates a barrier for new entrants who lack these established connections.

### WEAKNESSES: The Market's Inherent Challenges

Despite its strengths, the market is not without its vulnerabilities. These are the critical challenges that every player must navigate.

- **High Integration Complexity:** While the goal is seamless integration, the reality can be complex. Onboarding a new indexing solution into a sprawling enterprise data architecture can be a significant undertaking, leading to **long sales cycles (3-6 months)** and customer skepticism.

- **Significant Capital and Talent Requirements:** Building and maintaining a leading-edge indexing platform is expensive. It requires substantial upfront investment in R&D and cloud infrastructure, as well as a team of highly specialized (and scarce) data engineers and scientists. This creates a high bar for profitability, especially for smaller players.

- **Moderate Switching Costs:** While integration creates some stickiness, the cloud-native, SaaS nature of these products means switching is not impossible. A competitor offering a significantly better price-to-performance ratio can lure customers away, especially in the cost-sensitive midmarket.

- **Dependency on Cloud Providers:** The entire market is built on the infrastructure of a few giants like AWS, Google Cloud, and Azure. This creates a **dependency risk**, as any pricing changes or policy shifts by these providers can directly impact the profitability and operations of the SaaS vendors.

- **Legacy System Inertia:** In the large enterprise segment, many organizations still rely on entrenched on-premise solutions. The organizational inertia and perceived risk of migrating away from these legacy systems can significantly slow the adoption of new SaaS solutions.

- **Communication Complexity:** The technical nature of multi-dimensional indexing can make the value proposition difficult to communicate clearly. Vendors must overcome a wall of jargon and technical skepticism to build trust and convince non-technical stakeholders of the ROI.

### OPPORTUNITIES: The Catalysts for Future Growth

[PLACEHOLDER - MARKET SWOT URL 2]

Where weaknesses present challenges, opportunities offer pathways to exponential growth. The market is ripe with potential for savvy players.

- **Explosive Growth in Emerging Segments:** The **midmarket and SMB SaaS user segment** is the single greatest opportunity. Their rapid adoption of cloud analytics, combined with their need for low-complexity, cost-effective solutions, creates a massive, underserved market that is growing faster than the enterprise segment.

- **AI-Enabled Technological Leaps:** The use of AI is not just a demand driver; it's an opportunity for product innovation. AI can be used to create self-tuning indexing algorithms, predict query performance, and automate optimization, creating a new echelon of "intelligent" indexing solutions that further widens the performance gap.

- **Ecosystem and Partnership Expansion:** There is a vast opportunity in building deeper alliances with cloud vendors and platform integrators. Co-marketing, bundling, and marketplace listings can unlock access to thousands of potential customers and significantly lower customer acquisition costs.

- **Geographic Expansion:** While North America and Europe are the primary markets today, there is huge untapped potential in **Asia-Pacific and other emerging markets** where cloud adoption is accelerating rapidly. A targeted geographic expansion strategy could unlock a new wave of growth.

- **Sustainability as a Differentiator:** Data centers consume enormous amounts of energy. An optimized indexing solution that dramatically reduces computational load and, by extension, energy consumption, can be positioned as a "green" technology. This appeals to the growing number of enterprises with strong Environmental, Social, and Governance (ESG) mandates.

- **Business Model Innovation:** While subscriptions are the norm, there are opportunities to innovate with **consumption-based pricing models** or freemium tiers that have a clear path to monetization. This can further reduce the barrier to entry for smaller customers and accelerate adoption.

### THREATS: The External Risks to Consider

Finally, every market faces external threats that are largely outside of any single company's control. Awareness and mitigation are key.

- **Intense Competitive Rivalry:** The presence of heavily capitalized incumbents like **Snowflake and Databricks** represents a constant threat. Their massive marketing budgets and existing customer bases can make it difficult for smaller players to gain traction.

- **Technological Disruption:** The pace of innovation is both a strength and a threat. A new, paradigm-shifting approach to data indexing could emerge from an open-source project or a stealth startup, potentially rendering existing patented algorithms obsolete.

- **Commoditization and Price Pressure:** As the market matures, there is a persistent threat of commoditization. Competitors may engage in aggressive price wars, eroding margins and forcing companies to compete on cost rather than value.

- **Regulatory Uncertainty:** The global regulatory landscape for data privacy and sovereignty is constantly shifting. A sudden change in policy, such as new restrictions on cross-border data flows, could significantly impact the business models of global SaaS providers.

- **Cybersecurity Risks:** As critical components of the data infrastructure, indexing platforms are high-value targets for cyberattacks. A major data breach at any one provider could damage trust in the entire SaaS market segment.

- **Economic Volatility:** A global economic downturn could lead to cuts in IT spending, slowing down sales cycles and reducing demand, particularly for large, capital-intensive projects in the enterprise segment.

**Strategic Insight:** The primary tension in this market is between **innovation-led value creation** and the **risk of competitive commoditization**. The strategic imperative is to use AI-driven innovation not just as a feature, but as a core defense, continuously widening the performance and efficiency gap to a point where the value proposition is undeniable, justifying premium pricing and insulating the business from pure cost-based competition.

\*\*\*

## Part 5: Conceptualizing AI Agents for the Multi-dimensional Data Indexing SaaS Market

The transformative potential of Artificial Intelligence extends beyond its role as a demand driver for indexing solutions; it can be woven into the very fabric of a company's operations. By conceptualizing dedicated AI agents, we can envision a future where every facet of the value chain is augmented, optimized, and automated. These are not mere chatbots; they are sophisticated systems designed to work alongside human experts, amplifying their capabilities and driving asymmetric advantages.

It is important to emphasize that the following are **conceptual ideas** intended to illustrate a strategic direction, not descriptions of existing products.

### A. Two High-Impact AI Agent Concepts

Here are two examples of specialized AI agents that could deliver game-changing value in this market.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

**1. Agent Concept: "Max - AI-Driven Indexing Algorithm Optimizer"**

- **Function:** This agent acts as a tireless R&D partner. It continuously analyzes real-time query performance, data ingestion patterns, and system load across the entire customer base. Using this data, it runs thousands of simulations in a virtual environment to discover and recommend optimizations to the core multi-dimensional indexing algorithms.

- **Augmented Job Title:** It would directly augment the **Data Engineering and R&D Teams**. Instead of spending weeks manually testing and tuning new algorithm parameters, these teams would be presented with AI-vetted recommendations, complete with predicted performance gains and risk analyses.

- **Problem Solved:** It directly tackles the threat of technological obsolescence and the high cost of R&D. It automates the innovation cycle, ensuring the core technology remains state-of-the-art.

- **Concrete Use Case:** A large e-commerce client experiences a sudden shift in customer behavior, leading to new query patterns that degrade performance. Max detects this anomaly, identifies the suboptimal indexing parameters, and recommends a specific algorithmic tweak. The R&D team validates and deploys the change in hours instead of weeks, preventing a negative impact on the customer's business.

- **KPIs Impacted:** Query Performance SLA Compliance (improves), R&D Spend Ratio (optimizes), Customer Churn Rate (reduces).

- **Game-Changer Impact:** It transforms innovation from a periodic, human-led effort into a continuous, automated process, creating a nearly insurmountable technological moat.

**2. Agent Concept: "Sage - Predictive Market Analytics and Customer Segmentation Engine"**

- **Function:** Sage is a strategic marketing and sales intelligence agent. It ingests a vast array of data—from CRM activity and customer usage logs to competitive pricing announcements and job postings (as a signal of intent). It then uses predictive models to identify emerging customer segments, pinpoint high-propensity leads, and even suggest dynamic pricing strategies.

- **Augmented Job Title:** It augments the **Sales and Marketing Teams**. It provides them with a prioritized list of leads, complete with talking points tailored to their specific, AI-identified pain points, dramatically increasing conversion rates.

- **Problem Solved:** It directly addresses the weakness of long, expensive enterprise sales cycles and the challenge of efficiently penetrating the fast-growing midmarket segment.

- **Concrete Use Case:** Sage analyzes market signals and detects a cluster of mid-sized health tech companies all recently receiving Series B funding and hiring for "Data Analyst" roles. It flags this as a high-potential micro-segment. It then pushes this list to the sales team with a recommended outreach campaign focused on "AI-readiness for regulatory compliance," a key pain point for that specific niche.

- **KPIs Impacted:** Customer Acquisition Cost (CAC) (reduces), Sales Cycle Length (shortens), Monthly ARR Growth Rate (increases).

- **Game-Changer Impact:** It shifts the GTM motion from reactive and broad to predictive and surgical, allowing a company to outmaneuver competitors by reaching the right customers with the right message before anyone else.

### B. A Broader Arsenal of AI Agent Concepts

The potential extends far beyond these two examples. Here is a list of ten other conceptual agents that could address specific challenges and opportunities across the value chain.

[PLACEHOLDER - MARKET SWOT PRIORITY URL]

1. **Echo - AI-Powered SaaS Integration and Deployment Assistant:** Augments Customer Success teams by automating and guiding new clients through complex integrations.

2. **Sentinel - AI-Driven Compliance and Data Privacy Monitoring System:** Augments Compliance Officers by continuously monitoring data usage against regulations like GDPR.

3. **Bridge - AI-Enhanced Customer Engagement and Retention Platform:** Augments Customer Success Managers by using predictive analytics to identify churn risks and automate proactive outreach.

4. **Futura - Demand Forecasting and Economic Impact Analyzer:** Augments Finance and Sales Planning by forecasting demand based on economic indicators to optimize resource allocation.

5. **Optima - Multi-Cloud Resource Allocation Optimizer:** Augments Cloud Infrastructure Managers by dynamically shifting workloads between cloud providers to minimize costs.

6. **Guardian - AI-Powered Cyber Threat Detection and Response:** Augments Security Operations teams by using anomaly detection to identify and respond to potential breaches in real-time.

7. **Liaison - AI-Enabled Clear Communication Assistant:** Augments Technical Writers by auto-generating clear, easy-to-understand documentation for complex features.

8. **Scout - Competitive Landscape Monitoring System:** Augments Strategy teams by providing real-time alerts on competitor moves, pricing changes, and feature launches.

9. **Prime - Energy-Aware Indexing Algorithm Designer:** Augments R&D and Sustainability teams by designing algorithms that minimize energy consumption.

10. **Voice - AI-Powered Ecosystem Partner Collaboration Facilitator:** Augments Partnership Managers by identifying and optimizing joint GTM opportunities with ecosystem partners.

### C. The Ultimate Vision: An Interdependent System of Agents

[PLACEHOLDER - MARKET AGENT SYSTEM URL]

The ultimate evolution of this concept is not a collection of siloed agents, but a fully integrated, interdependent **AI agent system**. In this vision, a master **Orchestrator Agent**, the **Harmony Tech Command Center**, would oversee the entire value creation chain.

This Master Orchestrator would augment the **Chief Data Officer or Data Platform Manager**, providing a single pane of glass view of the entire business. It would delegate tasks to the five specialized agents that map directly to the value chain:

- **Integration Efficiency Agent (Nexus Optima):** Handles seamless deployment.

- **Query Acceleration Agent (Turbo Quest):** Optimizes query speed.

- **Cost Management Agent (Frugal Sentinel):** Controls cloud spend.

- **Data Platform Efficiency Agent (Core Pulse):** Ensures overall system health.

- **AI Training Acceleration Agent (Neuron Surge):** Speeds up ML workflows.

The synergy here is key. The Cost Management Agent could inform the Query Acceleration Agent that a certain optimization is too expensive, prompting it to find a more efficient solution. The Integration Agent's findings would feed directly into the Platform Efficiency Agent's models. Coordinated by the Harmony Tech Command Center, this system would create a self-optimizing, self-healing business operation that learns and adapts in real-time. This is the futuristic vision of a company not just _using_ AI, but being fundamentally _powered_ by it.

\*\*\*

## Conclusion: A Strategic Summary and Your Next Steps

Our deep dive into the Multi-dimensional Data Indexing SaaS market reveals a landscape of immense opportunity, fraught with strategic challenges. The market, valued at **€4.5 billion and growing at a formidable 22% annually**, is a critical enabler of the AI revolution. Its segmentation into enterprise, midmarket, and partner channels demands tailored Go-To-Market strategies, moving from high-touch consultative sales for large corporations to frictionless, product-led growth for agile SMBs.

The competitive arena is a dynamic duel. Established leaders like **Databricks** and **Snowflake** leverage scale and deep integration to defend their dominance, while a vibrant class of challengers like **Starburst** and **Dremio** carves out niches through flexibility and cost-effectiveness. The core tension lies between profound technological innovation and effective market execution. Success is not guaranteed by patents alone; it requires a masterful commercial strategy. The market's structural strengths—powerful demand, high innovation, and recurring revenue models—are counterbalanced by weaknesses like integration complexity and intense capital requirements. The path forward for any player in this space involves leveraging AI not just as a product feature, but as a core operational principle to automate innovation, streamline customer acquisition, and build a resilient, adaptive organization.

The market is moving towards more intelligent, self-optimizing, and deeply integrated solutions. The most significant opportunities lie in serving the burgeoning midmarket with accessible yet powerful tools and in leveraging AI to create defensible technological moats. Artificial intelligence will be the key differentiator, separating the companies that simply participate in this market from those that will come to define it. The future belongs to the swift, the strategic, and the AI-augmented.

If you are interested in this topic you can follow these next steps:

1️⃣Download below the full Multi-dimensional Data Indexing SaaS market study in pdf format

[PLACEHOLDER - PDF DOWNLOAD LINK]

2️⃣ Get additional insights of this market by reading our memo of an interesting company in this market called Qbeast.

[PLACEHOLDER - QBEAST MEMO LINK]

3️⃣ If you want us to build a custom AI system and dedicated AI agents for your business, book a strategic discussion with an AI Partner: https://forms.proplace.co/meet