.png)

The Multi-dimensional Data Indexing SaaS market by our Market Intelligence AI agent

Of course. Here is the comprehensive, SEO-optimized blog post, generated in English based on the provided data and adhering to all specified rules and formatting.

\*\*\*

# The Complete 2025 Market Analysis: Multi-dimensional Data Indexing SaaS

**Meta Description:** A deep-dive analysis of the Multi-dimensional Data Indexing SaaS sector. Explore market size, go-to-market strategies, competitive dynamics, and the AI-driven opportunities revealed by automated intelligence. A definitive guide for investors and CEOs.

**Target Keywords:** Multi-dimensional Data Indexing SaaS, AI market analysis, data analytics optimization, cloud cost reduction, multi-dimensional indexing 2025, AI agents for data indexing, Databricks analysis, Snowflake competition.

\*\*\*

### Introduction

The Multi-dimensional Data Indexing SaaS market is emerging as a critical and high-growth theater of innovation within the broader data analytics landscape. As organizations grapple with the exponential growth of data housed in complex cloud data lakes, the ability to query this information quickly and cost-effectively has become a paramount competitive differentiator. This market is not merely about storage; it is about activating data at speed and scale to fuel real-time decision-making, power sophisticated AI models, and unlock tangible business value.

This analysis, powered by our Market Intelligence AI agent, offers a comprehensive examination of this dynamic sector. We will move beyond surface-level observations to provide a granular, data-driven perspective forged from the methodical synthesis of market signals, competitive intelligence, and strategic frameworks. We will first dissect the market's structure, sizing its €4.5 billion potential and segmenting its core customer profiles. Subsequently, we will architect winning Go-To-Market playbooks tailored for each distinct segment.

Following this, we will map the competitive arena, identifying the true power brokers and the disruptive challengers poised to reshape the hierarchy. A rigorous SWOT analysis will then uncover the structural strengths and latent vulnerabilities of the market, revealing untapped opportunities and looming threats. Finally, we will explore the transformative potential of specialized AI agents designed to revolutionize every facet of the value chain. This article is your definitive strategic brief for understanding, navigating, and capturing value in the Multi-dimensional Data Indexing SaaS market of tomorrow.

\*\*\*

## Section 1: A Complete Overview of the Multi-dimensional Data Indexing SaaS Market

The Multi-dimensional Data Indexing SaaS market represents a specialized yet pivotal segment of the data management industry. Its core purpose is to reorganize vast data lakes using advanced, often patented, algorithms to dramatically accelerate query speeds and slash the associated cloud compute costs. This sector's rapid evolution is directly fueled by the global explosion in data volume and the concurrent rise of AI and machine learning, which demand unprecedented levels of data access efficiency. As open data platforms like Apache Spark and Google BigQuery become ubiquitous, the need for sophisticated, seamless indexing solutions delivered via a flexible SaaS model has become undeniable.

[PLACEHOLDER - YOUR MARKET URL]

### Market Sizing and Projections: A €4.5 Billion Opportunity

Our analysis reveals a robust and rapidly expanding market. The **Total Addressable Market (TAM)** for Multi-dimensional Data Indexing SaaS is currently valued at **€4.5 billion**. This figure is derived from the global cloud analytics software market—estimated at approximately €70 billion in 2024—with an attributable 6-7% share specifically for advanced indexing technologies. This calculation is informed by leading analyst reports from Gartner, IDC, and Forrester, which underscore the burgeoning demand for real-time data querying capabilities.

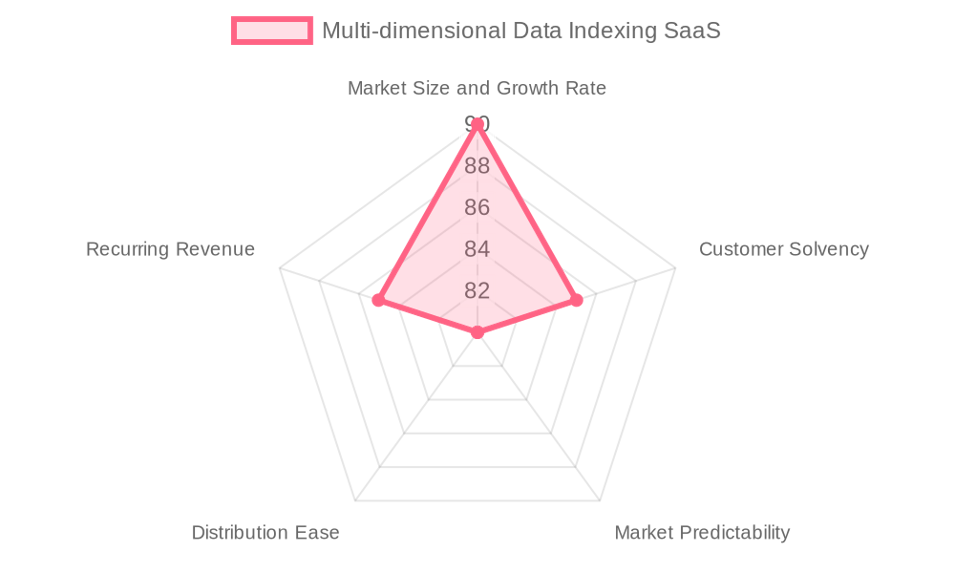

The market is projected to grow at a compelling **22% year-over-year (YoY)**. This trajectory is underpinned by the relentless expansion of cloud data lakes and the increasing integration of AI, which necessitates faster and more efficient data preparation and training cycles. The market's attractiveness is further evidenced by its high scores across key evaluation criteria, including size and growth (90/100), customer solvency (85/100), and predictability (80/100), culminating in an overall market attractiveness score of 85 out of 100. This indicates a lucrative, stable, and fast-growing opportunity ripe for strategic investment.

### Deep Dive into Key Market Segments

The market is not monolithic; it comprises distinct segments with unique needs, behaviors, and growth drivers. Understanding these nuances is critical to unlocking value.

#### Segment 1: Enterprise Data Analytics Optimization

Constituting the largest portion of the market, this segment represents approximately **50% of the TAM**, or **€2.25 billion**, and is growing at a solid **20% YoY**. Its key characteristics include the management of massive, complex data lakes and a critical requirement for high-performance, multi-dimensional indexing. The target audience is primarily Fortune 1000 companies in data-intensive sectors like finance, telecommunications, and retail. These organizations are driven by two primary pain points: escalating cloud compute costs from inefficient data queries and sluggish query response times that hamstring analytics teams and delay AI model training. Their decision-making process is rigorous, often involving a 3-6 month buying cycle with multiple stakeholders, including CIOs and Data Architects. The key decision factors are seamless compatibility with existing platforms like Apache Spark or BigQuery and a demonstrable ROI on both speed improvement and cost reduction.

#### Segment 2: Midmarket and SMB Data SaaS Users

This segment, representing **30% of the TAM (€1.35 billion)**, is the fastest-growing at an impressive **25% YoY**. It is characterized by the accelerating adoption of cloud data platforms and a sharp focus on agility and cost optimization. The ideal customers are tech startups and medium-sized businesses in fields like e-commerce and health tech. Their primary pain points stem from a lack of deep, in-house data engineering expertise for database tuning and an urgent need to shorten data-to-insight timelines to maintain a competitive edge. Their purchase behavior reflects this agility; buying cycles are shorter (1-3 months) and often driven by direct product evaluation through freemium models or self-service demos. For them, ease of integration without requiring infrastructure changes and clear, immediate cost savings are paramount.

#### Segment 3: Cloud Data Platform Vendors and Partners

This ecosystem-focused segment makes up the remaining **20% of the TAM (€0.9 billion)** and is growing at **15% YoY**. It includes major cloud vendors and data platform integrators who seek to augment their own offerings with advanced indexing capabilities. Their primary driver is competitive differentiation and increasing the "stickiness" of their platforms by embedding powerful analytics performance features. The buying journey here is a partnership and integration cycle, often lasting over six months. Decision-making, led by Heads of Partnerships and Platform Product Managers, hinges on technical alignment, API compatibility, and the potential for a joint go-to-market strategy.

### Key Evolutions and Emerging Trends

Our analysis highlights several transformative shifts shaping the market's future:

- **Technological Evolution:** The rate of innovation is rapid. The most significant trend is the rise of **AI-optimized indexing**, which goes beyond simple query speed to directly accelerate AI model training, with some solutions demonstrating a **62%+ reduction in training time**. This creates a highly disruptive potential, transforming slow, expensive analytics into a fluid, cost-efficient workflow.

- **Behavioral Evolution:** A clear **shift to open data platforms** is underway. This increases data heterogeneity and volume, thus amplifying the demand for superior indexing solutions that can handle complexity without vendor lock-in. Customers are increasingly seeking interoperable, modular tools that enhance their existing data stack rather than replacing it.

- **Regulatory Evolution:** The regulatory landscape, while a potential hurdle, also creates opportunities. Data privacy regulations like **GDPR** necessitate indexing solutions that are compliant by design, while **cloud data sovereignty laws** are driving demand for SaaS providers with a robust regional data center presence, adding a layer of trust and local compliance.

Based on these dynamics, our AI-driven forecast suggests the market will continue its strong growth trajectory, with the midmarket segment likely outperforming projections as self-service tools mature. The distinction between "data indexing" and "AI acceleration" will blur, becoming a single, integrated value proposition.

\*\*\*

## Section 2: 3 Potentially Winning Go-To-Market Strategies: Conquering Each Market Segment

A one-size-fits-all approach is destined for failure in a market this nuanced. Our analysis of the Go-To-Market (GTM) landscape suggests that victory lies in deploying highly tailored strategies for each of the three core segments. Success requires a deep understanding of each customer's unique profile, pain points, and buying journey.

### A. GTM Playbook for Segment 1: Enterprise Data Analytics Optimization

This segment represents the largest prize but demands a sophisticated, high-touch approach. The goal is to build strategic partnerships with large organizations, navigating complex sales cycles to secure high-value, long-term contracts.

[PLACEHOLDER - GTM\_1 IMAGE]

- **Ideal Customer Profile:** The target is a large enterprise with over 1,000 employees and more than €1B in revenue, typically in the finance, telecom, or retail sectors across North America, Europe, or Asia. These companies possess high technological maturity, with an annual data infrastructure budget between €1M and €5M. Their decision timelines are extended, averaging 3-6 months.

- **The Winning Persona & Their Obsessions:** The key decision-maker is the **Chief Information Officer (CIO)** or a senior data leader like the Head of Data Engineering. Their three core obsessions are:

1. **Cost Reduction:** Relentlessly focused on reducing exorbitant AWS or other cloud compute expenses.

2. **Performance & Speed:** Pressured to eliminate sluggish query times that impede critical business analytics and stall AI initiatives.

3. **Risk Mitigation:** Highly averse to solutions that require disruptive infrastructure overhauls or introduce integration complexity.

- **Top Acquisition Channels:** A multi-pronged strategy is essential.

1. **Direct Enterprise Sales:** Building a dedicated sales team to engage in consultative selling, providing demos, and orchestrating proofs-of-concept.

2. **Thought Leadership on LinkedIn:** Publishing technical whitepapers, ROI case studies, and deep-dive webinars to establish credibility and attract inbound interest from data architects and IT leaders.

3. **Industry Conferences:** Securing speaking slots and exhibition booths at major data and analytics conferences to engage directly with target personas.

4. **Strategic Partnerships:** Co-hosting webinars and creating joint content with established platforms like Databricks or Google BigQuery to leverage their ecosystem.

- **The 4-Step Acquisition Process:** The enterprise buying journey is triggered by budget overruns or significant delays in AI projects. The acquisition process should mirror this reality:

1. **Awareness & Education:** Use LinkedIn Ads and thought leadership to educate CIOs on the hidden costs of inefficient indexing.

2. **Consideration & Proof:** Nurture leads with detailed case studies and offer a non-disruptive proof-of-concept to validate performance claims.

3. **Validation & Buy-In:** Work with data architects and engineering heads to demonstrate seamless integration and build internal consensus.

4. **Procurement & Negotiation:** Engage with the CIO and procurement teams, armed with a clear ROI analysis, to finalize the contract. A Customer Acquisition Cost (CAC) up to €120K can be justified by the high lifetime value (LTV) of these accounts.

- **Key Insight for Conquest:** The winning message for this segment is not just about technology; it's about **de-risked innovation**. Emphasize the seamless, non-disruptive nature of the integration and back it with patented technology and undeniable proof points, such as a **70% reduction in cloud costs** or a **>62% acceleration in AI training**.

### B. GTM Playbook for Segment 2: Midmarket and SMB Data SaaS Users

This segment is all about speed, efficiency, and accessibility. The winning GTM is a product-led growth (PLG) model that empowers users to discover, evaluate, and adopt the solution with minimal friction.

[PLACEHOLDER - GTM\_2 IMAGE]

- **Ideal Customer Profile:** A tech startup or mid-sized business (50-500 employees, €5M-€50M revenue) in e-commerce or health tech, located in North America, Europe, or India. They have medium tech maturity and an annual data budget of €100K-€500K. Decisions are made quickly, within 1-3 months.

- **The Winning Persona & Their Obsessions:** The decision-maker is often the **Founder, Head of IT, or a lead Data Analyst**. Their three main obsessions are:

1. **Simplicity & Self-Service:** Lacking large data engineering teams, they need solutions that are easy to deploy and manage without specialized expertise.

2. **Affordability & ROI:** Operating with tight budgets, they demand a clear and rapid return on investment, often starting with a freemium or low-cost tier.

3. **Speed to Insight:** Their competitive advantage relies on quickly turning data into actionable insights to pivot and grow.

- **Top Acquisition Channels:**

1. **YouTube & How-To Content:** Creating tutorials, onboarding walkthroughs, and demo videos that show how easy the product is to use.

2. **Community Engagement (Slack/Discord):** Building and nurturing a community where users can ask questions, share successes, and get peer support.

3. **Freemium/Free Trial Model:** Offering a no-risk entry point for users to experience the product's value firsthand.

4. **Google Ads:** Targeting long-tail keywords related to "data query optimization for startups" or "reduce BigQuery costs."

- **The 4-Step Acquisition Process:** The trigger is often a startup funding round or the pain of escalating cloud bills.

1. **Discovery:** Potential users find the product through a Google search or a YouTube tutorial.

2. **Evaluation:** They sign up for a free trial or freemium plan and test the core features.

3. **Value Realization:** They experience a tangible improvement in query speed or a reduction in their cloud bill within days.

4. **Conversion:** They upgrade to a paid plan to unlock advanced features or higher usage limits. The target CAC here is significantly lower, around **€15K**, with a high volume of conversions. A 20% freemium-to-paid conversion rate is a strong benchmark.

- **Key Insight for Conquest:** The key to winning the midmarket is to **eliminate friction**. The entire user experience, from discovery to value realization, must be automated, intuitive, and self-service. The message should focus on **"effortless optimization"**—achieving enterprise-grade performance without needing an enterprise-grade team.

### C. GTM Playbook for Segment 3: Cloud Data Platform Vendors and Partners

This GTM strategy is not about selling to end-users but about building a powerful, symbiotic ecosystem. The approach is rooted in business development and strategic alliance-building.

[PLACEHOLDER - GTM\_3 IMAGE]

- **Ideal Customer Profile:** A cloud platform vendor or data integrator (100-2,000 employees, €50M-€500M revenue) with an active partner program. They have high technical sophistication and a strategic partnership budget of €500K-€2M. The decision timeline is long, at 6+ months.

- **The Winning Persona & Their Obsessions:** The key contact is the **Head of Partnerships or Platform Product Manager**. Their primary obsessions are:

1. **Competitive Differentiation:** Constantly seeking unique features to make their platform stand out in a crowded market.

2. **Ecosystem Stickiness:** Increasing the value of their platform to reduce customer churn and drive deeper adoption.

3. **Joint Revenue Growth:** Identifying partners that can create new, joint go-to-market opportunities and drive incremental revenue.

- **Top Acquisition Channels:**

1. **Direct Business Development:** Targeted outreach via email and calls to partnership leaders at key platform companies.

2. **Industry Conference Networking:** Setting up one-on-one meetings at major industry events to discuss strategic alignment.

3. **Co-Branded Content:** Producing technical case studies and joint webinars that demonstrate the value of the integration.

4. **API & Integration Guides:** Publishing detailed documentation that makes it easy for potential partners to evaluate the technical fit.

- **The 4-Step Acquisition Process:** The process is triggered by a platform's need to fill a feature gap or respond to competitive pressure.

1. **Strategic Alignment:** Initial conversations focus on the joint value proposition and technical compatibility.

2. **Technical Deep Dive:** Engineering teams from both sides meet to validate the API and integration workflow.

3. **Joint GTM Planning:** Business development teams collaborate to define the co-marketing strategy, revenue share model, and success metrics.

4. **Formal Agreement & Launch:** Legal teams finalize the partnership agreement, followed by a joint public launch. Success is measured not by CAC, but by partner-influenced revenue, with a target of €8M+ in incremental influence within 90 days of a partnership launch.

- **Key Insight for Conquest:** To win with partners, you must position your technology as a **"strategic force multiplier."** The conversation should transcend features and focus on how your unique, patented IP can help them win their own market battles, differentiate their offering, and create new revenue streams.

\*\*\*

## Section 3: Who Truly Holds Power in the Multi-dimensional Data Indexing SaaS Market?

Understanding the competitive landscape requires moving beyond a simple list of companies. It requires a nuanced analysis of the value chain, the core axes of differentiation, and the underlying power dynamics that determine who captures the most value. In this turbulent ocean, a few large galleons command the seas, but specialized, agile vessels are constantly challenging their dominance.

[PLACEHOLDER - COMPETITION QUADRANT URL]

### A. The Value Chain and the Balance of Power

The value chain in this market begins with foundational **cloud infrastructure providers** (e.g., AWS, Google Cloud, Azure). They hold significant power as suppliers, influencing costs and operational realities. Next are the **open-source data platforms** (e.g., Apache Spark, Trino), which provide the architectural canvas. Their power lies in their widespread adoption, which dictates compatibility requirements.

The core of the value chain consists of the **Multi-dimensional Data Indexing SaaS providers** themselves. These companies integrate their patented algorithms into data lakes to optimize queries. Their power is derived from the uniqueness and performance of their IP. Further down the chain are the **data platform integrators and consultants**, who help enterprises deploy these solutions. Finally, the **end customers**—enterprises and midmarket firms—wield considerable power. Their bargaining power is high due to the availability of multiple solutions and moderate switching costs, especially for cloud-native firms.

Ultimately, the power in this market is consolidating around players who can master two things: **proprietary technology** that delivers undeniable performance gains and a **robust GTM engine** that ensures widespread distribution and ecosystem integration. Companies that control both innovation and market access, like Snowflake and Databricks, currently sit at the apex of the power structure.

### B. The Core Axes of Differentiation

Competition in this market unfolds along two primary axes:

1. **Innovation in Indexing Technology:** This is the bedrock of differentiation. It is not merely about having an indexing solution, but about the sophistication, performance, and uniqueness of the underlying algorithms. This axis measures a company's ability to develop and patent novel approaches that deliver step-change improvements in query speed, cost reduction, and AI training acceleration. A company with high innovation can solve customer pain points in a way that competitors cannot easily replicate. Qbeast's patented technology, for example, which accelerates AI training by over 62%, is a prime example of high differentiation on this axis.

1. **Market Reach and Go-To-Market Effectiveness:** Having brilliant technology is necessary but not sufficient. This axis evaluates a company's ability to effectively access and convert its target customer segments. It encompasses the strength of its enterprise sales force, the efficiency of its self-service/PLG models, the breadth of its partner ecosystem, and the power of its brand. A company with high market reach can scale rapidly and capture market share even with technology that is "good enough" rather than revolutionary.

The primary tension in the market is between these two axes. Pure-play innovators risk being outmaneuvered by distribution giants, while large platforms with massive reach risk being disrupted by nimbler specialists with superior technology.

### C. Mapping the 10 Key Competitors

Our analysis maps the key players into four distinct strategic clusters based on their innovation and market reach:

- **Market Leaders (High Innovation, High Reach):**

- **Snowflake:** A dominant cloud data platform with revenues over $1 billion. Its strength lies in a robust, widely adopted cloud-native architecture combined with strong indexing capabilities and an extensive partner network.

- **Databricks:** With revenues in the hundreds of millions, Databricks is a technology powerhouse, integrating AI-optimized indexing with its leading Apache Spark-based platform. Its innovation in accelerating AI workloads is a key differentiator.

- **Challengers (Medium/Low Innovation, High/Medium Reach):**

- **Qubole:** A solid enterprise player with revenues under $100 million, focusing on cloud-native deployments. It has good enterprise reach but more moderate innovation compared to the leaders.

- **Starburst Data:** An emerging company (revenues under $50M) competing on cost-effective SaaS delivery and flexible integrations, primarily targeting the midmarket with a message of accessibility.

- **Vertica:** A more traditional analytics vendor with established execution capabilities but less focus on SaaS-native multi-dimensional approaches, making it a challenger with lower disruption potential.

- **Cloudera:** An enterprise-focused big data platform with strong data management execution but slower adaptation to SaaS-native models and less disruptive innovation.

- **Trend Setters (High Innovation, Medium/Low Reach):**

- **Dremio:** A highly innovative player (revenues under $100M) known for its advanced open data lake integrations and user-friendly self-service platform, but with more limited market reach than the leaders.

- **Apache Pinot:** An open-source project with powerful real-time indexing capabilities and strong technical vision, but still building commercial traction and enterprise adoption.

- **Pure Players (Medium/Low Innovation, Low Reach):**

- **Presto:** A widely used open-source query engine with significant disruptive potential due to its developer community, but lower commercial execution as a standalone SaaS offering.

- **Impala:** An open-source query engine from Cloudera focused on low latency, but with a smaller community and constrained SaaS positioning, placing it in a niche role.

This mapping reveals a landscape where two giants lead, but a dynamic and varied field of challengers and specialists are constantly vying for position by exploiting different strategic angles.

### D. Analysis of a Market Leader: Databricks

The list of market leaders is formidable, including titans like **Databricks, Snowflake, Amazon Web Services, Google Cloud Platform, Microsoft Azure, Palantir, Cloudera, Teradata, Oracle, and IBM**. Among them, **Databricks** offers a compelling case study in leadership driven by a potent combination of deep technical innovation and effective market strategy.

Databricks, with over 3,000 employees and hundreds of millions in revenue, has expertly positioned itself at the convergence of big data analytics and artificial intelligence. Its core strategy is to provide a unified "lakehouse" platform that combines the best of data warehouses and data lakes. A key pillar of this strategy is its investment in **AI-optimized multi-dimensional indexing**. Databricks recognized early that for AI to scale, the underlying data access had to be exceptionally fast and efficient. Its technology, tightly integrated with Apache Spark, is specifically designed to accelerate the massive data-pulls required for training machine learning models.

The company's GTM is equally impressive. It combines a high-touch enterprise sales motion targeting large corporations with a powerful community-driven approach that has built a loyal following among data scientists and engineers. Their recent $1 billion Series H funding round, valuing the company at approximately $38 billion, will be used to double down on this strategy, expanding R&D in AI and indexing while accelerating their global market penetration. The key factor in Databricks' dominance is its ability to sell not just a tool, but a complete, unified vision for data and AI that resonates powerfully with both technical practitioners and C-level executives.

### E. Focus on a Key Challenger: Starburst

While the leaders command attention, a vibrant ecosystem of challengers is actively working to disrupt the status quo. This group includes innovative companies like **Starburst, Dremio, Tabular (recently acquired by Databricks for $1B), Onehouse, LakeFS, ClickHouse, Firebolt, DataPelago, BigQuery Omni, and Trino**. Among these, **Starburst Data** exemplifies a classic challenger strategy.

Starburst, with around 250 employees and revenues under $50 million, is not trying to out-innovate Databricks on core AI algorithms. Instead, its disruptive strategy is built on **flexibility, accessibility, and cost-effectiveness**. It is built on the open-source Trino (formerly PrestoSQL) query engine, giving it instant credibility with a large community of developers. Starburst’s core value proposition is enabling companies to query data _wherever it lives_—across different clouds, data warehouses, and data lakes—without having to move it first.

This "federated query" approach directly challenges the "unified platform" model of the leaders. For a midmarket company with data scattered across various systems, Starburst offers a pragmatic, lower-cost alternative to a full-scale migration to a single platform like Snowflake or Databricks. Their GTM targets midmarket customers who are more price-sensitive and value flexibility over an all-in-one solution. The primary threat Starburst and other challengers pose to the leaders is **disaggregation**. They threaten to peel off customers who do not need or cannot afford the leaders' all-encompassing platforms, thereby slowing the leaders' growth and creating a more fragmented, multi-polar market.

\*\*\*

## Section 4: Hidden Strengths, Critical Vulnerabilities, and Latent Opportunities in the Market

A comprehensive SWOT analysis, informed by our AI agent's synthesis of market data, reveals the underlying structural dynamics of the Multi-dimensional Data Indexing SaaS sector. This framework uncovers the foundational strengths that create value, the inherent weaknesses that pose risks, the growth opportunities waiting to be seized, and the systemic threats that could reshape the landscape.

### Structural Strengths: The Market's Solid Foundation

The market is built on a bedrock of powerful, advantageous characteristics that create a favorable environment for growth and innovation.

[PLACEHOLDER - MARKET SWOT URL]

- **Robust Market Fundamentals:** The market's substantial size of **€4.5 billion** and its strong **22% YoY growth** provide a massive canvas for opportunity, directly fueled by the macro trends of cloud and AI adoption.

- **Powerful Demand Drivers:** The demand is not speculative; it's driven by the critical, tangible needs of businesses to accelerate query times and reduce soaring cloud compute costs.

- **Favorable Competitive Structure:** The presence of a few dominant leaders alongside several specialized challengers fosters a climate of healthy, innovation-led competition rather than a cutthroat price war.

- **Effective Value Chain Structure:** A diversity of distribution channels—from direct enterprise sales to self-service online platforms—ensures that players can effectively access all key customer segments.

- **High Innovation Velocity:** The environment is defined by rapid technological advancement, with **patented multi-dimensional indexing algorithms** serving as a key competitive advantage and a strong barrier against commoditization.

- **A Maturing Regulatory Framework:** Regulations like GDPR, while adding complexity, ultimately build trust and can serve as a moat for compliant providers who bake in privacy-preserving features.

- **Strong Financial Dynamics:** The market attracts significant investment, demonstrated by healthy **IRR benchmarks of 14-16%** and premium valuation multiples, reflecting strong investor confidence in the SaaS recurring revenue model.

- **Powerful Network Effects:** Deep integration with major data platforms like Apache Spark and BigQuery creates significant ecosystem stickiness, raising switching costs for customers and driving partner-led growth.

- **Strong Intellectual Property Moats:** Patented algorithms form a crucial line of defense, protecting innovators from direct imitation and sustaining their unique value proposition.

- **High Data & Analytics Maturity:** The target customers are increasingly sophisticated in their use of data, creating a strong pull for advanced indexing solutions that can meet their performance demands.

### Critical Weaknesses: The Market's Structural Limitations

Despite its strengths, the market is not without its inherent vulnerabilities. These are the structural challenges that all players must navigate.

- **High Integration Complexity:** The technical challenge of seamlessly integrating with diverse and complex customer data stacks remains a significant barrier to adoption and can slow down sales cycles.

- **Significant Financial Requirements:** The high fixed costs associated with R&D for proprietary algorithms and maintaining a scalable cloud infrastructure create high capital intensity, pressuring margins for smaller players.

- **Extended Enterprise Sales Cycles:** The average sales cycle of **3-6 months** for enterprise deals inflates customer acquisition costs and creates revenue unpredictability.

- **Specialized Talent Scarcity:** A shortage of engineers and data scientists with deep expertise in multi-dimensional indexing and cloud analytics constrains the R&D capacity and scaling potential of many firms.

- **Legacy System Inertia:** In many large enterprises, entrenched on-premise systems and the "build-it-in-house" mentality represent a significant substitution risk and create resistance to adopting SaaS solutions.

- **Moderate Switching Costs:** While ecosystem integration creates stickiness, the cloud-native nature of many solutions means that switching to a competitor, while not trivial, is not insurmountable, keeping pressure on vendors.

- **Ecosystem Dependencies:** A heavy reliance on major cloud providers like AWS and Google Cloud introduces vulnerability to their pricing changes, policy shifts, or API modifications.

- **Customer Reliability Concerns:** Particularly in the midmarket, budget constraints and skepticism about the reliability and long-term viability of smaller SaaS vendors can limit uptake.

- **Communication Complexity:** The highly technical nature of the products makes it difficult to communicate the value proposition clearly and concisely, requiring sophisticated marketing and sales efforts.

- **Geographic Concentration:** The market is currently concentrated in North America and Western Europe, exposing vendors to regional economic downturns and geopolitical risks.

### Sectoral Opportunities: The Catalysts for Future Growth

The intersection of market needs and technological advancement creates a fertile ground for numerous growth opportunities.

[PLACEHOLDER - MARKET SWOT URL 2]

- **Explosive Growth in Emerging Segments:** The **midmarket and SMB segment is growing at 25% YoY**, representing a massive, underserved opportunity for players who can deliver affordable, low-complexity, self-service solutions.

- **AI-Driven Performance Breakthroughs:** Leveraging AI to further optimize indexing algorithms opens the door to new levels of performance, including accelerating AI model training and enabling new real-time analytics use cases.

- **Business Model Innovation:** Freemium-to-paid conversion funnels, consumption-based pricing, and other product-led growth models can significantly lower the barrier to entry and accelerate customer acquisition.

- **Channel Transformation through Community:** Building engaged communities on platforms like Slack provides a low-cost, high-trust channel for customer support, product feedback, and grassroots viral adoption.

- **Strategic Market Consolidation:** The fragmented landscape of smaller specialists presents an opportunity for leaders to acquire unique technology or market access, and for challengers to merge to create a stronger competitive force.

- **Ecosystem and Partnership Deepening:** Moving beyond simple integrations to deep, co-marketing and co-selling partnerships with cloud vendors can unlock significant partner-driven revenue streams.

- **Sustainability as a Differentiator:** As data centers face scrutiny for their energy consumption, solutions that reduce computational waste by optimizing queries have a powerful and timely ESG narrative.

- **Geographic Expansion:** Untapped growth potential exists in emerging markets across the Asia-Pacific region and Eastern Europe, where cloud adoption is accelerating rapidly.

- **Adjacent Market Entry:** The core indexing technology can potentially be extended into adjacent high-growth markets like IoT data analytics and edge computing.

- **Data Monetization and Insights-as-a-Service:** There is a nascent opportunity to move up the value chain by not just optimizing data access, but also by selling the analytics and insights generated as a new service layer.

### Global Threats: The Market's Overarching Risk Factors

Every market operates under the shadow of external threats. For this sector, the most significant risks are competitive, technological, and regulatory.

- **Intense Competitive Rivalry:** The presence of well-capitalized, aggressive incumbents like Snowflake and Databricks creates intense pressure on pricing and necessitates continuous, rapid innovation to survive.

- **Disruptive Technological Shifts:** The rapid pace of technology evolution means a new data architecture or analytics framework could emerge that renders current indexing methods less relevant or even obsolete.

- **Substitution by In-House or Integrated Solutions:** The persistent risk remains that large enterprises will opt to build their own custom solutions or that major cloud platforms will embed "good enough" indexing features natively, reducing the need for third-party specialists.

- **Evolving Regulatory Minefield:** New or changing data privacy and sovereignty laws can create significant compliance costs and operational unpredictability, potentially limiting cross-border service delivery.

- **Supply Chain Vulnerability:** The market's deep dependency on a small number of cloud infrastructure giants (AWS, GCP, Azure) creates a systemic risk if one of these providers experiences a major outage, security breach, or significant price hike.

- **Cybersecurity and Data Breaches:** As custodians of critical analytics infrastructure, these SaaS platforms are high-value targets for cyberattacks. A single major breach could have devastating reputational and financial consequences.

- **Economic Volatility:** A global economic downturn could lead to widespread cuts in IT spending, slowing SaaS adoption rates and lengthening sales cycles, especially for large enterprise deals.

- **Escalating Talent Wars:** The fierce competition for the limited pool of elite data engineers and AI scientists will continue to drive up salary costs and could constrain the growth of all but the best-funded players.

- **Commoditization Pressure:** As the market matures, there is a risk that indexing becomes perceived as a commodity, leading to a race to the bottom on price that would erode margins for all but the largest-scale players.

- **Patent Cliffs and IP Disputes:** The expiration of key patents or costly litigation over intellectual property could weaken the defensive moats of innovative players and open the door to new competitors.

\*\*\*

## Section 5: 15+ Specialized AI Agents: Revolutionizing Multi-dimensional Data Indexing SaaS 🤖

The true transformation of the Multi-dimensional Data Indexing SaaS market will not come from incremental improvements alone, but from the systematic application of Artificial Intelligence across the entire value chain. We have conceptualized an ecosystem of specialized AI agents, each designed to augment a specific human role and optimize a critical business process. These are not futuristic fantasies; they are practical, high-impact workflows designed to create a decisive competitive advantage.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

### A. Two Game-Changing AI Agent Concepts for the Sector

Our analysis identified several priority workflows. Among them, two stand out for their potential to address the market's most pressing challenges and unlock the greatest value.

#### Agent 1: Max, the AI-Driven Indexing Algorithm Optimizer

- **Function:** This advanced AI agent works tirelessly in the background, continuously analyzing query patterns, data distribution, and system performance telemetry. It uses this information to automatically tune, reconfigure, and optimize the proprietary multi-dimensional indexing algorithms in real-time.

- **Augmented Job Title:** It directly augments the capabilities of **Data Engineering and R&D Teams**. Instead of spending weeks manually tuning parameters for a new customer workload, these teams are augmented with an automated system that achieves superior results in minutes, freeing them to focus on next-generation innovation.

- **Problem Solved:** Addresses the critical market weakness of **integration complexity and the need for specialized manual tuning**. It makes the platform smarter and more adaptive out-of-the-box.

- **Concrete Use Case:** A new e-commerce client onboards with a massive product catalog dataset. Max analyzes the initial query patterns during peak shopping hours and automatically adjusts the indexing layout to prioritize filtering on `product_category` and `price_range`, dramatically reducing query latency for the most common user searches without any human intervention.

- **Key KPIs Impacted:**

1. **Query Latency:** Aims to reduce average query times by 30-50%.

2. **Cloud Compute Cost:** Aims to lower compute spend by 15-25% through more efficient data access.

3. **R&D Productivity:** Aims to reallocate 40% of manual tuning time to core innovation tasks.

- **Game-Changer Impact:** Max transforms a company's core IP from a static asset into a living, learning system that constantly improves, creating a powerful and ever-widening competitive moat.

#### Agent 2: Sage, the Predictive Market Analytics Engine

- **Function:** Sage is an intelligence agent that ingests a vast array of data—from public sources like funding announcements and job postings to internal customer usage patterns and CRM data. It builds predictive models to identify emerging customer segments, pinpoint high-intent leads, and forecast market trends.

- **Augmented Job Title:** This agent acts as a strategic partner for **Sales and Marketing Leaders**. It provides them with a prioritized list of target accounts, data-backed talking points, and early warnings of competitive moves, transforming their GTM from reactive to predictive.

- **Problem Solved:** Directly tackles the market weaknesses of **long sales cycles and high customer acquisition costs**, especially in the enterprise segment.

- **Concrete Use Case:** Sage detects a cluster of mid-sized health tech companies that have recently received Series B funding and are hiring data engineers with experience in Apache Spark. It flags this as an emerging high-potential sub-segment, automatically scores the top 20 companies, and provides the sales team with a tailored outreach sequence highlighting a case study from another health tech client.

- **Key KPIs Impacted:**

1. **Sales Cycle Length:** Aims to reduce the average sales cycle by 20%.

2. **Lead-to-Opportunity Conversion Rate:** Aims to increase conversion rates by 25% through better targeting.

3. **Pipeline Velocity:** Aims to accelerate the overall movement of deals through the sales funnel.

- **Game-Changer Impact:** Sage provides the "unfair advantage" of knowing where the market is going before competitors do, allowing a company to allocate its resources with surgical precision and consistently outmaneuver the competition.

### B. A Broader Ecosystem of 10+ AI Agent Concepts

Beyond these two, a full suite of agents can be deployed to optimize every corner of the business:

[PLACEHOLDER - MARKET SWOT PRIORITY URL]

1. **Echo - AI-Powered SaaS Integration Assistant:** Augments **Customer Success Managers** by automating and guiding customers through complex integrations, reducing onboarding friction.

2. **Sentinel - AI-Driven Compliance Monitoring System:** Augments **Compliance Officers** by continuously monitoring data usage against regulations like GDPR, automating reporting and alerting.

3. **Bridge - AI-Enhanced Customer Engagement Platform:** Augments **Customer Success Teams** by using predictive analytics to identify churn risks and trigger proactive, personalized outreach.

4. **Futura - Demand Forecasting Analyzer:** Augments **Finance and Sales Planning Teams** by forecasting demand based on economic indicators and IT budget cycles, enabling proactive resource allocation.

5. **Optima - Multi-Cloud Resource Optimizer:** Augments **Cloud Infrastructure Managers** by dynamically allocating workloads across different cloud providers to optimize for cost and performance.

6. **Guardian - AI-Powered Cyber Threat Detector:** Augments the **Security Operations Center (SOC)** by identifying anomalous activity and potential intrusions in real-time.

7. **Liaison - AI-Enabled Technical Education Assistant:** Augments **Technical Writers** by auto-generating clear, easy-to-understand documentation and tutorials for complex features.

8. **Prime - Energy-Aware Algorithm Designer:** Augments **R&D Teams** by designing indexing configurations that explicitly minimize energy consumption, supporting sustainability goals.

9. **Insight - White Space Opportunity Identifier:** Augments **Product Managers** by mining customer feedback and market data to discover unmet needs and lucrative niche opportunities.

10. **Voice - AI-Powered Ecosystem Partner Facilitator:** Augments **Partnership Managers** by identifying high-potential partners and facilitating collaboration and joint GTM planning.

### C. The Ultimate Advantage: An Interdependent AI Agent System

The true pinnacle of AI-driven strategy is not in deploying individual agents, but in creating a fully integrated, synergistic system where agents collaborate, orchestrated by a master agent.

[PLACEHOLDER - MARKET AGENT SYSTEM URL]

Imagine a **Harmony Tech Command Center**, a master orchestrator agent that has a complete, real-time view of the entire value chain. It augments the **Chief Data Officer**, providing strategic oversight and coordination. This orchestrator directs five specialized sub-agents:

1. **Nexus Optima (Integration):** Automates deployment into customer data lakes.

2. **Turbo Quest (Query Acceleration):** Optimizes query speeds post-integration.

3. **Frugal Sentinel (Cost Management):** Monitors the compute costs generated by the queries.

4. **Core Pulse (Platform Efficiency):** Ensures the underlying data platform is running efficiently.

5. **Neuron Surge (AI Training Acceleration):** Focuses specifically on speeding up ML workloads.

When a new customer signs up, Harmony Tech delegates the integration task to Nexus Optima. Once complete, it signals Turbo Quest to begin optimizing queries. As users run queries, Frugal Sentinel analyzes the cost impact and recommends efficiencies, which Core Pulse might implement by rebalancing resources. If the customer is an AI company, Neuron Surge steps in to specifically accelerate their model training pipelines. Harmony Tech monitors the KPIs from all five agents, resolving bottlenecks and providing the human leadership team with a single, holistic view of customer health and value delivery. This is the future of the sector: a fully "augmented" organization, operating with a level of speed, intelligence, and efficiency that is simply unattainable through human effort alone.

\*\*\*

## Section 6: Accelerating Growth in the Data Indexing Market

For organizations poised to lead in the data optimization space, such as Qbeast, which possesses unique multi-dimensional indexing technology and a strong technical team, the path forward is clear. Leveraging strategic insights and AI-driven automation is not just an option; it is essential for capturing market share and achieving leadership within the next decade.

### Conclusion: A Strategic Synthesis and Path Forward

This deep-dive analysis of the Multi-dimensional Data Indexing SaaS market reveals a sector at a dynamic inflection point. It is a **€4.5 billion market** with a robust **22% annual growth rate**, fueled by the unstoppable macro trends of cloud adoption and AI integration. The landscape is clearly segmented, with large enterprises demanding de-risked performance and a burgeoning midmarket clamoring for accessible, self-service efficiency. Victory requires tailored GTM strategies—a high-touch, ROI-focused approach for the former, and a frictionless, product-led model for the latter.

The competitive arena is dominated by the twin powers of **Databricks and Snowflake**, whose leadership is built on a potent mix of deep technological innovation and formidable market reach. However, a vibrant cast of challengers like **Dremio and Starburst** are effectively disrupting the edges by targeting specific niches or offering more flexible, cost-effective solutions. The market's structural strength lies in its high innovation potential and clear demand drivers, yet it is constrained by inherent weaknesses like integration complexity and talent scarcity. The most significant opportunity lies in capturing the fast-growing midmarket segment, while the greatest threat remains substitution from platform incumbents.

The ultimate conclusion of our analysis is that Artificial Intelligence will be the decisive factor in this market's next chapter. The strategic deployment of a coordinated ecosystem of AI agents—from algorithm optimizers like **Max** to intelligence engines like **Sage**—offers a clear pathway to outmaneuver competitors. These agents can compress sales cycles, slash operational costs, accelerate innovation, and deliver a superior customer experience.

The market is moving towards a future where indexing performance is self-optimizing, market strategy is predictive, and customer onboarding is frictionless. The companies that will win will be those that embrace this AI-augmented reality, transforming their operations from a series of manual processes into a cohesive, intelligent, and automated system. The opportunity is not just to participate in the market's growth, but to actively shape its future.

If you are interested in this topic you can follow these next steps:

1️⃣Download below the full Multi-dimensional Data Indexing SaaS market study in pdf format

[PLACEHOLDER - PDF DOWNLOAD LINK]

2️⃣ Get additional insights of this market by reading our memo of an interesting company in this market called Qbeast (Accelerate queries, cut costs, optimize data lakes.)

[PLACEHOLDER - QBEAST MEMO LINK]

3️⃣ If you want us to build a custom AI system and dedicated AI agents, book a strategic discussion with an AI Partner : https://forms.proplace.co/meet