.png)

The Carbon Capture Utilization Tech market by our Market Intelligence AI agent

# The Race to Zero: A Deep Dive into the Carbon Capture Utilization Tech Market

**Meta Description:** An in-depth strategic analysis of the Carbon Capture Utilization (CCU) Tech market for steel manufacturing. Explore market size, go-to-market strategies, competitive dynamics, SWOT, and the transformative potential of AI agents.

**Keywords:** Carbon Capture Utilization Tech, artificial intelligence, AI market analysis, CCU Technology 2025, AI agents for steel decarbonization, industrial AI, deep tech strategy, sustainable manufacturing.

\*\*\*

### Introduction

The global steel industry, a cornerstone of modern civilization, stands at a critical juncture. As one of the world's largest emitters of CO₂, it faces unprecedented pressure from regulators, investors, and society to decarbonize. This challenge has catalyzed a wave of innovation, thrusting Carbon Capture Utilization (CCU) technologies from the laboratory to the industrial frontline. This is no longer a distant ambition; it is an urgent strategic imperative.

While conventional wisdom has long emphasized post-combustion capture retrofit solutions as the primary lever for decarbonization in steelmaking, our analysis reveals a more nuanced and disruptive reality. We've found that integrated, tailored CCU technologies embedded directly into steel production processes may represent the fastest route to market leadership, offering superior operational efficiencies and long-term emission reductions that legacy approaches might struggle to match.

This comprehensive analysis, powered by our Market Intelligence AI agent, will guide you through the intricate landscape of the CCU technology market for steel manufacturing. We will dissect the market's size and segments, explore winning go-to-market strategies, map the competitive power dynamics, and reveal the structural strengths and hidden vulnerabilities of this rapidly evolving ecosystem. Finally, we will conceptualize how purpose-built AI agents can not just optimize but fundamentally reshape this industry, creating unprecedented value and accelerating the transition to a sustainable future.

[PLACEHOLDER - A HIGHLY-IMPACTFUL VISUAL REPRESENTING THE CONVERGENCE OF STEEL MANUFACTURING AND CCU TECHNOLOGY]

\*\*\*

## Section 1: A Complete Panorama of the Carbon Capture Utilization Tech Market

### Carbon Capture Utilization Tech: An €8 Billion Market on the Brink of Transformation

The global Carbon Capture Utilization (CCU) technology market is not merely growing; it is accelerating at a formidable pace, propelled by a global mandate to mitigate climate change. As industries grapple with their carbon footprint, the steel sector has emerged as a focal point for CCU adoption due to its significant emissions profile. Our analysis projects the Total Addressable Market (TAM) for CCU technologies across heavy industries to reach approximately **€8 billion by 2025-2026**, with a powerful year-over-year growth rate of **20%**. This expansion is underpinned by increasingly stringent carbon regulations and the rising economic viability of turning captured CO₂ into value-added products.

[PLACEHOLDER - YOUR MARKET URL]

For the steel industry specifically, this translates into a Serviceable Addressable Market (SAM) of **€1.6 billion**. This figure represents the immediate opportunity for CCU providers focusing on steel manufacturing in regions with aggressive decarbonization mandates, such as the European Union, North America, and parts of Asia. Within this landscape, a focused company like PeroCycle could realistically target a Serviceable Obtainable Market (SOM) of **€240 million** over the next 3-5 years, representing a significant 15% share of the SAM by leveraging technological differentiation and strategic partnerships.

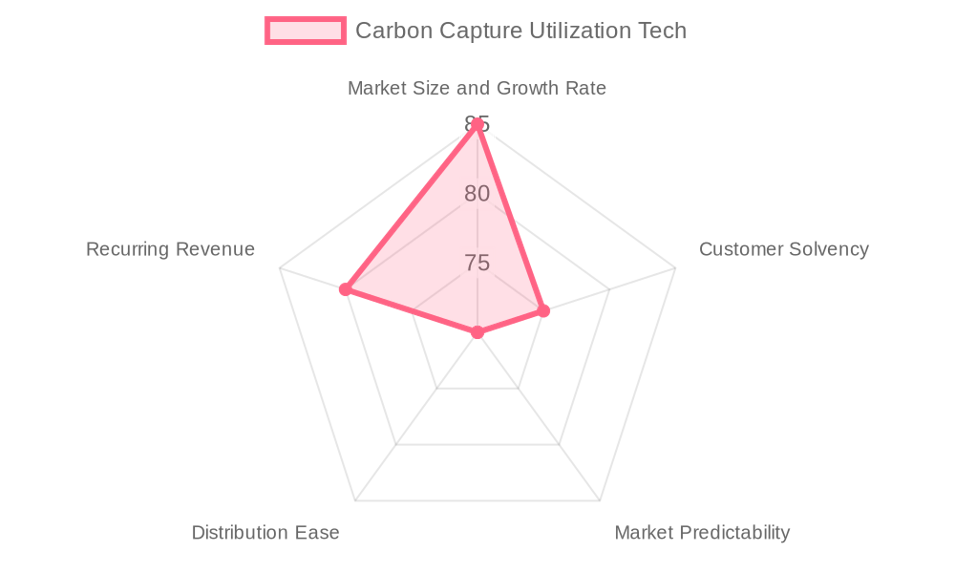

The market's attractiveness is scored at a high **80 out of 100**, reflecting its robust size and growth, the financial solvency of large steel manufacturers, and the potential for long-term, recurring revenue contracts. Though some unpredictability exists due to shifting policy landscapes, the underlying momentum is undeniable. Key performance indicators (KPIs) in this sector underscore its capital-intensive and performance-driven nature. Success is measured by tangible outcomes like the **weekly volume of CO₂ captured (benchmarked at 500-800 metric tons per facility)**, the **operational availability of capture systems (targeting 95% or higher)**, and the **energy consumed per ton of CO₂ captured (aiming for the 250-350 kWh/ton range)**.

The market can be dissected into three primary segments, each with distinct characteristics and opportunities.

#### **Segment 1: Post-Combustion Carbon Capture for Steel Plants (~40% of TAM)**

This segment, representing **€3.2 billion** of the TAM and growing at **18% annually**, is the most mature. Its core strength lies in its **retrofitting capability**, allowing existing, traditional blast furnace plants to integrate carbon capture technology without a complete operational overhaul. This makes it a compelling solution for established steel producers facing immediate regulatory pressure to reduce emissions.

The target audience consists of large steel manufacturers, particularly in Asia, Europe, and North America, operating under tight emissions restrictions. Their key decision-makers—Chief Sustainability Officers, Plant Managers, and CAPEX Committees—are often risk-averse, seeking technology that is proven at scale. Their primary pain points are the high costs associated with carbon taxes and the critical need to balance emissions reduction with operational efficiency. The sales cycle is consequently long, typically **12-24 months**, involving extensive feasibility studies and pilot testing.

#### **Segment 2: Carbon Utilization for Chemical Feedstocks (~30% of TAM)**

Growing at an impressive **22% year-over-year**, this **€2.4 billion** segment is driven by innovation and the principles of a circular economy. It focuses on the **conversion of captured CO₂ into valuable products like chemicals and synthetic fuels**. This transforms a liability—carbon emissions—into a potential revenue stream.

The target audience here is markedly different. It includes innovation-led chemical manufacturers and integrated steel producers looking to diversify their offerings and pioneer sustainable solutions. These are the early adopters, led by R&D Directors and Corporate Strategy Officers. Their primary challenges are the scalability of emerging conversion technologies and the market uncertainty for CO₂-derived products. The buying cycle is shorter, around **12 months**, and often tied to R&D budgets and pilot deployments through joint ventures or technology licensing agreements.

#### **Segment 3: Direct Carbon Capture Technology Integration (~30% of TAM)**

This **€2.4 billion** segment, with a strong **20% annual growth rate**, represents the cutting edge of CCU. It involves the **direct integration of customized CCU solutions into the core steel manufacturing process**, tailored to a plant's specific emissions profile and production technology. This approach is particularly attractive to producers investing in "green steel" and seeking long-term, systemic decarbonization.

The target audience comprises progressive, mid-to-large steel producers in regions with ambitious climate targets. Led by Engineering Managers and Heads of Sustainability, these companies are focused on achieving sustainability leadership and operational efficiency gains. Their key pain points are the complexity of process integration and the investment risk associated with emerging technologies. The purchase journey is therefore meticulous, with due diligence phases often exceeding **18 months** and centering on pilot testing to prove reliability and compatibility with existing infrastructure.

Our AI-driven analysis of the CCU market has identified several key signals and trends shaping its trajectory:

1. **Macro Signal - Regulatory Certainty:** Stringent carbon regulations, exemplified by the EU Emissions Trading System (ETS), are the primary engine of market growth. This creates a predictable, non-discretionary demand for CCU solutions.

2. **Technological Signal - Accelerating Maturity:** Innovations in solid sorbent materials and CO₂-to-fuel pathways are rapidly moving from pilot to commercial scale, with a striking **18-22% CAGR** in project expansion.

3. **Competitive Signal - Fragmented Leadership:** While incumbents like Mitsubishi Heavy Industries lead, the market is fragmented enough for nimble innovators like LanzaTech and Svante to carve out significant niches, particularly in customization and utilization.

4. **Behavioral Evolution - Proactive Investment:** Corporate sustainability commitments and net-zero targets are shifting steel manufacturers from reactive compliance to proactive investment in CCU as a core part of their long-term strategy.

5. **Economic Evolution - The Rise of Circular Carbon:** The transformation of CO₂ from waste to feedstock is creating new value chains and business models, particularly at the intersection of the steel and chemical industries.

Looking ahead, we predict that the next 2-3 years will be defined by a race to scale. Companies that can demonstrate reliable, cost-effective, and seamlessly integrated CCU solutions will capture a disproportionate market share. The focus will shift from simple capture to sophisticated utilization, and AI will become indispensable for optimizing these complex, interconnected systems.

\*\*\*

## Section 2: 3 Potentially Winning Go-To-Market Strategies to Conquer the CCU Tech Market

Navigating the CCU technology market requires more than just superior technology; it demands a nuanced, segment-specific go-to-market (GTM) strategy. Our analysis identifies three distinct playbooks, each tailored to the unique profiles, pain points, and buying behaviors of the primary market segments.

### A. GTM for Segment 1: Post-Combustion Carbon Capture for Steel Plants

This strategy targets the largest and most established segment: traditional steel plants seeking regulatory compliance through retrofitting.

[PLACEHOLDER - GTM\_1 IMAGE: A visual representing a large, established steel plant with a CCU retrofit module being added.]

**The Ideal Customer Profile (ICP):** The target is a large, B2B industrial manufacturer in the steel sector with **1,000-10,000 employees** and **€1B-€10B in revenue**. These companies, located primarily in Europe, North America, and Asia, have a mature approach to technology adoption and have allocated **€50M-€200M in CAPEX** for carbon reduction initiatives. Their decision timelines are long, ranging from **12 to 24 months**.

**The Winning Persona & Their Obsessions:** The key decision-maker is the **Chief Sustainability Officer (CSO)**, who reports to the C-suite. Their world revolves around three core obsessions:

1. **Compliance Assurance:** Ensuring the company meets or exceeds tightening emissions regulations to avoid crippling fines and reputational damage.

2. **Operational Continuity:** Implementing new technology with minimal disruption to existing production, as downtime directly impacts the bottom line.

3. **Cost-Benefit Justification:** Proving a clear return on investment (ROI) for any significant capital expenditure, balancing green credentials with financial prudence.

**Top Acquisition Channels & Buying Triggers:** Reaching this persona requires a multi-pronged approach focused on credibility and trust.

- **Industry Conferences & Trade Shows:** Essential for high-level networking and demonstrating technology at scale.

- **Direct B2B Sales:** Dedicated account management is crucial for navigating long sales cycles and complex organizations.

- **Technical Whitepapers & Case Studies:** Providing evidence of reliability and ROI is paramount for this risk-averse audience.

- **Partnerships with EPC Firms:** Collaborating with established Engineering, Procurement, and Construction firms provides a trusted channel to market.

The primary buying trigger is **regulatory change**, such as an increase in carbon pricing or the announcement of stricter emissions targets.

**The 4-Step Acquisition Process:**

1. **Awareness & Education:** Use LinkedIn ads and sponsored content targeting CSOs and Plant Managers with messaging about regulatory pressure and proven retrofit solutions.

2. **Consideration & Validation:** Retarget engaged prospects with detailed technical whitepapers, pilot project data, and webinar invitations focusing on ROI and minimal operational disruption.

3. **Deep Dive & Pilot Proposal:** Engage through direct outreach and account management to set up technical deep-dive sessions, leading to a formal proposal for a paid pilot project.

4. **Contract & Scale-Up:** Following a successful pilot, negotiate a long-term contract for full-scale deployment, leveraging the proven results to overcome final objections on cost and complexity.

**Calculating the Return:** Success in this segment requires disciplined investment. The goal is to acquire customers with a Customer Acquisition Cost (CAC) under **€150K**. With long-term contracts and recurring maintenance revenue, the Customer Lifetime Value (LTV) can be substantial. A healthy LTV:CAC ratio of **5:1 or higher** should be the target, leading to the generation of a **€10M pipeline within 30 days** and the acquisition of **3 customers for €5M in revenue within 90 days.** The key insight is that for this segment, **reliability trumps novelty**. Your messaging must center on proven success, minimal disruption, and de-risking a major capital investment.

### B. GTM for Segment 2: Carbon Utilization for Chemical Feedstocks

This playbook is designed for the innovators—chemical manufacturers and integrated producers seeking to turn CO₂ into revenue.

[PLACEHOLDER - GTM\_2 IMAGE: A futuristic visual showing CO2 molecules being transformed into chemical compounds.]

**The Ideal Customer Profile (ICP):** The target is a mid-to-large B2B manufacturer in the chemical or integrated steel-chemical sectors, with **500-5,000 employees** and **€500M-€3B in revenue**. These companies are early adopters with a dedicated R&D budget of **€10M-€50M** for innovation projects and a decision timeline of around **12 months**.

**The Winning Persona & Their Obsessions:** The crucial decision-maker is the **R&D Director**, who reports to the VP of Engineering or Corporate Strategy. Their primary obsessions are:

1. **Technological Scalability:** Finding and validating novel CO₂ utilization pathways that can be scaled from the lab to commercial production.

2. **Market Viability:** Identifying and confirming a real market demand for the CO₂-derived products to ensure a return on R&D investment.

3. **Strategic Alignment:** Ensuring that new circular economy initiatives align with broader corporate goals for sustainability and revenue diversification.

**Top Acquisition Channels & Buying Triggers:** This segment congregates in forums dedicated to innovation.

- **R&D Consortiums & Innovation Clusters:** Participating in these groups provides direct access to decision-makers and ongoing projects.

- **Industry-Specific Webinars:** Hosting and presenting at technical webinars positions you as a thought leader and innovation partner.

- **Joint Ventures & Strategic Partnerships:** Direct partnership proposals are the most effective channel for commercialization.

- **Technology Licensing News:** Monitoring announcements of new R&D projects and licensing deals provides key intent signals.

The buying trigger is often an internal **strategic mandate to explore circular economy solutions** or a breakthrough in a pilot project.

**The 4-Step Acquisition Process:**

1. **Innovation Showcase:** Target R&D Directors on LinkedIn and in industry publications with content about patented technology and R&D successes.

2. **Collaborative Dialogue:** Engage leads through invitations to exclusive webinars and R&D consortium events, focusing on partnership potential rather than a hard sell.

3. **Joint Development Proposal:** Initiate direct conversations to explore a joint development agreement or a technology licensing deal for a specific application.

4. **Pilot & Commercialization:** Launch a collaborative pilot project to validate the technology and co-develop a commercialization roadmap for the resulting products.

**Calculating the Return:** This GTM motion is about building deep, strategic partnerships. The target CAC should be lower, under **€120K**, as sales cycles are relationship-driven. Success is measured not just by initial revenue but by the initiation of **2 licensing deals within 90 days**. The key insight for this segment is to **position yourself as an innovation co-pilot, not a vendor**. The value proposition is a shared journey of discovery and commercialization, de-risking innovation for your partner.

### C. GTM for Segment 3: Direct Carbon Capture Technology Integration

This strategy is for the visionaries—steel producers committed to building the "green steel" plants of the future.

[PLACEHOLDER - GTM\_3 IMAGE: An animated schematic of a modern steel plant with CCU technology seamlessly integrated into its core processes.]

**The Ideal Customer Profile (ICP):** The target is a progressive steel producer with **500-8,000 employees**, **€500M-€6B in revenue**, and a public commitment to investing in green steel. They have a CAPEX budget of **€20M-€100M** and a long decision timeline of **18-24 months** for these strategic projects.

**The Winning Persona & Their Obsessions:** The key decision-maker is the **Engineering Manager** or **Head of Sustainability**, who is responsible for the technical execution of the company's green steel strategy. Their obsessions are:

1. **Integration Seamlessness:** Ensuring that new CCU technology is perfectly compatible with their specific production processes and existing infrastructure.

2. **Long-Term Reliability:** Validating that the emerging technology is robust and will deliver on its emissions reduction promises over the long term.

3. **Risk Mitigation:** Carefully managing the investment risk and potential operational disruption associated with implementing unproven, cutting-edge technology.

**Top Acquisition Channels & Buying Triggers:** Engagement with this segment must be deeply technical and consultative.

- **Technical Workshops:** Hosting hands-on workshops on direct integration challenges establishes you as a technical authority.

- **Industry Partnerships & Pilot Programs:** Co-launching pilot programs with influential steel producers builds credibility and provides invaluable case studies.

- **Consultancy-Led Procurement:** Building relationships with the engineering consultancies that advise steel producers on major capital projects.

- **Direct Enterprise Contracts:** Engaging in long-term, direct contract negotiations with a focus on customization and partnership.

A key buying trigger is the announcement of a major **"green steel" capital project** or the availability of government funding for decarbonization pilots.

**The 4-Step Acquisition Process:**

1. **Thought Leadership:** Target engineering leaders with sponsored technical articles and workshop invitations focused on direct integration best practices.

2. **Consultative Engagement:** Use direct outreach to schedule technical consultations, focusing on the specific challenges and opportunities of the prospect's plant.

3. **Customized Pilot Contract:** Develop a highly detailed proposal for a pilot project designed to prove the technology's compatibility and performance within their unique operational environment.

4. **Strategic Partnership Agreement:** Following a successful pilot, transition to a long-term strategic partnership for full-scale integration and ongoing optimization.

**Calculating the Return:** This GTM is the most resource-intensive but potentially the most rewarding. The target CAC is around **€130K**. Success is defined by securing **3 pilot contracts within 90 days**, which serve as the foundation for multi-million-euro, multi-year deployments. The critical insight here is that **customization and co-creation are everything**. You must demonstrate a deep understanding of the customer's specific operational context and position yourself as a long-term engineering partner dedicated to their success.

In summary, a one-size-fits-all GTM will fail. Conquering the CCU market requires a tripartite strategy: selling **reliability** to the incumbents, **innovation** to the chemical pioneers, and **customized partnership** to the green steel visionaries.

\*\*\*

## Section 3: Who Truly Holds the Power in the Carbon Capture Utilization Tech Market?

To succeed in the CCU technology sector, it is not enough to understand the market; one must comprehend its intricate power dynamics. An analysis of the value chain, competitive pressures, and key players reveals a landscape where technological maturity and entrenched customer relationships are the primary currencies of power.

[PLACEHOLDER - COMPETITION URL]

### A. The Value Chain and the Epicenter of Power

The CCU value chain in steel manufacturing is a complex sequence: **Raw material sourcing → Steel production → Carbon capture technology development → Technology integration → Emissions monitoring & compliance → Industrial partnerships**. While each stage is crucial, our analysis, based on Porter's Five Forces, indicates that power is not distributed evenly.

The highest barriers to entry and, consequently, the greatest concentration of power, lie within the **technology development and integration stages**. This is where substantial capital investment, deep specialized expertise, proprietary technologies, and rigorous certifications create a formidable moat. The bargaining power of customers—the large, concentrated steel manufacturers—is **High**. They can demand significant customization and favorable terms. However, once a technology is integrated, high switching costs due to long investment cycles and operational disruption grant the technology provider significant leverage. The bargaining power of suppliers of specialized chemicals or components is **Medium**, as they provide critical inputs but are often part of a competitive supplier landscape. The threat of new entrants is **Medium**; while capital and expertise are barriers, novel tech startups can find entry points through pilot programs.

Ultimately, the real power is held by leading technology developers and engineering firms. Incumbents like **Carbon Clean** and **Mitsubishi Heavy Industries** wield considerable influence. They possess proprietary technologies, proven track records, and strong, long-standing relationships with major steel producers and EPC firms. This combination allows them to command the largest margins and shape the market's technological trajectory.

### B. The Axes of Differentiation and Competitive Tension

The competitive battlefield is defined by two primary axes of differentiation:

1. **Technology Maturity and Innovation:** This axis measures a company's ability to offer proven, scalable, and efficient CCU technologies. In a sector defined by high-stakes capital projects, customer trust hinges on demonstrated reliability and a clear innovation roadmap that promises future performance gains.

2. **Market Reach and Customer Relationships:** This axis evaluates the breadth and depth of a company's global presence and its network within the steel industry. In this relationship-driven market, a strong existing footprint with steel producers and EPC firms is a powerful accelerator for growth.

These axes create three fundamental competitive tensions:

- **Incumbents vs. Innovators:** Established leaders with mature technology and broad reach compete against agile startups with disruptive but less proven solutions.

- **Integrated Solutions vs. Niche Specialization:** Companies offering end-to-end, turnkey projects clash with specialists focusing on a single, highly optimized component of the CCU process (e.g., a novel solvent or membrane).

- **Cost Efficiency vs. Performance Leadership:** A constant battle exists between solutions that prioritize the lowest possible capital and operational cost versus those that promise the highest capture efficiency and value creation from utilization.

The real power resides at the intersection of these axes. Companies that can combine proven, mature technology with deep, trusted customer relationships are best positioned to dominate.

### C. Mapping the 10 Key Players in the CCU Arena

Our analysis of the competitive landscape identifies a clear hierarchy of players, each occupying a distinct strategic position.

[PLACEHOLDER - COMPETITION QUADRANT URL]

**The Leaders:** These companies exhibit both high technology maturity and extensive market reach.

- **Carbon Clean:** A leader in CCU technology with estimated revenues of €150 million. They are distinguished by their advanced chemical absorption technology and a portfolio of successful, large-scale deployments.

- **Mitsubishi Heavy Industries:** A global industrial conglomerate with over €120 billion in revenue. Their power stems from deep engineering expertise, vast integration capabilities, and a dominant market presence, especially in Asia.

**The Specialists (or Trend Setters):** These players have strong technology and innovation but a more focused or emerging market reach.

- **Fluor Corporation:** A major engineering firm with around $16 billion in revenue. They excel at delivering turnkey CCU projects using advanced amine solvents, positioning them as a technology specialist with a growing market presence.

- **LanzaTech:** A key innovator with revenues near $50 million, specializing in converting captured carbon into chemical feedstocks using microbial technology. Their disruption potential is high, though their focus has traditionally been more on the chemical sector than steel.

- **CarbonCure Technologies:** An innovative player focused on utilizing recycled CO₂ in concrete, demonstrating strong visionary capacity but still scaling its execution in heavy industries.

- **Blue Planet Systems:** A visionary company with highly innovative mineralization technologies, though its commercial deployment in the steel sector is still in early stages.

**The Challengers:** These companies have strong execution capabilities but may lag in visionary, disruptive technology.

- **Linde:** An industrial gas giant with a vast customer footprint and solid experience with proven capture technologies, but with less emphasis on cutting-edge disruption.

- **Honeywell UOP:** A provider of reliable process technologies with established market relationships, focusing on incremental rather than radical innovation.

**The Accessible (or Pure Players):** These companies are building their presence and technology.

- **Svante:** A mid-size company with estimated revenues of €30 million. They are developing promising solid sorbent capture technologies through several pilot projects, making them an accessible partner with progressing technology maturity.

This mapping reveals a dynamic landscape where large, established leaders are challenged by agile, technology-driven specialists. The competitive intensity is high, with a total score of **75 out of 100**, driven by high differentiation potential and significant customer switching costs.

### D. Deep Dive on a Market Leader: ArcelorMittal and the Incumbent Cohort

To understand the forces of market domination, we look to **ArcelorMittal**, a quintessential leader in the steel industry. While not a CCU technology developer itself, it represents the primary customer and partner whose strategic decisions shape the entire ecosystem. ArcelorMittal's strategy is defined by a dual approach: optimizing existing blast furnace assets with retrofit CCU solutions while simultaneously investing in breakthrough technologies for long-term green steel production.

Their strength lies in their immense scale, global operational footprint, and significant CAPEX budgets dedicated to decarbonization. They, along with other industry titans like **ThyssenKrupp, Tata Steel, SSAB, Voestalpine, Salzgitter, Nucor, Nippon Steel, POSCO, and China Baowu**, form a powerful cohort of incumbents.

The collective strategy of these leaders is often one of cautious, calculated adoption. They prioritize proven, de-risked technologies that can be deployed at scale with minimal operational disruption. Their immense bargaining power allows them to demand extensive pilot testing and favorable commercial terms from technology providers. Their key to maintaining market dominance is their ability to leverage their existing infrastructure and capital to scale up successful CCU solutions faster and more broadly than any challenger could. They are the gatekeepers to the largest market segment, and their endorsement can make or break a new technology.

### E. Focus on a Key Challenger: H2 Green Steel and the Disruptors

In stark contrast to the incumbents stands **H2 Green Steel**, a prime example of a market challenger. Their strategy is not to retrofit the old but to build the new from the ground up. By designing a greenfield steel plant powered by green hydrogen and fully integrated with the latest clean technologies, they aim to leapfrog the legacy assets of incumbents entirely. Their disruptive potential lies in creating a new paradigm for steel production where decarbonization is not an add-on but a foundational principle.

H2 Green Steel is part of a growing wave of challengers, including innovators like **Boston Metal**, and agile, forward-thinking producers such as **Nucor Corporation, Steel Dynamics, Cleveland-Cliffs, Salzgitter, Liberty Steel, and the Celsa Group**. These companies threaten the established order in several ways:

- **Technological Disruption:** By embracing green hydrogen, direct electrification (as with Boston Metal), or novel CCU integration, they challenge the long-term viability of the traditional blast furnace route.

- **Brand & Market Positioning:** They are capturing the "green steel" narrative, attracting ESG-focused investors and customers willing to pay a premium for carbon-neutral products.

- **Agility:** Unburdened by legacy infrastructure, they can design and build optimized, highly efficient plants that may ultimately have a lower long-term operating cost than retrofitted older facilities.

The primary threat these challengers pose to leaders like ArcelorMittal is not a direct, immediate takeover of market share, but a fundamental shift in the definition of "best practice" for steelmaking. If their models prove economically and technologically superior, they could make the incumbents' vast asset base a liability rather than a strength.

\*\*\*

## Section 4: Unveiling the Market's Structural Strengths, Hidden Vulnerabilities, and Strategic Opportunities

A comprehensive SWOT analysis reveals the underlying forces that will determine the winners and losers in the CCU technology market. It highlights a sector buoyed by strong regulatory drivers and innovation but constrained by high capital costs and technological complexity.

### Structural Strengths: The Market's Solid Foundation

The CCU market is built on a set of powerful and enduring strengths that create a favorable environment for growth and value creation.

[PLACEHOLDER - MARKET SWOT URL]

1. **Massive and Growing Addressable Market:** The market's foundation is a substantial **€8 billion TAM** with a robust **20% annual growth rate**. This scale provides ample room for multiple players to thrive and ensures a consistent flow of new opportunities. AI can amplify this by enhancing market analytics to pinpoint the most lucrative growth hotspots.

2. **Regulatory-Driven Demand:** Demand is not speculative; it is mandated. Carbon pricing and emissions trading schemes create a powerful and predictable economic incentive for steel producers to invest in CCU, ensuring consistent market pull. AI helps firms navigate this with real-time compliance tracking and scenario modeling.

3. **High Potential for Differentiation:** The technological complexity of CCU creates significant opportunities for companies to differentiate themselves based on capture efficiency, integration ease, or the value of utilized products. AI accelerates this by enabling advanced process optimization and faster innovation cycles.

4. **Established Value Chain and Channels:** Pre-existing relationships between steel producers and large EPC firms provide well-defined and accessible distribution channels for new technologies, reducing the friction of market entry.

5. **High Customer Switching Costs:** The long sales cycles (**12-24 months**) and deep integration of CCU systems into plant operations create high switching costs. This fosters strong customer retention and predictable, recurring revenue streams for service and maintenance. AI enhances this with personalized engagement and predictive service management.

6. **Strong Financial Underpinnings:** The target customers—large steel manufacturers—are capital-intensive organizations with access to significant CAPEX budgets for strategic projects, and the sector supports favorable IRR benchmarks of **14-16%**.

### Critical Weaknesses: The Structural Headwinds

Despite its strengths, the market is not without its structural limitations, which can slow adoption and create significant challenges for participants.

1. **High Upfront Capital Expenditure:** The significant capital required for CCU projects is a major barrier to adoption, especially for smaller producers. The long investment cycles delay revenue realization and require sophisticated financial justification. AI-enabled financial modeling can help optimize these investment decisions and improve capital efficiency.

2. **Operational Complexity and Integration Risk:** Integrating a complex chemical process like CCU into a live steel plant is a major engineering challenge that carries the risk of costly operational downtime and disruption. AI can mitigate this through digital twin simulations for retrofit planning and predictive maintenance to prevent failures.

3. **Fragmented and Uneven Technology Maturity:** The market offers a wide spectrum of solutions, from proven but less efficient technologies to innovative but unproven ones. This fragmentation can create confusion for buyers and uncertainty about long-term performance.

4. **Long and Complex Sales Cycles:** The decision-making process for a CCU investment is lengthy and involves numerous stakeholders, from engineering to finance to the C-suite. This increases customer acquisition costs and requires a highly skilled, patient sales force.

5. **Dependence on Regulatory Stability:** The market's primary driver is regulation. Any significant reversal or weakening of climate policies could dramatically reduce demand and undermine the economic case for CCU investment.

6. **Shortage of Specialized Talent:** The rapid growth of the sector has created a shortage of engineers and scientists with deep expertise in CCU technology development and integration, which can constrain the ability of companies to scale.

The most critical weakness is the intersection of **high capital costs** and **integration complexity**. This combination creates significant perceived risk for buyers, making proven reliability and strong technical partnership the most important factors in any purchasing decision.

### Sectoral Opportunities: The Catalysts for Future Growth

Beyond the current landscape, a wealth of opportunities exists for companies that can think strategically and act decisively.

[PLACEHOLDER - MARKET SWOT URL 2]

1. **Circular Economy Business Models:** The greatest opportunity lies in moving beyond simple carbon capture to **carbon utilization**. Developing partnerships with the chemical industry to create synthetic fuels, polymers, or other valuable materials from captured CO₂ opens up entirely new revenue streams.

2. **Direct Integration for Green Steel:** The "Direct Carbon Capture Technology Integration" segment is poised for explosive growth. Companies that can master the art of seamlessly embedding CCU technology into new "green steel" plant designs will become indispensable partners to the industry's pioneers.

3. **Data Monetization and Optimization Services:** The vast amount of operational data generated by CCU systems is a valuable asset. There is a significant opportunity to offer AI-powered analytics-as-a-service to help plants optimize their capture efficiency, manage compliance, and predict maintenance needs.

4. **Geographic Expansion into Emerging Markets:** While Europe and North America currently lead in CCU adoption, rapidly industrializing nations in Asia and other regions will soon face their own regulatory pressures, creating massive, untapped markets for CCU solutions.

5. **Technology Licensing and Joint Ventures:** For innovators with breakthrough technology, licensing their IP to larger players or forming joint ventures to scale can be a highly effective, capital-efficient way to penetrate the market.

6. **Market Consolidation:** The fragmented nature of the market, particularly among smaller innovators, presents an opportunity for strategic acquisitions. A roll-up strategy could create a technology powerhouse with a comprehensive portfolio of solutions.

### Global Threats: The Risks on the Horizon

Finally, companies must navigate a series of external threats that could disrupt the market's positive trajectory.

1. **Technological Disruption from Alternatives:** The biggest threat to CCU is the emergence of a superior, more cost-effective decarbonization technology. Breakthroughs in green hydrogen production or direct electrification of steelmaking could, in the long term, make post-combustion capture obsolete for new plants.

2. **Intense Competitive Rivalry:** The market is populated by large, well-funded incumbents and agile, aggressive innovators. This high level of competition can lead to pricing pressure and margin erosion for undifferentiated players.

3. **Regulatory and Policy Volatility:** As mentioned, the market is highly dependent on a stable policy environment. A shift in political winds or a global economic downturn could lead governments to relax emissions targets, weakening the business case for CCU.

4. **Supply Chain Vulnerabilities:** CCU systems rely on a stable supply of specialized inputs, such as amine solvents or sorbent materials. Disruptions in these supply chains, whether due to geopolitical events or resource scarcity, could halt projects and increase costs.

5. **Public Perception and Reputational Risk:** CCU technology is not without its critics. Any high-profile project failure or negative press around the long-term efficacy of carbon capture could damage public trust and create social license challenges.

6. **Cybersecurity Risks:** As CCU systems become increasingly digitized and connected, they become potential targets for cyber-attacks, which could disrupt operations across the entire steel production process.

The two invisible tensions revealed by our analysis are the clash between the **slow, capital-intensive pace of the steel industry** and the **fast, agile pace of technological innovation**, and the conflict between the need for **standardized, scalable solutions** and the demand for **highly customized, plant-specific integrations**.

The recommended offensive strategy is clear: **Focus on mastering the complexity of direct, customized integration**. While retrofit solutions offer a larger immediate market, true, defensible leadership will be built by becoming the indispensable technical partner for the next generation of green steel plants.

\*\*\*

## Section 5: 15+ AI Agent Concepts Designed for the Carbon Capture Utilization Tech Market

The complexity and high-stakes nature of the CCU technology market make it a prime candidate for augmentation by specialized AI agents. These are not futuristic fantasies; they are conceptual frameworks for practical tools that could solve today's most pressing challenges. By automating intelligence, optimizing processes, and providing predictive insights, these agents can transform every link in the value chain. What follow are not existing products, but concepts and ideas intended to illustrate a potential direction for the industry.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

### A. Two High-Impact AI Agent Concepts

Here are two conceptual agents designed to address critical market weaknesses and unlock significant value.

#### **Agent Concept 1: "Optima" - Predictive Maintenance & Operational Efficiency Agent**

- **Augmented Job Title:** Plant Operations Engineer, now equipped with a clairvoyant AI partner.

- **Problem Solved:** This agent tackles the immense financial and operational risk of unplanned downtime in a CCU system. A single failure can halt operations, incur massive costs, and jeopardize compliance.

- **How It Works:** "Optima" continuously ingests data from thousands of IoT sensors on pumps, valves, compressors, and chemical processors. Using machine learning models trained on historical performance and failure data, it predicts component degradation and potential failures weeks in advance. It doesn't just raise an alarm; it automatically schedules maintenance, orders necessary parts, and suggests optimized operational parameters to extend component life until the scheduled repair.

- **Concrete Use Case:** A steel plant's CCU system is running at 98% capacity. "Optima" detects a subtle vibration anomaly and a minor temperature increase in a critical solvent pump. It cross-references this with the pump's operational history and predicts a 75% probability of bearing failure within the next 3 weeks. It automatically schedules a maintenance window during a planned production slowdown, pre-orders the specific bearing model, and provides the maintenance team with a detailed work order, thus averting a catastrophic and costly mid-production failure.

- **KPIs Impacted:**

1. **Capture System Operational Availability:** Increases from a baseline of 95% to over 99%.

2. **Unplanned Downtime:** Reduced by up to 80%.

3. **Maintenance Costs:** Lowered by 20-30% through predictive rather than reactive or preventative schedules.

- **Game-Changer Impact:** "Optima" transforms the core value proposition from "we capture carbon" to "we guarantee carbon capture uptime," a far more powerful message for risk-averse steel producers.

#### **Agent Concept 2: "Scout" - Dynamic Regulatory Compliance & Policy Monitoring Agent**

- **Augmented Job Title:** Chief Compliance Officer, now empowered with an AI that reads and interprets global regulations 24/7.

- **Problem Solved:** The global regulatory landscape for carbon emissions is a complex, ever-changing patchwork of national laws, regional trading schemes (like the EU ETS), and local ordinances. Manually tracking and ensuring compliance is a monumental and error-prone task.

- **How It Works:** "Scout" uses Natural Language Processing (NLP) to continuously scan and ingest new legislation, policy updates, and carbon price fluctuations from government databases and regulatory bodies worldwide. It interprets these changes and translates them into specific, actionable compliance requirements for each of a company's plant locations. It can run simulations to forecast the financial impact of proposed policy changes and automatically flag potential non-compliance risks.

- **Concrete Use Case:** The European Commission proposes an amendment to the EU ETS that would change the allocation of free carbon allowances for the steel sector. "Scout" immediately detects this, analyzes the 200-page document, and sends an alert to the CSO with a summary: "Proposed amendment will decrease our free allowances by 15% starting in 2028, creating a potential €50M annual cost increase. Recommending initiation of our Phase 2 decarbonization plan 6 months ahead of schedule."

- **KPIs Impacted:**

1. **Compliance Fines and Penalties:** Reduced to zero.

2. **Regulatory Reporting Time:** Automated and reduced by over 90%.

3. **Financial Forecasting Accuracy:** Improved by incorporating predictive policy impact.

- **Game-Changer Impact:** "Scout" turns regulatory risk into a competitive advantage. Companies using it can adapt to policy changes faster, optimize their compliance strategy, and make more informed long-term capital investments.

### B. A Full Roster of Specialized AI Agent Concepts

The potential for AI augmentation extends across the entire value chain. Here are ten additional concepts:

[PLACEHOLDER - MARKET SWOT PRIORITY URL]

1. **Faye (Market Demand Forecaster):** Augments **Business Development Managers** by predicting CCU demand by region and technology type, identifying white-space opportunities for expansion.

2. **Max (Capital Investment Optimizer):** Augments **CFOs and CAPEX Committees** by simulating the IRR and risk profile of various CCU projects to optimize capital allocation.

3. **Sage (Competitive & IP Intelligence):** Augments **Strategy Teams** by monitoring patent filings and competitor R&D, providing early warnings of new technological threats.

4. **Echo (Supply Chain Resilience Agent):** Augments **Procurement Managers** by modeling risks in the supply of critical materials (e.g., solvents) and recommending alternative sourcing strategies.

5. **Bridge (Stakeholder Engagement Analyst):** Augments **Corporate Communications Teams** by analyzing public and investor sentiment around CCU projects to manage reputational risk.

6. **Insight (Ecosystem Collaboration Mapper):** Augments **Strategic Alliance Managers** by identifying and scoring potential partners across the steel, chemical, and energy sectors to build powerful ecosystems.

7. **Horizon (Disruption Trend Scanner):** Augments **R&D Leadership** by scanning scientific literature and startup activity to identify emerging decarbonization technologies that could threaten the CCU market.

8. **Prime (Customer Lifecycle Manager):** Augments **Account Managers** by predicting churn risk and identifying upsell opportunities for long-term service and upgrade contracts.

9. **Summit (Digital Twin Retrofit Planner):** Augments **Integration Engineers** by creating a virtual model of a steel plant to simulate and de-risk the integration of CCU technology before any physical work begins.

10. **Capital (Dynamic Pricing Engine):** Augments **Sales & Finance Teams** by enabling performance-based contracts where pricing is tied dynamically to the volume of CO₂ captured and the market price of carbon.

### C. The Ultimate Vision: A Coordinated System of AI Agents

While individual agents are powerful, the ultimate vision is a fully integrated **system of interdependent AI agents**, working in concert and orchestrated by a master agent. This creates a neural network for the entire business, enabling a level of efficiency and strategic agility that is impossible to achieve with human coordination alone.

[PLACEHOLDER - MARKET AGENT SYSTEM URL]

Imagine a **"Forge Command Center,"** a master orchestrator AI that oversees the entire CCU value chain. It augments the **Operations Manager**, giving them a real-time, holistic view of the business. This orchestrator coordinates the actions of five specialized sub-agents:

- **SourceScout (Raw Materials Agent):** Optimizes the sourcing of materials needed for CCU.

- **ForgeMax (Steel Production Agent):** Ensures the steel production process is optimized for carbon capture.

- **EcoPulse (CCU Technology Agent):** Manages the performance and innovation pipeline of the capture technology itself.

- **BreatheGuard (Emissions & Compliance Agent):** Monitors all emissions and guarantees regulatory compliance in real-time.

- **AllyBridge (Industrial Partnerships Agent):** Manages relationships and joint projects with partners in the ecosystem.

When the **Forge Command Center** detects a market opportunity for a new synthetic fuel (identified by **Faye**), it can direct **AllyBridge** to secure a partnership, task **EcoPulse** to fine-tune the capture process for the required CO₂ purity, and instruct **ForgeMax** and **SourceScout** to adjust their operations accordingly, all while **BreatheGuard** ensures every step remains compliant. This is the future of industrial management: a synchronized, intelligent, AI-augmented system that not only executes strategy but actively shapes it in real time.

\*\*\*

## Section 6: Our Value Proposition for PeroCycle

PeroCycle has strong potential to become a significant player in the steel decarbonisation market within 10 years due to its unique retrofit-compatible technology, strong IP from University of Birmingham, backing from major mining company Anglo American, and ability to work with existing steel infrastructure rather than requiring completely new plants.

\*\*\*

### Conclusion & Strategic Exchange

Our deep dive into the Carbon Capture Utilization technology market for steel manufacturing has revealed a sector at a pivotal moment. It is no longer a question of _if_ the industry will adopt CCU, but _how_ and _who_ will lead the charge.

**Key Insights Synthesized:**

The market is a robust and growing **€8 billion** opportunity, propelled by an undeniable regulatory tailwind. It is clearly segmented into three distinct arenas—**compliance-driven retrofitting**, **innovation-led utilization**, and **visionary direct integration**—each demanding its own unique go-to-market strategy. The competitive landscape is dominated by incumbents like **Mitsubishi Heavy Industries** and **Carbon Clean**, whose power is rooted in mature technology and entrenched market access. However, the field is ripe for disruption by agile challengers like **H2 Green Steel** and innovators like **LanzaTech**. The market's structural strength lies in its non-discretionary demand and high switching costs, but it is critically hampered by high capital requirements and extreme integration complexity. The most profound opportunity lies not just in capturing carbon, but in leveraging AI to master the entire value chain, transforming a complex industrial process into a seamlessly optimized, intelligent system.

**Sectoral Findings:**

The trajectory of the CCU market is clear: it is moving from a cost center for compliance to a potential value-creation engine. The most pressing priority is solving the dual challenge of high capital investment and technical integration risk. It is here that artificial intelligence will play its most decisive role. AI will not be a mere add-on; it will become the core operating system for the next generation of sustainable industry, enabling the predictive maintenance, regulatory agility, and ecosystem coordination necessary to make large-scale decarbonization a reality.

If you are interested in this topic you can follow these next steps:

1️⃣ **Download below the full Carbon Capture Utilization Tech market study in pdf format**

2️⃣ **Get additional insights of this market by reading our memo of an interesting company in this market called PeroCycle (Cutting CO₂ emissions in steelmaking sustainably)**

3️⃣ **If you want us to build a custom AI system and dedicated AI agents, book a strategic discussion with an AI Partner: https://forms.proplace.co/meet**