.png)

The Biometric payment solution market by our Market Intelligence AI agent

Here is the complete blog post, generated according to your specifications.

***

# The Future of Payments is in Your Hand: A Deep Dive into the Biometric Payment Solutions Market

**Meta Description:** An in-depth analysis of the Biometric Payment Solution sector. Explore market size, go-to-market strategies, competitive dynamics, and AI-driven opportunities revealed through automated market intelligence.

**Keywords:** Biometric payment solution, biometric payments artificial intelligence, AI market analysis, biometric payments 2025, AI agents for biometric payments, palm vein payment, retail technology trends.

***

## Introduction: Beyond the Hype, a €9.5 Billion Revolution

The world of retail technology is in constant flux, but few shifts are as profound or as personal as the move towards biometric payments. This isn't just about convenience; it's a fundamental reshaping of the trust, security, and speed at the heart of every transaction. The biometric payment solutions market is a coveted island of opportunity, valued at an impressive **€9.5 billion** and charting a vigorous **18% annual growth rate**. Yet, navigating these waters requires more than a simple map. Formidable ships, including established leaders like **IDEMIA** and **Fujitsu**, alongside agile innovators such as **Natural Security**, are all vying for dominance in this lucrative territory.

The conventional view often lumps all biometric technologies together, focusing on the mainstream adoption of fingerprint and facial recognition. However, a deeper, AI-augmented analysis reveals a more nuanced reality. It uncovers the subtle but powerful currents of regulatory pressure, consumer privacy sentiment, and technological maturation that are creating unprecedented opportunities for those who can see them.

This comprehensive analysis moves beyond surface-level trends to provide a strategic deep dive into the biometric payment solutions landscape. We will dissect the market's core segments, revealing their unique dynamics and growth trajectories. We will outline three distinct go-to-market playbooks tailored to capture value in each segment. We will map the competitive arena to identify who truly holds the power and what it takes to challenge the incumbents. Finally, we will conduct a full SWOT analysis and unveil a suite of specialized AI agents designed to navigate this complex environment, transforming challenges into strategic advantages. The key insight we will repeatedly return to is this: while fingerprint and facial recognition currently dominate, the less invasive, more private, and highly secure palm vein scanning segment is poised for disruptive growth, representing a critical pivot point that many are underestimating. Welcome to the future of payments.

[PLACEHOLDER - YOUR MARKET URL]

## Section 1: A Complete Panorama of the Biometric Payment Solutions Market

The biometric payment solutions market represents a significant and rapidly expanding frontier within retail technology. Fueled by a global push towards more secure, frictionless, and—critically, in a post-pandemic world—contactless interactions, its growth trajectory is both steep and sustained. The market’s Total Addressable Market (TAM) stands at a formidable **€9.5 billion**, with a projected compound annual growth rate (CAGR) of **18%**. This expansion is not speculative; it's anchored in real-world demand from retail chains, supermarkets, hospitality, and specialty stores grappling with fraud, operational inefficiencies, and the ever-higher expectations of modern consumers.

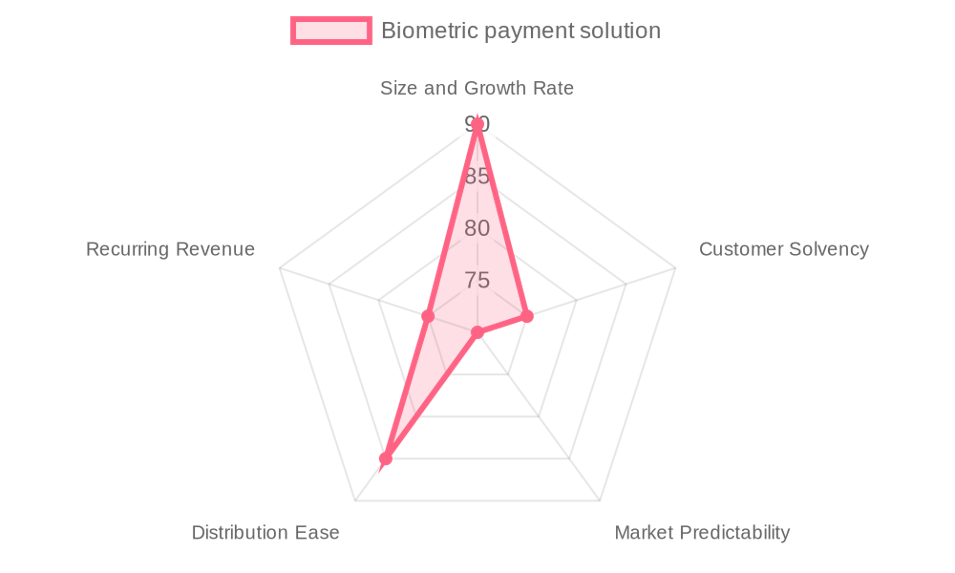

This vibrant market is best understood by dissecting its core components. While the global opportunity is vast, strategic focus is paramount. The Serviceable Addressable Market (SAM) for a player focused on European retail with advanced palm scanning solutions is estimated at a substantial **€1.2 billion**. From this, a focused company like **Handwave** could realistically target a Serviceable Obtainable Market (SOM) of **€60 million** over a 3-5 year horizon, representing a 5% share of this high-potential segment. The market's attractiveness is underscored by a composite score of **82 out of 100**, reflecting its exceptional size and growth, healthy customer solvency, and accessible distribution channels. Key performance indicators in this sector set a high bar, with top-tier players achieving a system uptime of **99.95%** and maintaining healthy gross margins of around **55%**, signaling a mature yet highly profitable operational environment.

To truly grasp the strategic landscape, we must analyze the three primary technology segments that constitute this market.

### Segment 1: Palm Scanning Biometrics (30% Market Share)

Representing approximately **30%** of the total market, palm scanning biometrics is the fastest-growing segment, with an impressive year-over-year growth rate of **18-20%**. Its primary advantage lies in superior security. By scanning the unique vein patterns within a person's palm, a method far more difficult to replicate than a fingerprint or facial image, it offers a robust layer of protection. This technology inherently includes **liveness detection**, ensuring a real hand is present, which critically mitigates spoofing attacks. From a consumer perspective, it is less invasive and more socially acceptable than facial recognition, a crucial factor in public retail environments.

The target audience for this technology includes security-conscious businesses, particularly retailers of age-restricted items (like alcohol or tobacco) who can leverage it for seamless age verification, and large chains seeking to reduce checkout times and prevent fraud. The buying cycle is typically measured in months (3-6), involving rigorous technology trials and point-of-sale (POS) integration testing. Key decision-makers include IT Managers, CFOs, and Operations Directors, whose primary concerns revolve around security robustness, ease of integration, and a clear cost-benefit analysis.

### Segment 2: Fingerprint and Facial Recognition (50% Market Share)

This segment is the current market heavyweight, accounting for roughly **50%** of the total market, though its growth is more moderate at **15% YoY**. These technologies are widely adopted and familiar to consumers through smartphones and other devices, leading to faster, more established use cases. However, this familiarity comes with trade-offs. While quick, these methods can be less secure than vein-based biometrics and are more susceptible to false positives and negatives.

The most significant headwind for this segment, particularly for facial recognition, is the growing cloud of privacy concerns and regulatory scrutiny. Legislations like GDPR in Europe and state-level laws in the US (like BIPA and CCPA) place strict limitations on the collection and storage of facial data. This makes the target audience—global retail chains and e-commerce players with an offline presence—increasingly cautious. Their decision-making process, often shorter at 1-3 months, is heavily weighted by regulatory compliance, customer acceptance, and price. Objections frequently center on the risk of privacy legislation changes, potential customer pushback, and the accuracy of the technology.

### Segment 3: Other Emerging Biometrics (Iris, Voice) (20% Market Share)

Constituting the remaining **20%** of the market, emerging biometric technologies like iris and voice recognition are the wildcard segment, boasting the highest potential growth rate at over **25% YoY**. These are currently niche applications, often deployed in specialized or premium environments where cutting-edge technology serves as a key differentiator. For example, luxury retail might use iris scanning for high-value clienteling, while voice biometrics could find a home in drive-thru or hands-free payment scenarios.

The primary barriers to wider adoption are high cost, technological maturity, and the complexity of integration. The buying cycle is consequently the longest, often exceeding six months and requiring extensive pilot programs and proof-of-concept validation. The decision to adopt is driven less by immediate operational efficiency and more by the pursuit of an innovative advantage and the highest possible level of security. CIOs and Innovation Managers are the key decision-makers, and they require compelling evidence of return on investment and scalability before committing.

These segments are not siloed; they exist in a dynamic interplay of technology, regulation, and consumer behavior. The overarching trend is a move towards AI-enhanced, multi-modal solutions that combine the strengths of different biometrics to deliver unparalleled security and convenience.

## Section 2: Three Winning Go-To-Market Playbooks: How to Conquer Each Segment

Success in the biometric payment solutions market is not a one-size-fits-all proposition. The distinct characteristics of each technology segment demand a tailored go-to-market (GTM) strategy. An analysis of the market reveals three potentially winning playbooks, each designed to resonate with the specific needs, pains, and buying behaviors of its target audience.

### A. The "Security & Efficiency" Playbook for Palm Scanning Biometrics

[PLACEHOLDER - GTM_1 IMAGE]

This GTM strategy is engineered for the **Palm Scanning Biometrics** segment, where the core value proposition is unbreachable security combined with operational excellence.

* **Ideal Customer Profile (ICP):** The target is a B2B retail chain in Europe, North America, or APAC with **50-5,000 employees** and revenues between **€50M-€1B**. These companies possess a high technological maturity, allocate an annual budget of €500K-€5M for biometric tech, and operate on a 3-6 month decision timeline. They are often early adopters, driven by a need to protect their bottom line from fraud and enhance the customer experience.

* **Winning Persona & Obsessions:** The key decision-maker is often the **Retail IT Manager**, who reports to the CIO or CTO. This individual is obsessed with three primary goals:

1. **Selecting Secure & Seamless Technology:** They are tasked with finding a payment authentication method that is virtually fraud-proof without creating friction for the customer.

2. **Ensuring Operational Efficiency:** Their success is measured by metrics like reduced checkout times and lower rates of transaction fraud.

3. **Meeting Compliance for Age Verification:** In many retail environments, a solution that simplifies and secures the sale of age-restricted goods is a massive operational win.

* **Top Acquisition Channels & Buying Triggers:** The most effective channels are highly targeted and professional. This includes **B2B trade shows** (like NRF), specialized **retail technology conferences**, direct sales outreach, and partnerships with technology integrators. The primary buying trigger is often a security incident, mounting pressure from fraud losses, or new regulatory mandates for age verification.

* **The 4-Step Acquisition Process:**

1. **Awareness:** Generate visibility through thought leadership content (whitepapers on biometric security ROI) and a strong presence at industry events.

2. **Consideration:** Nurture leads with detailed case studies, customer testimonials, and direct outreach showing how Handwave's technology reduces checkout time to as little as four seconds.

3. **Trial:** Offer a structured, low-risk pilot program to allow prospects to test the technology and its integration ease within their own POS environment.

4. **Conversion:** Close the deal by presenting a clear cost-benefit analysis, addressing privacy concerns head-on (highlighting the privacy-focused design of palm vein tech), and showcasing a seamless integration roadmap.

* **Key Insight for this Segment:** The winning message is not just about security; it's about **secure efficiency**. By demonstrating a tangible ROI through reduced fraud, faster checkout, and simplified compliance, providers can justify the upfront investment and overcome objections related to implementation complexity.

### B. The "Compliance & Trust" Playbook for Fingerprint and Facial Recognition

[PLACEHOLDER - GTM_2 IMAGE]

This playbook is designed for the mature but sensitive **Fingerprint and Facial Recognition** segment, where navigating privacy and regulation is as important as the technology itself.

* **Ideal Customer Profile (ICP):** This profile shifts to larger, global retail chains with **100-10,000 employees** and revenues from **€100M-€5B**. These are often omnichannel retailers with a significant presence in North America and Europe, where regulatory frameworks are most stringent. Their biometric tech budget ranges from €0.5M-€3M, with a swifter 1-3 month decision timeline driven by compliance deadlines or digital transformation projects.

* **Winning Persona & Obsessions:** The central figure here is the **Security Officer**, who reports to the CISO or CIO. Their obsessions are markedly different:

1. **Deploying Compliant Technology:** Their primary job is to ensure any deployed biometric solution adheres to a complex web of privacy laws (GDPR, BIPA), minimizing the company's legal and financial risk.

2. **Balancing Customer Acceptance with Security:** They must find a solution that customers will actually use without significant resistance, which means minimizing false rejections and addressing privacy fears transparently.

3. **Ensuring ROI with Minimal Risk:** This persona is highly price-sensitive and risk-averse, focusing on proven technologies that deliver measurable results without opening the door to lawsuits or reputational damage.

* **Top Acquisition Channels & Buying Triggers:** Trust and authority are key. **Industry webinars featuring privacy experts** are a prime channel, alongside targeted LinkedIn campaigns. Partnerships with retail technology consultants specializing in compliance are also crucial. The buying trigger is almost always external pressure: an impending compliance deadline, news of a competitor's data breach, or a corporate-wide digital transformation initiative that includes updating payment systems.

* **The 4-Step Acquisition Process:**

1. **Education:** Build trust by providing high-value content like compliance checklists, analyst reports, and webinars that address privacy concerns directly.

2. **Validation:** Share case studies focused specifically on successful and compliant deployments of facial or fingerprint biometrics.

3. **Consultation:** Engage prospects with a consultative sales approach, focusing on a needs assessment around their specific compliance challenges and offering a tailored solution.

4. **Assurance:** Close by providing strong assurances on technology accuracy, offering flexible pricing models, and highlighting certifications and client references that build confidence.

* **Key Insight for this Segment:** The conversation must lead with **privacy and compliance**, not features. By positioning the solution as the safest, most compliant choice that mitigates risk, providers can win the trust of security-conscious buyers and differentiate themselves in a crowded field.

### C. The "Innovation & Exclusivity" Playbook for Emerging Biometrics

[PLACEHOLDER - GTM_3 IMAGE]

This playbook targets the niche but high-potential **Emerging Biometrics (Iris, Voice)** segment, where the goal is to sell a competitive advantage, not just a payment solution.

* **Ideal Customer Profile (ICP):** The focus is on premium or luxury retail and specialized service providers, typically with **100-500 employees** and revenues of **€20M-€200M**. These companies are innovation-driven, early adopters, and see technology as a way to enhance their brand's exclusivity. Their biometric tech budget is smaller (€0.3M-€1M), and their decision timeline is long (6+ months) due to the pioneering nature of these solutions.

* **Winning Persona & Obsessions:** The **Chief Information Officer (CIO)** or **Innovation Manager** is the key decision-maker. Their mandate is to look to the future, and their obsessions reflect this:

1. **Pioneering Cutting-Edge Technology for Differentiation:** They want to be the first, to offer an experience no one else can, and to use technology to amplify their brand's premium positioning.

2. **Ensuring Security Through Rigorous Validation:** While innovative, they cannot afford a security failure. Proof-of-concept validation is non-negotiable.

3. **Measuring Success by Innovation Impact:** The ROI is measured not just in dollars, but in brand equity, press coverage, and a strengthened reputation for being ahead of the curve.

* **Top Acquisition Channels & Buying Triggers:** Engagement happens where innovation is discussed. This includes **sponsorships at innovation conferences**, participation in exclusive **technology pilot programs**, and highly targeted outreach within niche LinkedIn groups. The buying trigger is internal: a strategic decision to seek brand differentiation or a need for an ultra-high-security solution that existing technologies cannot provide.

* **The 4-Step Acquisition Process:**

1. **Inspiration:** Showcase the art of the possible with visionary content, pilot results from other industries, and exclusive-invite webinars with technology pioneers.

2. **Collaboration:** Position the engagement as a co-innovation partnership rather than a sale. Offer to build a custom proof-of-concept tailored to their unique environment.

3. **Validation:** Execute a flawless pilot program, providing extensive data and support to prove the technology's effectiveness, security, and ROI.

4. **Partnership:** Formalize the relationship with a long-term agreement that emphasizes continuous innovation and a shared journey of technological leadership.

* **Key Insight for this Segment:** The sale is about selling a **strategic vision of exclusivity**. The conversation should focus on brand enhancement, competitive differentiation, and the "wow factor" of being a technology pioneer. Price is secondary to the innovative advantage gained.

By understanding these nuances, a company can allocate its resources effectively, deploying a security-focused message for palm scanning, a trust-based message for facial/fingerprint, and an innovation-driven message for emerging biometrics, thereby maximizing its potential to capture a significant share of this dynamic €9.5 billion market.

## Section 3: Who Truly Holds the Power in the Biometric Payment Solutions Market?

Understanding the competitive landscape of the biometric payment solutions market requires looking beyond a simple list of companies. It requires an analysis of the underlying forces that shape profitability, the axes upon which competition pivots, and the strategic positioning of key players. This is a marketplace defined by intense rivalry, but also by immense potential for differentiation.

[PLACEHOLDER - COMPETITION QUADRANT URL]

### A. The Value Chain and the Battle for Control

The market's value chain flows from core technology development (sensors, algorithms) through to system integration (POS hardware and software) and finally to the end-user deployment in retail environments. An analysis based on Porter's Five Forces reveals where the power truly lies:

* **Rivalry Among Competitors (High):** The field is crowded. Established giants like **IDEMIA** and **Fujitsu** compete fiercely on reliability and large-scale integrations, while innovators like **Natural Security** differentiate with advanced AI. The market's strong 18% growth provides room for many to operate, but the fight for flagship accounts is intense, with significant marketing investments, particularly at major retail technology trade shows.

* **Power of Buyers (High):** The customers—primarily retail chains—wield considerable power. Modern POS systems are often modular, which lowers the cost and complexity of switching between biometric providers. Large retail groups can command significant price concessions and demand complex customizations, tilting negotiations in their favor. The transparency of public tenders, especially in Europe, further strengthens their position.

* **Power of Suppliers (Medium):** The providers of specialized components, such as biometric sensors (**Synaptics** is a key player), hold some power due to market concentration. Furthermore, the scarcity of specialized talent—experts in AI and biometric engineering—acts as a supplier-side constraint, giving these professionals significant leverage.

* **Threat of New Entrants (Medium):** While the technical sophistication and R&D investment required to build a secure, scalable biometric solution create a tangible barrier, the market'slucrative nature is a powerful magnet for innovative startups. Companies like **VoicePIN** have successfully carved out a niche in voice biometrics, demonstrating that entry is possible for focused and well-funded newcomers. However, established players benefit from economies of scale and control over key distribution channels through integrator partnerships.

* **Threat of Substitutes (Medium):** Traditional contactless payment methods, such as NFC-enabled cards and mobile wallets, represent a constant substitute. While biometrics offer superior security and added value (like age verification), the convenience and ubiquity of these alternatives exert downward pressure on pricing and create a baseline for user experience that biometrics must exceed.

**Insight:** The power in this market is not held by a single entity but exists in a tense equilibrium. While technology developers hold the keys to innovation, **the end customers (retailers) ultimately dictate the terms of engagement**, forcing providers to compete intensely on integration, price, and demonstrable ROI.

### B. The Two Axes of Differentiation

In this highly competitive environment, success hinges on excelling along two critical axes of differentiation:

1. **Technological Innovation:** This is the ability to develop and deploy advanced biometric solutions that are not just accurate but also fortified with cutting-edge features. This includes the use of AI for enhanced fraud and spoof detection, the development of multi-modal systems that fuse different biometrics for higher security, and the engineering of privacy-preserving architectures that earn consumer and regulatory trust. In a market where security is paramount, a tangible technological edge is the most defensible competitive advantage.

2. **Integration Capability & Partnerships:** A groundbreaking technology is commercially useless if it cannot be seamlessly integrated into a retailer's existing infrastructure. This axis represents the ability to easily connect with a wide array of POS systems, ERPs, and loyalty platforms. It is amplified by a strong network of partnerships with system integrators, technology consultants, and payment gateway providers who control access to the end customer. Strong integration capability dramatically reduces a retailer's adoption friction and accelerates the sales cycle.

The primary tension in the market lies at the intersection of these two axes. Pure-play innovators may possess superior technology but lack the integration network to scale, while large, established players may have the network but lag on the innovation curve. The ultimate winners will be those who can master both.

### C. Mapping the Key Commercial Players

An analysis of the key players based on their technological innovation and integration capabilities reveals four distinct strategic clusters:

* **Leaders:** These companies demonstrate excellence on both axes. **IDEMIA** is the archetypal leader, combining world-class palm vein recognition technology with a vast global network of banking and retail partnerships, giving it unparalleled integration capabilities.

* **Specialists:** These players are defined by their deep technological innovation in a specific niche but have a more limited integration reach. **Natural Security**, with its focus on AI-enhanced palm biometrics, and **VoicePIN**, a pioneer in voice authentication, fall into this category. They offer highly advanced solutions but currently lack the broad distribution network of the leaders.

* **Accessibles:** These companies have strong integration capabilities and market access but may not be at the absolute cutting edge of technological innovation across all modalities. **Fujitsu** is a prime example, with its robust and widely deployed palm scanning solutions and deep industrial expertise, making it a solid and reliable choice for many retailers. **Clearway Biometrics** also fits here, focusing on easy-to-integrate, API-driven facial recognition solutions.

* **Followers:** This quadrant is currently sparse, as the market's rapid pace of change and high technical bar make it difficult for companies with low innovation and limited integration to survive.

### D. Analysis of Market Leaders

The leadership tier of the biometric payments market is composed of titans from the payments, technology, and security industries. The primary leader cited for direct biometric payment systems is **IDEMIA**, but the broader ecosystem is dominated by entities like **Mastercard, Visa, Amazon (Amazon One), Apple (Apple Pay), Google (Google Pay), PayPal, Stripe, Square, Microsoft (Azure biometrics),** and **IBM (biometric solutions)**.

**IDEMIA** stands out as a direct leader, with an estimated $900 million in annual revenue from its biometric payment segment. Its strategy is built on a foundation of deep R&D in secure identity, which translates into highly trusted and robust palm vein and facial recognition technologies. Their strength is not just the technology itself, but their ability to navigate complex regulatory environments and forge deep partnerships with major financial institutions and governments worldwide. This gives them a formidable moat built on trust, scale, and integration.

The broader set of leaders like **Mastercard** and **Visa** are not typically building the biometric sensors themselves. Instead, their strategy is to create and control the payment *rails* and authentication *frameworks* upon which these new technologies operate. They are actively integrating biometric capabilities into their own payment standards (e.g., using a phone's fingerprint sensor for Apple Pay authentication on a Mastercard transaction). Their power comes from their ubiquitous network and their ability to set the standards for security and interoperability, effectively making them a mandatory partner for any new biometric solution that wants to achieve mass adoption. Companies like **Apple** and **Google** leverage their control of the mobile operating system to embed biometrics deeply into the consumer experience, while giants like **Microsoft** and **IBM** provide the powerful cloud and AI infrastructure needed to process biometric data securely at scale.

### E. Focus on the Challengers

The challenger landscape is vibrant and diverse, populated by focused innovators and disruptive giants. This group includes players like **Amazon One, Worldcoin, Clear, BioConnect, Neurotechnology, Veridium, HYPR, Nymi, TouchByte,** and **Fujitsu's PalmSecure** (which acts as both an established solution and a challenger to broader payment networks).

The most formidable challenger is arguably **Amazon One**. Amazon's strategy is to leverage its immense retail footprint (Whole Foods, Amazon Go) and customer base to rapidly scale its palm recognition payment system. Unlike other players who need to sell their technology to retailers, Amazon *is* the retailer. This gives it a massive advantage in deploying and refining its technology in a live environment. Its disruptive potential comes from its ability to create a closed-loop ecosystem where the shopping and payment experience are seamlessly unified, potentially bypassing traditional payment networks.

Other notable challengers are attacking the market from different angles. **Natural Security** focuses on being the best-in-breed on AI-powered palm scanning, hoping to win on pure technological superiority. **VoicePIN** targets the niche but growing market for voice payments. The innovative but controversial **Worldcoin** is attempting to build a new identity and financial network based on iris scans. A company like **Handwave** shows significant potential by pursuing a smartphone-first approach to palm biometrics, aiming to eliminate the need for dedicated hardware and thus lower the barrier to entry for retailers. Its success will hinge on its ability to secure regulatory approvals and forge the strategic partnerships needed to compete with the likes of Amazon One. These challengers, while smaller, are critical to the market's evolution, pushing the boundaries of technology and forcing the leaders to constantly innovate.

## Section 4: A Strategic SWOT Analysis of the Biometric Payments Market

A comprehensive SWOT analysis reveals the structural forces that define the biometric payment solutions market. It highlights the deep-rooted strengths and opportunities that make it so attractive, while also exposing the critical vulnerabilities and looming threats that demand strategic foresight. AI's role is transformative, acting as a powerful lever to amplify strengths, mitigate weaknesses, seize opportunities, and defend against threats.

[PLACEHOLDER - MARKET SWOT URL]

### STRENGTHS: The Market's Solid Foundation

The market is built on a powerful and resilient foundation, characterized by strong fundamentals and clear demand drivers.

* **Massive Market & Growth:** The most evident strength is the sheer scale of the opportunity. A **€9.5 billion TAM** growing at an **18% CAGR** provides a vast and expanding field for competition and value creation.

* **Recurring Revenue Models:** The business model is inherently stable. Providers benefit from recurring revenue streams through **SaaS fees, ongoing hardware maintenance contracts, and value-added loyalty program integrations**, ensuring financial predictability.

* **Powerful Demand Drivers:** The market is not built on speculation. There is a tangible consumer pull for **secure, contactless payment methods**, a trend massively accelerated by post-COVID hygiene concerns.

* **Regulatory Impetus:** Rising regulatory requirements for **fraud reduction and age verification** are not a burden but a demand driver, pushing retailers toward more sophisticated and reliable biometric solutions.

* **High Differentiation Potential:** The intensity of R&D encourages continuous innovation. This creates a healthy competitive dynamic where providers can genuinely differentiate themselves through **superior AI-powered fraud detection or multi-modal fusion**, rather than competing solely on price.

* **Accessible Distribution Channels:** The path to the customer is well-defined. A mature ecosystem of **B2B distribution channels**, including technology vendors, system integrators, and direct sales forces, makes it relatively easy to reach target customers.

* **Strong Partnership Ecosystems:** The market thrives on collaboration. Robust partnerships with **POS integrators and retail technology platforms** are a key strength, enhancing market reach and accelerating solution deployment.

* **Rapid Innovation Cycles:** The pace of innovation is a strength, with new capabilities in **AI-enhanced scanning and multi-modal authentication** emerging every 1-2 years, keeping the market dynamic and driving continuous improvement.

* **Attractive Financial Metrics:** The sector demonstrates strong financial health, with market-level **IRRs around 14-16%** and valuation premiums for AI-enabled players, attracting significant investment.

* **Privacy-Enhancing Technology as a Driver:** Paradoxically, stringent privacy regulations like GDPR have become a strength for certain segments. They drive the adoption of more secure and privacy-by-design technologies like **palm vein scanning**, which are inherently less invasive and store less identifiable data.

[PLACEHOLDER - MARKET SWOT URL 2]

### WEAKNESSES: Critical Structural Vulnerabilities

Despite its strengths, the market is not without its structural weaknesses that can impede growth and challenge profitability.

* **Regulatory Complexity & Fragmentation:** While a driver, regulation is also a weakness. The patchwork of **multijurisdictional biometric data privacy laws** (GDPR, CCPA, BIPA) imposes high compliance costs and creates uneven adoption speeds across regions.

* **High Capital Intensity:** The significant upfront investment required for **R&D and infrastructure development** creates high capital intensity, which can strain the finances of smaller providers and act as a barrier to entry.

* **Long and Complex Sales Cycles:** The sales process is rarely quick. Typical sales cycles of **3-6 months or longer**, involving extensive trials and security reviews, can strain cash flow and slow time-to-revenue.

* **Integration Complexity:** A major friction point is the **difficulty of integrating with legacy POS and payment infrastructures**, which can slow down or halt deployments and frustrate retail customers.

* **Consumer Privacy Concerns:** Public skepticism and privacy concerns, particularly around **facial recognition**, can create significant customer resistance and slow market adoption, regardless of the technology's effectiveness.

* **Talent Scarcity:** There is a pronounced **shortage of experts with deep domain knowledge in both AI and biometrics**, which limits the ability of companies to innovate and scale rapidly.

* **Dependence on Component Suppliers:** The market's reliance on a handful of specialized providers for critical components like **biometric sensors** creates supply chain vulnerabilities and pricing pressure.

* **High Buyer Power:** As noted in the Porter's analysis, the high power of retail buyers, combined with relatively low switching costs due to modular POS architectures, leads to **intense price competition** and can erode margins.

* **Unproven Scalability of Emerging Tech:** Newer modalities like iris and voice recognition face challenges with **unproven scalability and long proof-of-concept cycles**, making them a risky bet for many retailers.

* **Geographic Concentration:** Market adoption is heavily concentrated in **North America, Europe, and parts of Asia-Pacific**, exposing providers to regional economic downturns or regulatory shocks.

### OPPORTUNITIES: Catalysts for Future Growth

The landscape is fertile with opportunities for strategic growth, driven by technological evolution and changing market needs.

* **AI-Enhanced Multi-Modal Authentication:** The biggest technological opportunity lies in combining different biometric inputs (e.g., palm and voice) and using **AI to fuse them into a single, ultra-secure authentication event**. This dramatically improves accuracy and spoof detection.

* **Expansion into Underserved Segments:** There is a massive, underserved opportunity among **small and medium-sized retailers**. Developing scalable, cost-effective SaaS models could unlock this vast market segment.

* **Niche Markets with High-Value Needs:** Specialized markets like **luxury retail and controlled-item sellers** (e.g., cannabis dispensaries) are ripe for the adoption of advanced biometrics that offer both premium experience and ironclad compliance.

* **Integrating Payments with Value-Added Services:** The opportunity extends beyond the transaction. Integrating biometric authentication with **loyalty programs and personalized marketing** creates a much richer value proposition for retailers.

* **Growth in Emerging Markets:** As digital infrastructure improves in regions like Latin America, Southeast Asia, and Africa, there are significant **geographic expansion opportunities** beyond the currently dominant markets.

* **Blockchain Integration for Enhanced Security:** Combining biometrics with blockchain offers the potential for **immutable, decentralized transaction authentication**, representing a new frontier in payment security and trust.

* **Shift to SaaS and Subscription Models:** Moving away from one-time hardware sales to **subscription-based pricing** offers providers more predictable revenue streams and fosters long-term customer relationships.

* **Platform Ecosystem Development:** There is a significant opportunity to build **biometric authentication platforms** that are not tied to a single use case, allowing expansion into adjacent markets like secure access control, identity management, and healthcare.

* **Data Monetization:** While navigating privacy regulations carefully, there is potential to monetize **anonymized and aggregated behavioral data** to provide valuable analytics and insights back to retailers.

* **Crisis-Driven Adoption:** Unfortunately, global crises like pandemics can act as powerful catalysts, massively **accelerating the consumer shift to contactless and hygienic technologies**, creating sustained tailwinds for the market.

### THREATS: Looming Market Risk Factors

Providers must navigate a landscape fraught with external threats that could disrupt growth and threaten viability.

* **Intensifying Competitive Pressure:** The market's attractiveness has drawn intense competition not just from direct rivals but also from tech giants, leading to **pricing pressure and a risk of commoditization**.

* **Rapid Technological Obsolescence:** The fast pace of innovation is also a threat. A breakthrough in one modality could **rapidly render existing systems obsolete**, requiring continuous and costly R&D investment to keep pace.

* **Evolving and Punitive Regulations:** The regulatory environment is a double-edged sword. A sudden tightening of **biometric data laws or a court ruling that creates new liabilities** could instantly derail deployments and create significant financial risk.

* **Cybersecurity and Data Breaches:** Biometric databases are an extremely high-value target for cybercriminals. A significant data breach could be an **extinction-level event for a provider**, destroying trust and reputation overnight.

* **Public Sentiment and Misinformation:** The market is vulnerable to shifts in public perception. A viral news story or a targeted **misinformation campaign about the dangers of biometrics** could sour consumer sentiment and trigger political backlash.

* **Substitution by Alternative Technologies:** The threat from substitutes like **advanced NFC or QR code-based payment systems** remains. If these technologies evolve to offer a "good enough" level of security and convenience at a lower cost, they could cap the growth of biometrics.

* **Economic Volatility:** An economic downturn could threaten the market by reducing consumer spending and causing retailers to **delay or cancel capital-intensive technology upgrade projects**.

* **Geopolitical and Supply Chain Risks:** Global trade tensions or disruptions to the supply chain for critical sensor components could **halt production and cripple a provider's ability to fulfill orders**.

* **Platform Dependency Risks:** A heavy reliance on third-party platforms, such as POS integrators or cloud providers like AWS or Azure, creates **exposure to their policy changes, price increases, or outages**.

* **Stakeholder Activism:** There is a growing threat from activist groups focused on privacy and data ethics. Campaigns targeting a provider or its retail customers could generate **negative press and regulatory scrutiny**, impacting sales and brand image.

By leveraging AI to navigate this complex interplay of factors, companies can build a resilient and adaptive strategy that is prepared for whatever the future holds.

## Section 5: An Ecosystem of 15+ Specialized AI Agents to Revolutionize Biometric Payments 🤖

To conquer the complexities of the biometric payment solutions market, a new approach is needed—one that moves beyond traditional software to an ecosystem of intelligent, autonomous agents. These AI agents are designed to augment human experts, automate complex processes, and provide the predictive insights necessary to win in this dynamic arena. They can be deployed to systemize the value chain: from developing the core technology to integrating with POS systems, onboarding retailers, and providing continuous support.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

### A. The Two Priority AI Agents for Immediate Impact

While a full ecosystem offers comprehensive advantages, two priority workflows, embodied by specialized agents, stand out for their ability to address the market's most pressing challenges and opportunities.

**1. Aegis: The AI-Driven Multi-Modal Biometric Authentication Agent**

* **Agent Name & Function:** **Aegis** is a highly specialized security agent. Its core function is to fuse data from multiple biometric modalities—such as palm vein, facial recognition, and voice—in real-time to create a single, incredibly secure authentication decision. It uses advanced AI fusion engines and spoof detection modules to achieve an accuracy and security level that no single biometric can match.

* **Augmented Role:** Aegis augments the work of **Authentication System Engineers and Security Analysts**. It offloads the complex task of developing and continuously refining biometric fusion models, allowing human experts to focus on strategic security architecture and threat modeling.

* **Problem Solved:** It directly solves the market's central challenge: the trade-off between convenience and security. By using adaptive learning, it can dynamically adjust authentication requirements based on risk, ensuring a frictionless experience for low-risk transactions while stepping up security for high-value ones.

* **Game-Changer Impact:** Aegis is a game-changer because it transforms biometric security from a static defense to a dynamic, intelligent shield. It directly addresses consumer and regulatory demand for spoof-resistant, privacy-conscious authentication, impacting key KPIs such as **reducing fraud rates by up to 40%**, decreasing the **False Rejection Rate (FRR)** to below 0.5%, and improving overall **customer satisfaction (NPS)**.

**2. Sage: The Integrated Market & Competitive Intelligence Agent**

* **Agent Name & Function:** **Sage** acts as the company's strategic lookout. It continuously scans, aggregates, and analyzes a vast array of unstructured data from around the globe, including regulatory updates, competitor press releases, technology patents, and customer sentiment on social media. Using NLP and predictive analytics, it synthesizes this information into actionable intelligence.

* **Augmented Role:** Sage is the ultimate assistant for **Strategic Planners and Marketing Analysts**. It eliminates thousands of hours of manual research and provides a real-time, data-driven view of the entire market landscape, allowing teams to make faster, more informed decisions.

* **Problem Solved:** It tackles one of the market's biggest weaknesses: navigating the fragmented, rapidly changing competitive and regulatory environment. It provides early warnings of competitive moves or impending regulatory shifts, turning a reactive posture into a proactive one.

* **Game-Changer Impact:** Sage provides an asymmetric strategic advantage. By being the first to know about a new regulation or a competitor's weakness, a company can pivot its product roadmap or GTM strategy to seize opportunities before others are even aware of them. It directly impacts the **Lead-to-Customer Conversion Rate** by enabling more relevant messaging, improves the **Rate of New Feature Adoption** by aligning it with market needs, and shortens the overall **sales cycle** by equipping sales teams with critical competitive insights.

[PLACEHOLDER - MARKET SWOT PRIORITY URL]

### B. The Full Roster of Specialized AI Agents

Beyond these two priority agents, a full ecosystem of over a dozen other specialized agents can be deployed to optimize every facet of the business:

* **Optima (POS Integration Agent):** Augments **System Integrators** by automating the complex process of integrating with heterogeneous POS systems, drastically reducing deployment time and errors.

* **Sentinel (Compliance Management Agent):** A critical tool for **Compliance Officers**, Sentinel continuously monitors global biometric data laws, automates compliance checks, and prepares audit reports.

* **Futura (Customer Analytics Agent):** Assists **Sales and Marketing Teams** by using predictive analytics to identify high-propensity leads, forecast customer churn, and personalize retention offers.

* **Prime (Supply Chain Optimization Agent):** Works with **Procurement Managers** to predict supply chain disruptions for critical hardware components and recommend alternative sourcing strategies to ensure resiliency.

* **Liaison (Customer Education Agent):** Supports **Customer Service Teams** with AI-powered chatbots and personalized content to proactively educate users about privacy and security, building trust and accelerating adoption.

* **Scout (White Space Discovery Agent):** A strategic agent for **Business Development Teams**, Scout analyzes market data to identify underserved niches and adjacent market opportunities for expansion.

* **Shield (Anomaly Detection Agent):** Augments the **Security Operations Center** by monitoring transaction streams in real-time to detect and preempt fraudulent activity or security breaches.

* **Vision (Revenue Forecasting Agent):** A vital tool for **Sales Managers**, Vision analyzes the sales pipeline to provide highly accurate revenue forecasts and identify bottlenecks that are slowing down deals.

* **Max (Talent Development Agent):** An HR agent for **Technical Leads** that creates personalized learning paths to upskill the workforce in specialized AI and biometric domains, addressing the talent gap.

* **Echo (Partner Collaboration Agent):** A platform agent that facilitates co-innovation and data sharing with **Ecosystem Partners** like POS vendors and integrators, strengthening the value chain.

[PLACEHOLDER - MARKET AGENT SYSTEM URL]

### C. The Orchestrator Model: A Symphony of AI Collaboration

The true power of AI is realized not when these agents work in isolation, but when they operate as a cohesive, interdependent system under the command of a master orchestrator.

Imagine a **Merchant Sync Command Center**, a master agent that acts as the Chief Operations Officer for the entire value stream. This orchestrator would have a complete, real-time view of the entire business, from R&D progress to live customer support tickets. It would delegate tasks to its five specialized subordinate agents:

1. **PalmTech Development Agent:** Focused on core technology R&D.

2. **POS Integration Agent:** Manages seamless deployment to retail environments.

3. **Retail Onboarding Agent:** Ensures new customers are trained and activated efficiently.

4. **Customer Support Agent:** Handles ongoing issues and maintains satisfaction.

5. **Product Innovation & Growth Agent:** Scans the horizon for new opportunities.

The orchestrator wouldn't just delegate; it would manage the *synergies*. For example, if the Customer Support Agent detects a recurring issue with a specific POS integration, the orchestrator could instantly task the POS Integration Agent to investigate and simultaneously inform the PalmTech Development Agent to see if a core technology update could prevent the issue in the future. This creates a powerful, self-optimizing feedback loop that is impossible to achieve with siloed human teams. This vision of a fully AI-augmented organization represents the future of the industry—one where speed, intelligence, and operational excellence are not just goals, but the automated standard.

## Section 6: Let's build your new AI System together

[PLACEHOLDER - COMPANY URL]

## Conclusion & A Proposal for Strategic Discussion

Our deep dive into the biometric payment solutions market reveals a sector at a fascinating inflection point. It is a market defined by robust growth, with a **€9.5 billion TAM** and an **18% CAGR**, yet it is far from monolithic. The landscape is a mosaic of distinct segments, from the mature but regulation-heavy world of fingerprint and facial recognition to the high-growth, security-focused frontier of palm vein biometrics, which our analysis shows is poised to outgrow and disrupt the incumbents. Success is not guaranteed by simply having a good technology; it requires a nuanced GTM strategy tailored to the unique pains and priorities of each segment.

The competitive arena is a battleground where established leaders like **IDEMIA** and payment giants like **Mastercard** and **Visa** defend their territory against formidable challengers like **Amazon One** and agile innovators like **Natural Security**. The key axes of differentiation are clear: pure **technological innovation** and seamless **integration capability**. Mastering both is the price of admission to the leadership circle. The market's structural strengths, such as recurring revenue models and strong demand drivers, are counterbalanced by critical weaknesses, including regulatory complexity, long sales cycles, and a persistent scarcity of specialized talent.

The transformative potential of Artificial Intelligence is the thread that runs through this entire analysis. AI is no longer a buzzword; it is the critical enabler for navigating this complex environment. It offers the tools to build superior, multi-modal authentication systems, the intelligence to anticipate regulatory and competitive shifts, the automation to streamline complex integrations, and the predictive power to acquire and retain customers more effectively. An ecosystem of specialized AI agents, working in concert under a master orchestrator, represents the ultimate strategic advantage—a way to achieve a level of operational efficiency and strategic agility that is simply unattainable through traditional means.

The path forward for any ambitious player in this space is clear. It requires a laser focus on a chosen segment, a commitment to technological excellence, and a deep investment in AI-driven capabilities to outmaneuver the competition. The opportunities are immense, but the window to seize them is finite.

If you are interested in this topic you can follow these next steps:

1️⃣Download below the full Biometric payment solution market study in pdf format

2️⃣ Get additional insights of this market by reading our memo of an interesting company in this market called Handwave (Secure, fast palm-wave payments & age verification)

3️⃣ If you want us to build a custom AI system and dedicated AI agents, book a strategic discussion with an AI Partner : https://forms.proplace.co/meet