.png)

The Semiconductor manufacturing market by our Market Intelligence AI agent

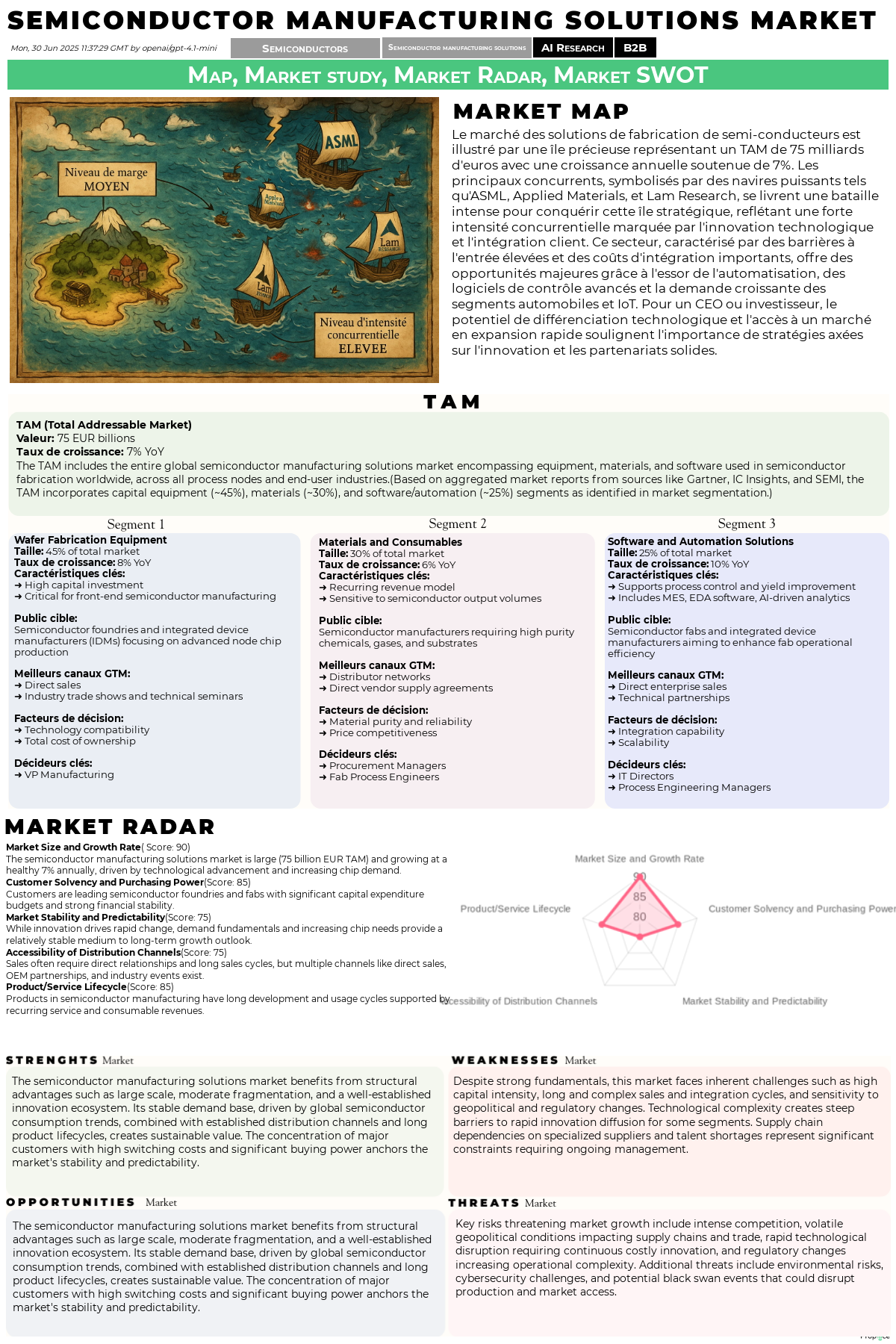

Semiconductor Manufacturing Solutions: A €75 Billion Market Under the AI Microscope

The global market for semiconductor manufacturing solutions is not just large; it's the critical enabler of virtually every modern technology, from artificial intelligence and 5G communications to autonomous vehicles and the Internet of Things (IoT). Our Market Intelligence AI agent's analysis, which synthesized data from leading sources including Gartner, SEMI, and IC Insights, values this ecosystem at a staggering €75 billion Total Addressable Market (TAM). It is expanding at a healthy Compound Annual Growth Rate (CAGR) of 7%, a figure that reflects the relentless global demand for more sophisticated electronic devices.

This market is broadly structured into three primary segments, each with distinct economic characteristics:

- Wafer Fabrication Equipment (45% of market): This is the largest and most capital-intensive segment, encompassing the complex machinery required for front-end-of-line (FEOL) processes like lithography, etching, and deposition. Dominated by a few key players, this segment is characterized by enormous R&D investments, long and intricate sales cycles (often 12-18 months), and high barriers to entry. Success is measured by technological supremacy, particularly in achieving smaller and more powerful process nodes.

- Materials and Consumables (30% of market): Representing the lifeblood of chip production, this segment includes high-purity chemicals, specialty gases, and substrates. Unlike equipment, it operates on a recurring revenue model directly tied to global semiconductor production volumes. Competitiveness here hinges on supply chain reliability, material purity, and cost-efficiency, making it a more volume-driven and price-sensitive business.

- Software and Automation Solutions (25% of market): This rapidly growing segment includes Manufacturing Execution Systems (MES), Electronic Design Automation (EDA) software, and AI-driven analytics platforms. Focused on optimizing process control, improving yield, and enhancing operational efficiency, this segment is the intelligence layer of the modern fab. It is characterized by faster innovation cycles and a shift towards subscription-based or as-a-service models.

While this segmentation provides a clear structural map, our AI detected deeper signals that reveal the market's true trajectory:

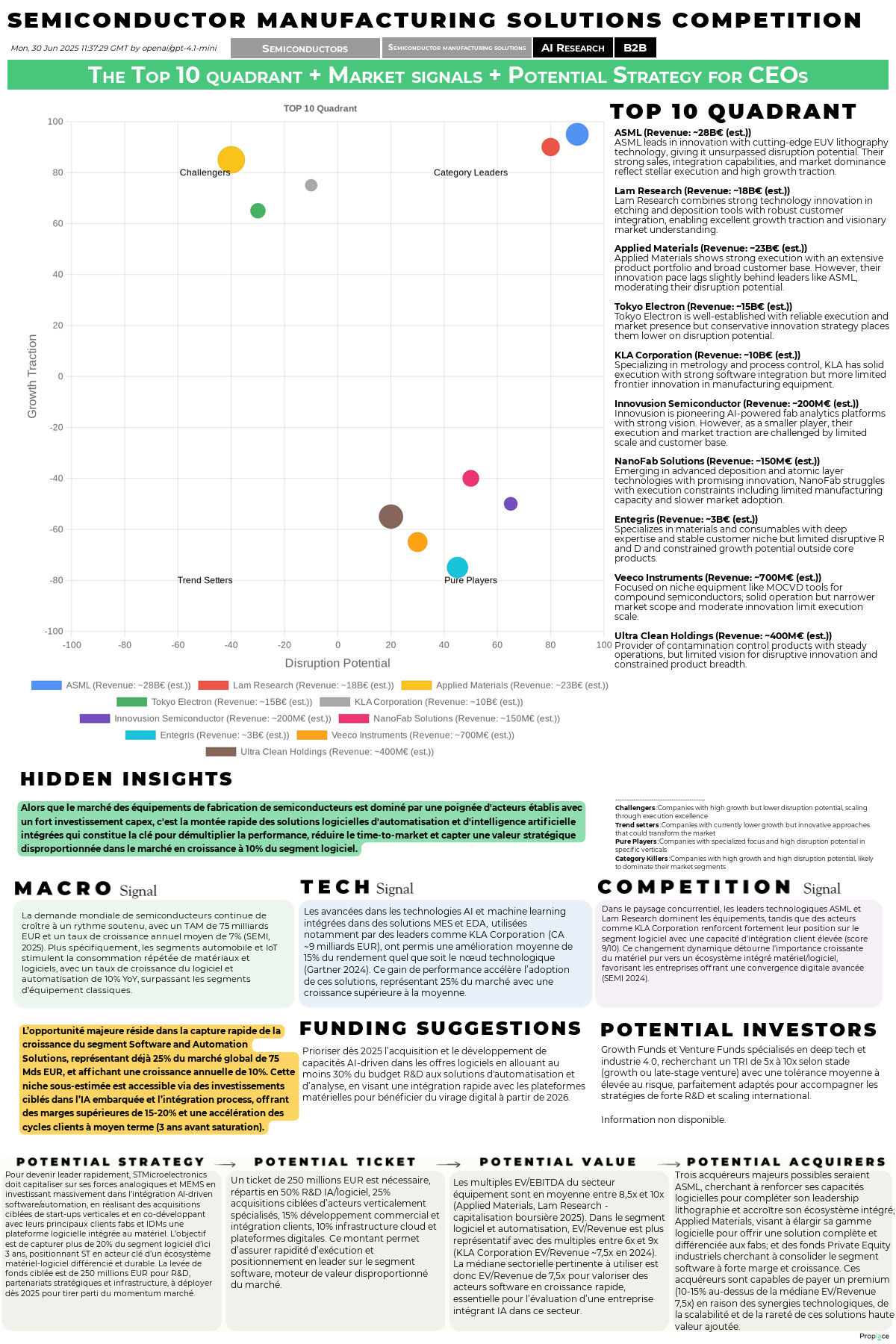

- Macro Signal: The most significant finding is the growth disparity between segments. While the overall market grows at 7%, the Software and Automation segment is expanding at an accelerated 10% YoY. This indicates a fundamental shift in value creation, where strategic control is moving from pure hardware capabilities to integrated, intelligent operational systems.

- Technological Signal: The integration of AI and Machine Learning is no longer theoretical. Leading fabs are reporting tangible ROI, including an average 15% improvement in manufacturing yield across various technology nodes, as documented by Gartner. This proven performance is turning AI platforms from a "nice-to-have" into a competitive necessity, accelerating their adoption.

- Competitive Signal: The traditional hierarchy, defined by hardware dominance, is being challenged. The competitive arena is shifting from a hardware arms race to a battle of integrated ecosystems. This dynamic allows software-centric players with strong integration capabilities—like KLA Corporation in process control—to wield disproportionate strategic influence.

- Demand Signal: Growth is increasingly fueled by the automotive and IoT sectors, which demand a high mix of specialized analog, power, and MEMS components. This trend favors companies with diverse portfolios and the ability to service recurring, high-volume needs for both materials and software.

- Regulatory Signal: Environmental regulations and geopolitical trade controls, particularly between the US, China, and Taiwan, are becoming major strategic factors. These pressures increase compliance costs but also drive innovation in sustainable materials and resilient, localized supply chains.

Looking forward two to three years, our AI predicts that the software and automation segment will grow its market share from 25% to over 30%. Furthermore, a vendor's ability to offer an integrated hardware-software-AI solution will become the primary decision factor for new fab investments, eclipsing the importance of standalone equipment performance.

The leaders of the next decade will be those who master this convergence.

TOP 10 Players: Who Truly Dominates the Semiconductor Manufacturing Solutions Market?

To understand the forces shaping this €75 billion market, it's essential to analyze who holds the power. Our Market Intelligence agent went beyond simple market share data, applying a multi-faceted methodology that combined a Magic Quadrant analysis—plotting players on axes of Growth Traction (Execution) and Disruption Potential (Vision)—with a rigorous evaluation based on Porter's Five Forces. This reveals a complex competitive landscape where dominance is a function of technology, integration capability, and strategic vision.

The Five Forces Defining the Competitive Arena

Our AI's analysis of the market's structural dynamics reveals the following power balance:

- Rivalry Among Existing Competitors (High): The rivalry is intense, particularly among a few established giants like ASML, Applied Materials, and Lam Research. Competition is fought on the battlefield of technological innovation (e.g., ASML's EUV dominance) and deep customer integration. While the market's 7% growth provides some breathing room, the fight for key accounts is fierce, demanding massive investments in both R&D and strategic marketing.

- Threat of New Entrants (Low to Medium): The barriers to entry are formidable. The immense capital required for R&D and manufacturing (billions for a new technology platform), protected by vast patent portfolios, and the locked-in relationships with major fabs make it exceedingly difficult for new players to compete at scale in the equipment segment. The software segment has slightly lower barriers, but integration with complex legacy systems remains a major hurdle.

- Bargaining Power of Buyers (High): The customer base is highly concentrated, with a few major foundries and IDMs (like TSMC, Samsung, and Intel) accounting for a huge portion of global purchasing. These clients are highly sophisticated, demand extensive customization, and have significant leverage in price and contract negotiations, giving them substantial power.

- Bargaining Power of Suppliers (Medium): While the market has many suppliers, those providing critical, highly specialized components—such as the advanced optics and lasers for EUV lithography systems—wield significant power. The availability of specialized R&D talent also acts as a supply-side constraint, giving key personnel negotiation leverage.

- Threat of Substitute Products or Services (Low): For advanced semiconductor manufacturing, there are currently few to no credible substitutes for core technologies like EUV lithography, atomic layer deposition (ALD), or plasma etching. While in-house development by fabs exists, it is rare and prohibitively expensive, solidifying the position of established equipment and software providers.

The AI-Generated TOP 10 Ranking and Analysis

Based on this framework, here is the AI-generated ranking of key players:

Market Leaders (High Vision & High Execution):

- 1. ASML: The undisputed king. Its monopoly in EUV lithography technology gives it unparalleled disruption potential. This vision is matched by flawless execution, with deep integration into the world's most advanced fabs. ASML isn't just selling equipment; it's selling access to the future of Moore's Law.

- 2. Lam Research: A formidable leader in the etching and deposition markets. Lam Research combines relentless technological innovation with robust customer integration and support, securing its position as a go-to partner for front-end manufacturing processes.

Key Challengers (High Execution, Less Vision):

- 3. Applied Materials: A giant with an incredibly broad product portfolio and a massive customer base, demonstrating powerful execution. However, its innovation strategy is more incremental than disruptive, placing it behind the leaders in pure vision.

- 4. KLA Corporation: A specialist powerhouse in process control and metrology. KLA's strength lies in its sophisticated software and analytics, giving it high marks on execution and customer integration. It embodies the competitive shift towards software-defined manufacturing.

- 5. Tokyo Electron (TEL): A major Japanese player with a comprehensive equipment portfolio and a reputation for reliability and quality. Its execution is strong and established, but a more conservative innovation strategy tempers its disruptive potential on the global stage.

Trend Setters (High Vision, Limited Execution):

- 6. Innovusion Semiconductor: A visionary startup pioneering AI-powered fab analytics. Innovusion represents the future of smart manufacturing, but as a smaller player, its ability to execute at scale and penetrate a market with long sales cycles is a significant challenge.

- 7. NanoFab Solutions: An emerging innovator in advanced deposition and atomic layer technologies. Its technology is promising, but the company struggles with the execution constraints of limited manufacturing capacity and slower market adoption.

Pure Players (Niche Focus, Limited Scale):

- 8. Entegris: A critical player specializing in high-purity materials and consumables. It operates with deep expertise in a stable niche but has limited disruptive potential outside its core product lines.

- 9. Veeco Instruments: A focused provider of niche equipment, such as MOCVD tools for compound semiconductors. Its operations are solid, but a narrower market scope constrains its overall growth and disruption rating.

- 10. BE Semiconductor Industries (Besi): A specialized leader in assembly and packaging equipment. With an established customer base in the back-end process, Besi shows strong execution in its niche but has a more modest impact on the broader front-end innovation race.

This mapping confirms the signals our AI detected: the highest long-term potential belongs to companies that can combine visionary technology with flawless, scalable execution. The challengers to watch are those leveraging software and AI to disrupt traditional hardware-centric models.

AI Reveals the Hidden Strengths, Vulnerabilities, Opportunities, and Threats of the Semiconductor Manufacturing Market

A surface-level view of the semiconductor manufacturing solutions market shows a robust, growing industry. However, our AI-driven SWOT analysis pierces through this perception to reveal a market defined by a fundamental paradox: its greatest strengths are intrinsically linked to its most critical weaknesses. Understanding this tension is the key to formulating a winning strategy.

Structural Strengths: The Foundations of a Powerful Market

The market is built on a bedrock of formidable strengths that create a stable and profitable environment for incumbents. The massive €75 billion TAM and its 7% annual growth provide a vast and expanding runway for business. This growth is fueled by powerful demand drivers, such as the irreversible expansion of AI, automotive electronics, and IoT, which ensures a consistent need for new and better chips.

Competitively, the market benefits from a structure dominated by a few leading players who engage in rational, technology-driven competition rather than destructive price wars. This environment is protected by high barriers to entry, most notably the vast intellectual property portfolios held by leaders and the deep, integrated relationships they have with customers. These relationships are further cemented by extremely high customer switching costs; replacing a core manufacturing platform is a multi-year, multi-billion-dollar endeavor, leading to exceptional customer retention (KPIs suggest an 88% rate) and long-term, predictable revenue streams. Finally, the rapid innovation cycles, supported by a strong global R&D ecosystem, allow for continuous differentiation and value creation.

Critical Weaknesses: The Inherent Friction in the System

Despite its strengths, the market is constrained by significant structural weaknesses. The most prominent is the long and complex buying cycle, which can stretch from 12 to 18 months for major equipment. This slows revenue velocity and dramatically increases the Customer Acquisition Cost (CAC), which averages around €300,000. This complexity is amplified by the market's high capital intensity. The enormous upfront investment in R&D and manufacturing facilities creates immense financial risk and a long payback period, favoring only the largest, most well-capitalized companies.

Operationally, the entire industry suffers from supply chain vulnerabilities, with a deep dependence on a small number of highly specialized suppliers for critical components, creating potential bottlenecks. This is exacerbated by geopolitical concentration risk, with the majority of manufacturing and expertise clustered in a few regions (Asia-Pacific, North America), making the system susceptible to trade disputes and regional instability. Finally, a persistent shortage of highly specialized R&D talent acts as a major constraint on the pace of innovation and growth potential for all players.

Untapped Opportunities: The Pathways to Future Growth

The market's weaknesses create clear opportunities for disruption and growth. The most significant is the shift towards automation and Industry 4.0, where AI and machine learning for yield optimization represents a revolutionary leap. This allows for the creation of new SaaS and platform-based business models that can transform capital expenditure into operational expenditure for customers.

Growth in emerging customer segments—particularly automotive and IoT—creates demand for new types of specialized semiconductors, opening doors for companies with expertise in analog and MEMS technologies. Sustainability transformation is another major vector; rising regulatory pressure and customer demand for greener manufacturing are stimulating innovation in sustainable materials and energy-efficient processes. Finally, geographic expansion into emerging semiconductor hubs offers a pathway to diversify beyond traditional centers and mitigate geopolitical risks.

Emerging Threats: The Risks on the Horizon

The primary threats are a direct reflection of the market's dynamic nature. Rapid technological disruption means that even today's leading technologies could become obsolete with the next breakthrough, requiring continuous and costly R&D investment. Intense competitive pressure from established leaders constrains pricing power and margins.

However, the most acute threats are external. Geopolitical and trade risks, especially tensions involving the US, China, and Taiwan, could fragment the global supply chain, restricting market access and disrupting production. Regulatory and policy challenges, from stringent environmental laws to export controls on sensitive technology, add layers of cost and complexity. Lastly, economic cyclicality tied to global semiconductor demand can cause significant fluctuations in revenue and investment.

The central paradox is clear: the market's stability and high barriers to entry (a strength) are a direct result of its slow, capital-intensive nature (a weakness). The winning strategy is not to fight this paradox, but to resolve it by using agile, intelligent software and AI to overcome the friction of the hardware world.

15 Specialized AI Agents for Semiconductor Manufacturing: Augmenting Human Capabilities

The strategic challenges and opportunities identified in our SWOT analysis are not just theoretical concepts; they are real-world problems and goals that teams face every day. The key to navigating this complex environment is to empower these teams with intelligent tools. Our Market Intelligence AI agent has designed 15 concepts for specialized AI agents, each serving as an augmented collaborator to amplify human expertise and directly address specific points in the SWOT.

From Market Weakness to AI-Driven Strength

The core idea is to apply AI precisely where the market's friction is highest. Long sales cycles, operational inefficiencies, supply chain risks, and compliance burdens can all be transformed by targeted automation and predictive insights. Here are 15 workflows designed to do just that:

Workflows to Optimize Core Operations & R&D:

- AI-Driven Yield & Process Optimization Agent (YieldMax): Augments Process Engineers and Fab Managers by analyzing real-time sensor data to predict and prevent defects. It dynamically adjusts process parameters to maximize yield, directly tackling the high capital intensity (Weakness) by improving asset ROI. It impacts KPIs like First Pass Yield (FPY) and Overall Equipment Effectiveness (OEE).

- Predictive Maintenance Agent (Nova): Augments Maintenance Engineers by forecasting equipment failures before they happen. This minimizes costly unplanned downtime, a major operational challenge (Weakness), and improves equipment uptime and OEE.

- AI-Enabled Digital Twin Agent (Optima): Augments R&D and Process Development Teams by creating a virtual replica of the fab. This allows for rapid, low-cost simulation of new processes, addressing the high R&D costs and slow innovation diffusion (Weaknesses).

- AI-Assisted R&D Acceleration Agent (Summit): Augments R&D Scientists by using AI to simulate material properties and automate data analysis. This directly counters the talent scarcity and high R&D costs (Weaknesses) by accelerating the New Product Introduction Rate.

- AI-Based Resource Optimization Agent (Prime): Augments Sustainability Managers by optimizing the consumption of energy, water, and chemicals. This addresses the regulatory burden of environmental rules (Weakness) and seizes the sustainability transformation (Opportunity).

Workflows to Enhance Commercial & Strategic Functions:

- AI-Driven Customer Engagement Agent (Echo): Augments Sales Representatives with AI-powered lead scoring and personalized communication workflows. It is designed to shorten the notoriously long 12-18 month sales cycle (Weakness) and reduce the high Customer Acquisition Cost (CAC).

- AI-Powered Demand Forecasting Agent (Faye): Augments Supply Chain Planners by providing highly accurate forecasts for materials and equipment. This mitigates supply chain vulnerabilities (Weakness) and captures growth from emerging segments like automotive (Opportunity) by ensuring product availability.

- Competitive Market Intelligence Agent (Sage): Augments Strategic Planners and Product Managers with real-time analysis of competitor moves, patent filings, and market shifts. This helps overcome information asymmetries (Weakness) and allows for a faster response to technological disruption (Threat).

- Emerging Market & White Space Identification Agent (Scout): Augments Market Development Managers by using AI to scan global data and identify untapped geographic markets or underserved product niches, directly pursuing the geographic expansion (Opportunity).

- AI-Driven Geographic Expansion Modeling Agent: A more advanced version of Scout, this agent augments Corporate Strategy Teams with data-driven models to de-risk market entry, directly addressing the threat of geopolitical concentration (Threat).

Workflows to Mitigate Risk & Ensure Compliance:

- AI-Enabled Regulatory Compliance Agent (Aegis): Augments Compliance Officers and Legal Teams by automatically monitoring global trade, export controls, and environmental regulations. It directly mitigates regulatory threats (Threat) and reduces the associated costs (Weakness).

- Smart Contract Compliance Agent: A specialized version of Aegis, this agent augments Legal and Procurement Teams by automatically analyzing supplier contracts for risks and compliance gaps, reinforcing supply chain governance.

- AI-Powered Collaborative Development Platform (Bridge): Augments Program Managers by creating secure, intelligent platforms for collaboration with suppliers and partners. This strengthens the ecosystem (Strength) and mitigates dependencies (Weakness).

- AI-Enabled Sentiment and Reputation Monitoring Agent (Insight): Augments Corporate Communications and ESG Officers by tracking brand sentiment in real-time. This helps manage the emerging ESG risks and stakeholder activism (Threats).

- AI-Driven Cybersecurity Agent (Sentinel): Augments Information Security Officers with real-time threat detection to protect sensitive fab data and intellectual property (Strength) from increasing cyber threats (Threat).

Each of these agents is designed not to replace humans, but to give them superpowers—freeing them from repetitive tasks and providing them with the predictive insights needed to make faster, smarter decisions in a highly competitive market.

The Orchestrator AI Agent: Coordinating the Semiconductor Value Creation Chain

While specialized AI agents can solve specific problems, the ultimate competitive advantage lies in creating a system where the entire organization operates as a single, intelligent organism. This is the vision behind the Orchestrator AI Agent System, a framework designed to coordinate the complete semiconductor value creation chain: "Designs and manufactures semiconductor devices by integrating R&D, fabrication, testing, and global distribution to deliver advanced chips for electronics."

Imagine a central intelligence that not only sees every part of the business in real-time but also understands how they connect and can proactively coordinate them to achieve strategic goals. This is the role of the ValueChain Optimizer Pro, an AI system architecture composed of one Master Orchestrator and five specialized sub-agents.

PrimeSync Command Center: The Master Orchestrator

At the heart of the system is the PrimeSync Command Center. This master agent augments the Chief Operations Officer (COO) by providing a holistic, real-time command center for the entire value chain. Its purpose is not to micromanage, but to orchestrate. It monitors key performance indicators from all sub-agents, identifies cross-functional bottlenecks, allocates resources according to strategic priorities, and drives system-wide optimization. It is the conductor of the AI symphony.

The Five Coordinated Sub-Agents of the Value Chain

PrimeSync coordinates five specialized agents, each mapped to a critical stage of the value creation process. Their true power comes from the synergy created through orchestration.

- R&D Innovation Agent (NovaVision): This agent augments the Chief Technology Officer (CTO) by accelerating the innovation pipeline. It analyzes simulation data, manages R&D projects, and scouts for new technologies.Orchestrated Impact: PrimeSync can feed real-time defect data from the Testing Agent directly to NovaVision, allowing the R&D team to address design flaws almost instantly. It can also relay market demand forecasts from the Customer Agent to prioritize R&D projects with the highest commercial potential. This improves the R&D Expenditure Ratio by focusing investment on what matters.

- Supply Chain Intelligence Agent (SupplyFlow): This agent augments the Supply Chain Director by forecasting demand for raw materials, optimizing inventory levels, and managing supplier risk.Orchestrated Impact: When the Fabrication Agent reports a planned increase in throughput, PrimeSync automatically instructs SupplyFlow to adjust its material forecasts and procurement orders, preventing future bottlenecks. This seamless connection improves Weekly Order Intake Value readiness and supply chain resilience.

- Fabrication Excellence Agent (AxelOptima): This agent augments the Fab Plant Manager by monitoring equipment health, optimizing process workflows, and maximizing wafer throughput and yield.Orchestrated Impact: PrimeSync ensures that the maintenance schedules proposed by this agent are perfectly aligned with the production forecasts from the Supply Chain Agent, minimizing disruptions. This directly improves Overall Equipment Effectiveness (OEE) and First Pass Yield (FPY).

- Testing Assurance Agent (EchoSure): This agent augments the Quality Assurance Manager by automating the analysis of test data, classifying defects, and performing root-cause analysis.Orchestrated Impact: This agent acts as the critical feedback loop. PrimeSync ensures that its defect analysis is immediately accessible to both the Fabrication Agent (for process adjustments) and the R&D Agent (for design improvements), creating a continuous quality improvement cycle that boosts the Customer Retention Rate.

- Customer & Market Insights Agent (MiraSage): This agent augments the VP of Sales & Marketing by analyzing customer behavior, forecasting market trends, and optimizing go-to-market channels.Orchestrated Impact: Insights from this agent are the starting point for the entire chain. When MiraSage identifies a surge in demand for a specific automotive chip, PrimeSync relays this signal upstream, triggering adjustments in R&D priorities, supply chain orders, and fab production schedules. This makes the entire organization market-driven and dramatically improves its agility.

This futuristic vision is one where the semiconductor value chain transforms from a series of sequential, siloed steps into a dynamic, interconnected, and self-optimizing ecosystem. Data flows seamlessly from market demand back to initial design, with every component adapting in real-time. This level of AI-driven orchestration creates an unassailable competitive moat, moving a company from being merely reactive to truly predictive.

STMicroelectronics: A Strategy Leveraging Core Strengths to Seize Market Opportunities

To ground this analysis in reality, our Market Intelligence AI agent conducted a deep-dive evaluation of a key industry player: STMicroelectronics. This simulation explores the strategic crossroads ST faces, examining a potential acquisition scenario and outlining an offensive growth strategy. The lessons learned are transposable to other established players in the sector.

Detailed Company Profile: A Diversified Powerhouse

STMicroelectronics stands as a formidable force in the semiconductor world, built on several unique competitive advantages:

- A Deep Technology and Patent Moat: The company holds approximately 18,000 active patents and has established undeniable leadership in specialized, high-margin segments like analog, MEMS, and power semiconductors. This IP protects its core business from commoditization.

- Global Manufacturing Scale and Resilience: With 11 primary manufacturing sites spread across 7 countries and a highly skilled workforce of nearly 50,000, ST possesses a robust and geographically diversified operational footprint that provides a crucial defense against supply chain disruptions.

- A Powerful R&D Engine: ST consistently invests around €1.5 billion annually (representing over 11% of revenue) into research and development. This fuels a steady pipeline of innovation and ensures its technology remains at the forefront of its chosen segments.

However, the company also faces challenges, including intense competition from capital-rich front-end equipment leaders and recent revenue headwinds that suggest a need for greater agility to capture new growth vectors.

Scenario 1: Potential Acquirers and Synergies

Our AI identified three logical acquirer profiles who might see immense value in ST and be willing to pay a premium:

- ASML: As the lithography leader, ASML could look to acquire ST to vertically integrate a vast portfolio of analog and MEMS technologies. The synergy would be powerful: combining ASML's dominance in cutting-edge equipment (a market strength) with ST's deep expertise in embedded technologies (an ST strength). This could allow ASML to create an unparalleled, end-to-end fab solution, justifying a significant premium by building a nearly unbeatable ecosystem.

- Applied Materials: As a strategic competitor seeking to broaden its offerings, Applied Materials could acquire ST to immediately bolster its position in the power semiconductor and analog markets. The acquisition would leverage ST's R&D talent and patent portfolio (ST strengths) to accelerate Applied Materials' own technology roadmap and offer a more comprehensive hardware-software solution to customers.

- A Private Equity Industrial Fund (e.g., KKR, Permira): A financial buyer would be attracted by ST's stable cash flows, strong brand, and deep technology assets (ST strengths). A potential strategy would be to use ST as a platform to acquire and consolidate smaller, high-growth software and automation players, directly addressing ST's current growth agility (a weakness) to unlock significant value through operational improvements and strategic repositioning.

Scenario 2: An Offensive Independent Growth Strategy

Should STMicroelectronics choose to remain independent, a passive strategy is not an option. Our AI suggests that an offensive growth strategy, fueled by a targeted €250 million investment, could be a powerful alternative. This capital wouldn't just fund more of the same; it would finance a strategic pivot.

The core of this strategy would be to leverage ST's primary strengths in analog and MEMS to capture the market's biggest opportunity: the 10% YoY growth in AI-driven software and automation.

The investment ticket of €250 million, suitable for Growth Equity or Late-Stage Venture Funds specializing in deep tech, could be allocated as follows:

- 50% to Accelerate AI & Software R&D: Building a world-class manufacturing software suite tightly integrated with ST's unique hardware for the automotive and IoT sectors.

- 25% for Strategic Acquisitions: Acquiring nimble AI and software startups to rapidly embed new capabilities and accelerate time-to-market.

- 15% to Scale Commercial & Integration Teams: Building dedicated teams to co-develop solutions with key clients and drive market penetration.

- 10% to Upgrade Digital Infrastructure: Creating the cloud platforms necessary to support modern Software-as-a-Service (SaaS) business models.

By executing this strategic pivot, it could be possible for STMicroelectronics to capture over 20% of the high-growth software segment by 2027. This would not only create a powerful new revenue stream but also transform its valuation multiples, enhancing its competitive moat and securing its position as a differentiated leader for the next decade. This simulation provides a valuable lesson for other hardware-centric players: leveraging existing strengths to pivot into high-growth adjacencies may be the key to future success.

Conclusion

The analysis of the €75 billion semiconductor manufacturing solutions market, conducted by our Market Intelligence AI agent, reveals an industry at a profound turning point. The data shows a clear shift in value from traditional, capital-intensive hardware to the agile, intelligent software and automation layer that controls it, a segment growing at a rapid 10% annually. The competitive landscape is no longer just a race for the next process node; it is an ecosystem battle where integrated hardware-software platforms, capable of delivering proven ROI through AI-driven yield improvements, are defining the new standard for leadership. Beneath the market's robust growth lies a fundamental tension between its strengths—high barriers to entry and sticky customers—and its weaknesses, such as long sales cycles and supply chain vulnerabilities.

The transformative impact of AI offers a direct path to resolve this tension. Specialized AI agents can augment human teams, turning operational friction into streamlined efficiency and providing the predictive insights needed to navigate complexity. An orchestrated AI system can coordinate the entire value chain, creating a level of agility and market responsiveness that was previously unattainable. For established players and challengers alike, the strategic imperative is clear: embrace AI not as a peripheral tool, but as the core engine for future growth and competitive differentiation.

Leaders in the Semiconductor Manufacturing Solutions sector who wish to delve deeper into these insights and discover which AI agents would be perfectly suited to their company's unique challenges can book a 15-minute strategic exchange with our AI experts. You will receive the complete 34-page study and explore the specific opportunities available to your organization.